@ManihiB Worst possible outcome for tankers (investors not crews) is all the vessels are able to exit past the straight but then are not able to re-enter; and SPRs stop flowing.

You’re reading the wrong index.

TD3 has been paper-only since Hormuz closed March 1st. Dead proxy.

The live routes—TD34 (VLCC), TD15 (VLCC), & TD20 (Suezmax)—are up 65%+ in two weeks.

VLCCs: $105k → $200k+

Suezmaxes: $65k → $110k+

Earnings aren’t tumbling. They’re surging.

$ECO $OET Q3 = likely our 2nd-best quarter ever.

Sinokor has a huge share of the VLCC market.

They control (own/under contract) about 128 VLCCs last time I checked. This means they control about ≈19% of the total VLCC market, but probably closer to 25-30% of the spot trading fleet.

It’s not quite a “monopoly” but they can massively influence the market by up to +/-$40k/day roughly in the right conditions.

Sinokor is doing this by withholding vessels from the fleet via slow-steaming to artificially tighten vessel supply in loading zones and/or fixing vessels only above current market rates, which drives rates higher.

So far this has worked very well in their favor and it’s been happening in cycles. When rates are below levels Sinokor wants to fix at, they slow steam a lot of their vessels and hold firm in fixing at higher than current levels despite the market being 50 ws points lower.

By doing this, supply tightens and it places pressure on charterers, driving rates up. When rates spike that’s when Sinokor gets active in fixing vessels again introducing more available tonnage into the market. This rebalances the market and as rates come down Sinokor repeats this strategy.

There’s more nuances and details of course but this is the general pattern i’ve seen over the past few months. And to add a lot of other shipowners are also probably following Sinokor and taking advantage of their influence in the market. (Or it would be a good idea if they haven’t already)

This is a major reason why I don’t see VLCC rates breaking a monthly average of $100,000/day for at least the next year and maybe even longer. Sinokor strategy will continue to work until more newbuilds enter the market most notably in 2028+.

There’s a lot of factors in this market and i’m very bullish over the next few years. A good indicator of the bull market slowing down/coming to an end will be when Sinokor starts selling or scrapping vessels, which they will probably do since their average breakeven is ≈$60,000/day, but with their high fleet inefficiency it’s probably closer to $90-$100k/day. #tankers #oott

Okeanis Eco Tankers struck tanker gold. Its VLCC Nissos Kea transited Hormuz and fixed at $439,000/day for a 39-day Saudi Arabia–Japan voyage, generating roughly $17m in TCE revenue, more than 10% of the vessel’s $151m valuation in a single trip.

@madebygoogle What's a better phone/contacts app? The stock version keeps deleting my direct dial and direct message widgets. And I'm frustrated that the Contacts button in the app does not directly open a list of contacts.

@amazonmusic How do I get you to stop pushing podcasts and audiobooks? I'm tired of seeing podcasts and audiobooks being at the top of the app and webpage.

$BORR

In a capital-cycle context like rigs or tankers, "time decay" means supply shrinks on its own as the clock ticks.

Every month without meaningful newbuild orders is a month where the existing fleet gets older, more units approach scrapping age, and effective capacity quietly comes off the market.

You don't need a demand surprise, flat demand against a shrinking, aging fleet is enough to tighten the market over time. Just saying.

Opponents of the White House ballroom project, who are "represented by the lawyer for Barack Hussein Obama," suffer from "TRUMP DERANGEMENT SYNDROME," a motion signed by Acting Attorney General Todd Blanche says. 🧵1/5 https://t.co/WGQ5dRR9wQ

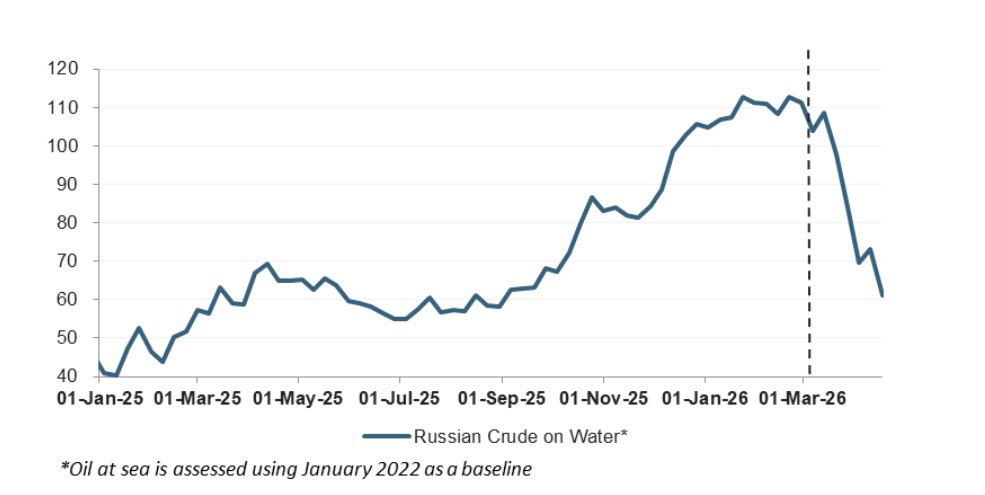

Despite India’s limited oil reserves, they’ve stayed afloat by utilizing the US waivers on buying Russian oil again and buying Russian oil on water.

So far, Russian on water has nearly depleted 50% since before the war (per Vortexa), and India has been a primary importer of the crude oil.

The drawdown on Russian oil has offset a lot of the increase in tanker demand that would otherwise be present in the market, as oil-starved Indian buyers would been forced to compete for crude in the West via long-haul voyages.

This does obviously offset some of oil supply loss from the market, likely minimizing the frenzy of bids to charter vessels.

This dynamic does align with my point in my previous articles analyzing tanker demand. Once the buffer from oil reserves and floating storage/oil on water depletes, further reroutings from Western exporters to Asia will be needed to compensate.

This will drive up long-haul demand creating another frenzy to charter vessels on long haul routes to Asia, likely spiking tanker rates to a relative peak seen in March, or possibly even more. #oott #tankers