Interesting that there are a couple of obvious-sounding "crypto projects" that were never seriously tried, let's take "decentralized search engine" as an example:

Naively, imagine a blockchain-based keyword + vector database and query engine...

where the priority of the domains are set by token holders. Search is burning a very small amount of the token.

Holders are incentivized to be both promoting their own agenda but keeping the usability of the engine. Competitors will enter and bid for higher ranking

Ironically, it’s extremely hard to convince an LP / allocator to increase the allocation exactly in that scenario.

I’d bet a meaningful amount that if @bennpeifert fund had continued, it would probably have seen a sharp recovery within a quarter.

There’s one easy concept in asset allocation that’s extremely hard to act upon: mean reversion after recent negative performance. Most stat-arb type strategies have actually higher expected forward returns in a drawdown.

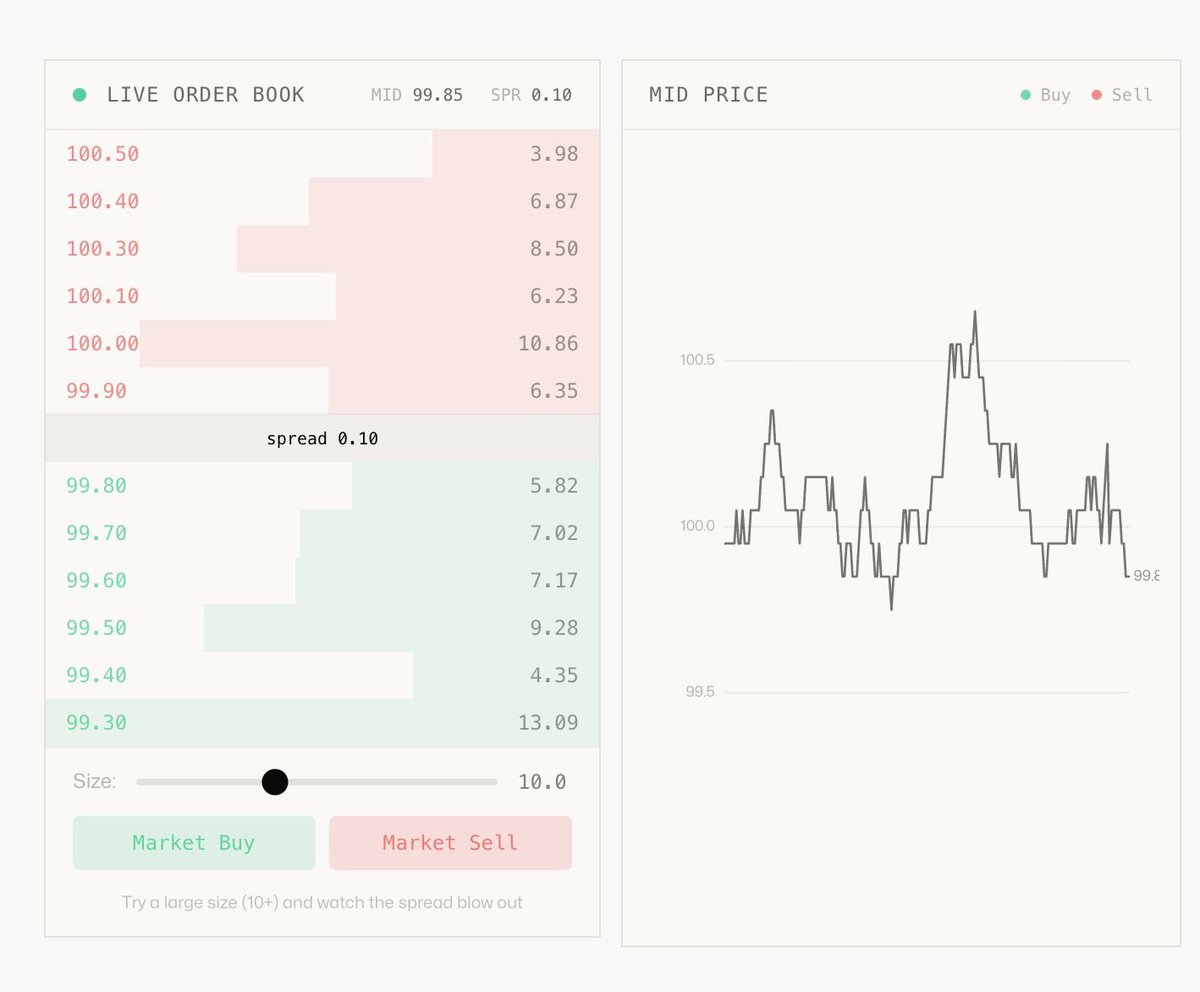

Market microstructure is usually explained in theory, but it only really clicks when you experience it.

