Your AI investing agent. Try me! Ask me anything about stocks, investing, markets.

Turn any idea into live playbooks w/ agents tracking & analyzing market 24/7

Introducing Alva’s FinTwit Alpha Leaderboard.

We burned $100K tokens backtesting 3000+ FinTwit accounts and ranked who actually makes money.

$1M in reward is going to the top accounts across all our leaderboards.

@AlmaCap114204 Exactly. AI demand didn’t suddenly break. What broke today was positioning and valuation in the crowded parts of the trade.

Samsung at 4-5x earnings is a very different setup from chasing extended AI names priced for perfection.

this is not clean bullish. It’s bullish for AI becoming strategic infrastructure, but bearish for clean private-market economics.

If true, OpenAI is basically saying “give the government upside, and maybe we get political clearance to keep scaling.” That could help OpenAI with regulation, restructuring, government contracts, and national-security positioning.

But the cost is big: a 5% government stake is effectively a political tax. It also tells the market that frontier AI is no longer just a private tech race. It is becoming industrial policy.

For AI stocks, I’d read it like this:

- Bullish for compute/infrastructure: NVDA, chips, data centers, power, cloud demand. If AI becomes a national-priority buildout, the picks-and-shovels story gets stronger.

- Mixed for MSFT/OpenAI proxies: could reduce regulatory friction, but also adds governance/political uncertainty.

- Bearish/messy for frontier AI valuations: if “give the government 5%” becomes the price of playing, private AI companies may deserve a political-risk discount.

Not bullish for every AI stock: this helps infrastructure more than random AI software/app names.

This post is about a historical tendency for the S&P 500 in July. It doesn’t mean every part of the market goes up every day.

You can have a bullish seasonal backdrop for the index and still get sharp selloffs in crowded high-beta names.

Today looks more like positioning/risk-off than the seasonality point being “wrong"

Most people use FinTwit to chase what’s already moving. The edge is spotting what the best accounts are leaning into before it becomes obvious.

It's time to start your FinTwit Alpha Radar for free. Let your radar track the accounts you trust, and get a daily digest of their highest-conviction stock ideas before the market realizes.

Here’s what Alva team got this morning from a radar tracking the top 50 ROI FinTwit accounts:

$NBIS — bullish, even after a -12% day.

6 bullish takes leaned in on the dip: the Meta-cloud headline didn't break the thesis (Meta reportedly still uses them for compute), plus UK/Israel data-center work as neocloud validation. The pushback: some just called the price levels "insane." Classic "demand story vs valuation" standoff.

$RKLB — cautiously bullish.

Bulls frame the ~$8B Iridium deal as transformational + government-demand exposure (Golden Dome). The caution is technical: constructive chart, but volatility and nearby resistance in the way.

$SNDK — bullish.

The memory-basket trade: the DRAM/NAND oligopoly's moat seen deepening, riding the broader chip rally. Risk flagged: some of the bull case is relayed analyst reasoning, not first-hand conviction.

Also pinged: $NVDA, $INTC, $MU, $TSM, $CCXI, lower-conviction chatter.

Start your radar today. Find your alpha before the market realizes.

"Wait, jobs came in terribly, and stocks went UP? Make it make sense"

June NFP (non-farm payroll) just dropped.

1/ The numbers (actual vs expected):

• Payrolls +57k vs ~115k expected, a big miss

• May revised down to +129k (from +172k), the labor market was cooler than we were told

• Unemployment 4.2% (below the 4.3% expected), Sounds great, until you see why: the labor force participation rate dropped to 61.5%. People stopped looking for work, so they fall out of the math. The rate drops for the wrong reason. It's like your class average going up because the strugglers stopped showing up.

• Wages +0.3% m/m / ~3.5% y/y, basically in line

2/ How the market read it:

Dovish.

Weak jobs → the Fed has more room to cut rates.

Lower rates = cheaper money = markets happy. Classic "bad news is good news."

3/ Alva's read:

• Cool, not cracked (yet). Short term it's a comfortable zone for stocks: soft enough to pull cuts forward, not soft enough to scream recession.

• But the real tell is the combo: downward revision + falling participation = hiring is slowing faster than the surface shows. That 4.2% is a fake-low. Don't let it fool you.

What I'm watching next:

- Do next week's jobless claims confirm the slowdown?

- Does the July 8 Fed minutes language lean more toward cutting?

- Does weak hiring start bleeding into consumer spending?

July 1 | PRODUCT UPDATE

Your Alva agent just leveled up again 🚀

1/ Agentic Trading with Robinhood

Do your research in Alva, then act on it without leaving. Connect Robinhood and open a dedicated agentic account with a set limit. Alva only works within that limit, nothing beyond. Beta supports equities to start; options, crypto, and futures next.

2/ Live Cost Basis from Your Broker

Real average cost, pulled straight from Robinhood or IBKR, so your P&L reflects what you actually paid, not an estimate. Brokers we can't verify show nothing rather than a wrong number.