We built an interactive guide: https://t.co/1LQfVXN0rE flow & liquidity play out instead of just reading about them!

Does it help get better intuitions?

We've been customers of every crypto data platform.

None gave us what quant research actually needs: point-in-time data, deep liquidity metrics, and real microstructure signals without survivorship bias.

So we built https://t.co/1x3rkTRhod. 100+ metrics. Full history

Now 40% off

I think one of the most interesting learnings from the flash crash was that HL's liquidations sub-vault https://t.co/1yxma8PWzr basically acts as a tail risk hedge

By design, our market-neutral factor portfolios weren’t affected: we have close to equal dollar amount of long/short positions - the experience is far different than holding a long-only portfolio of assets.

Friday’s flash crash definitely caught us by surprise: funding rates indicated “usual” amount of leverage and although retail participation was raising, it wasn’t even close to the levels of the 2021 euphoria.

What happened then?

There are some interesting theories going around about actors waiting for the right moment to dump a large amount of USDe on Binance to cause a local de-peg - that cascaded into a liquidation snowball: https://t.co/Sfm5hTIRgy

The Oct 11 Crypto Crash — What Really Happened

TL;DR:

Roughly $60–90M of $USDe was dumped on Binance, along with $wBETH and $BNSOL, exploiting a pricing flaw that valued collateral using Binance’s own order-book data instead of external oracles.

That localized depeg triggered $500M–$1B in forced liquidations, cascaded into $19B+ globally, and earned the attackers about $192M via $1.1B in BTC/ETH shorts opened on Hyperliquid hours earlier, but minutes before Trump tariff announcement.

It wasn’t a USDe failure!! It was Binance’s design flaw, timed with macro panic (Trump’s tariffs) for cover.

What looked like chaos was actually a coordinated exploitation of Binance’s internal pricing system, amplified by a macro shock and systemic leverage.

1️⃣ The Setup

Binance’s Unified Account let traders use assets like USDe, wBETH, and BNSOL as collateral.

Instead of oracle or redemption prices, Binance valued these using its own spot market - a major vulnerability.

On Oct 6, Binance announced a fix to move to oracle-based pricing, but rollout wasn’t until Oct 14, leaving an 8-day window.

2️⃣ The Exploit

During that window, sophisticated actors manipulated Binance’s order books, dumping ~$60–90M of USDe, driving it to $0.65 on Binance only (still ~$1 elsewhere).

Because the Unified Account marked collateral to internal prices, this instantly wiped margin value and triggered $500M–$1B in forced liquidations.

Then, Trump’s 100% China tariff headline hit, magnifying panic and liquidity stress.

3️⃣ The Profit Engine

The same day, fresh wallets on Hyperliquid opened $1.1B in BTC/ETH shorts, funded by $110M USDC from Arbitrum-linked sources.

As the Binance cascade unfolded, BTC and ETH cratered, those shorts netted $192M in profit before closing out at the bottom.

Timing, precision, and funding paths all suggest coordination.

4️⃣ The Contagion

Binance liquidations dumped BTC/ETH/ALTs into thin books.

Other exchanges mirrored the collapse through cross-market bots.

Market makers hedged across venues were forced to unwind everywhere.

Result: $19B+ global liquidations, with many alts down 50–70% intraday, all triggered by <$100M of manipulated collateral.

5️⃣ Who’s at fault?

Binance: design flaw + delay in oracle rollout = root cause.

Exploiters: executed and timed the manipulation, profited via external shorts.

Ethena (USDe): not at fault - protocol stayed 1:1 collateralized, redemptions normal, peg held everywhere else.

6️⃣ Aftermath

Binance admitted “platform-related issues,” promised compensation for affected margin/futures/loan users, and rolled out minimum price floors + oracle integration.

USDe remained operational, and the incident is now a case study in how exchange-side pricing errors can trigger system-wide liquidations.

Bottom line:

A ~$90M dump on Binance and a $1.1B leveraged short elsewhere sparked a $19B bloodbath.

Not a stablecoin failure, but a masterclass in exploiting flawed collateral valuation during peak macro stress.

One of our biggest factor research breakthrough came when we made turnover a first class citizen. The lesson was: high IC is essential, but not sufficient by itself. 1/5

To keep ourselves honest and avoid overfitting, we target a daily turnover of 30-40% for any factor—before we even look at performance.

See the difference yourself: “Altair” raw (with 100% daily turnover):

https://t.co/XKYpYEnbs0