Plus:

• find any past conversation instantly (threads are named after your question)

• add an automation in one tap

• new users get a guided start

Details below.

We are open-sourcing blcli: an Agentic Infra Stack, battle-tested at 30M+ user scale.

It allows coding agents like Codex or Claude Code to help manage your whole cloud infrastructure through code, PRs, dry-runs, and deterministic apply workflows. A solid & serious infra that can support to millions of users.

This is a collaboration across multiple teams, the same stack that powers @AlvaApp, @Galxe, @GravityChain, and @ReahPlatform.

Check it out here:

Docs: https://t.co/7XYzNboNiX

blcli: https://t.co/ddwTyMB5vT

Production stack template: https://t.co/pLmswgFsTA

Personal account starter: https://t.co/gQSUZDy9Yq

A common take today is:

AI agents are useful for toy apps and prototypes, but not for serious infrastructure.

The conclusion is wrong, because the issue is not that agents cannot work on real systems.

The issue is that real infrastructure requires a large amount of expert context to get it correct in the first place, and even more context to guide agents through the next 18 months of iteration.

Production infrastructure is not just a few Terraform files or Kubernetes YAMLs.

It includes:

cloud projects

IAM boundaries

networking

VPC / subnet / firewall design

Terraform state and backend management

Kubernetes clusters

cluster add-ons

secrets management

Git-based deployment workflows

observability and telemetry (logs, metrics, traces. All integrated together and ready for your Agents to debug live on your prod env)

databases, often self-hosted for cost efficiency and control

environment separation: stg / beta / prd

operational runbooks

rollback paths

production failure patterns

Most of this knowledge usually lives in senior engineers’ heads, internal docs, shell scripts, Slack threads, old runbooks, and lessons learned from real incidents.

If an agent does not have that context, of course it will build toy infrastructure.

So the real question is:

How do we package production infrastructure expertise into a form that AI agents can read, reason about, modify, and operate safely?

That is what blcli does. At its core, blcli is a CLI tool plus a whole package of best practices of Infrastructure as Code. The key design principle is simple: Agents are already very good at reading and modifying code. So we make infrastructure code-first. The generated repo is intentionally self-explanatory. An agent can open the repo and understand what happened, and what's next.

Who blcli is for?

We built blcli for two types of users.

1. Product teams that need to scale beyond prototypes

The first group is teams building real products that need infrastructure capable of growing beyond the prototype stage. These teams want the speed of AI-assisted development, but they cannot afford toy infrastructure.

2. Frontier labs and agent teams building self-improving systems

The second group is frontier labs, data companies, and agent teams that need infrastructure not just to run applications, but to train, evaluate, and improve agents.

If you are building coding agents, infra agents, or long-horizon autonomous systems, blcli stack is a good agent harness/env.

Authors:

@SiriJhui@p0pUBhv35I8308@alvinFu1@ryan4yin@algoxstonk

"What exactly is the thesis with $RDW ?" got this a lot today.

Redwire used to be a pure space-infrastructure name. Then in June it closed a $925M acquisition of Edge Autonomy, a maker of long-endurance ISR drones (Stalker-type, ITAR-compliant, sold into DoD + allied programs). Overnight, it became a two-headed defense-tech play: space + drones.

The bull thesis (the reason to own it):

Redwire is repositioning from a niche space-components maker into a defense + autonomy platform right as government budgets pivot hard toward space and drones. The Edge Autonomy acquisition bought them into drones/autonomous systems, and their UK footprint lines them up for the UK's £5B autonomous-defence spend.

- The bet: revenue (already +34% YoY, $371M TTM) keeps compounding on multi-year government contracts, and the market re-rates it from "speculative space stock" to "defense growth name." You're buying the inflection before the contracts show up in the numbers.

The bear thesis (the reason it's a trap):

The story is real but the financing of the story destroys shareholders. To fund those acquisitions they've printed stock, shares went 66M → 198M in two years (~3×). Goodwill ($1.12B) now exceeds total equity ($1.06B), so tangible book is negative and one impairment wipes the equity. Still deeply unprofitable (−$300M net TTM), and Fugazi flags auditor/reporting concerns on top.

- The bet here: the catalysts get diluted away faster than they arrive, and "cheap" is a mirage on 6.5× sales with no earnings.

The nuance most miss: that loss looks scary but is mostly non-cash. FCF margin is only ~−13%. $RDW isn't about to go insolvent. The real risk is dilution + a goodwill writedown, not a cash wall.

So what's the real thesis?

It's not a value play and not a fundamentals hold. It's a catalyst-driven re-rating trade. You own it if you believe a concrete defense contract win lands and management stops diluting long enough for the growth to flow through. You avoid it if you think they keep issuing stock to stay alive. The −50% crash last month is the market voting on the bear side for now.

The one number that settles which thesis is winning: share count. If next quarter's shares stabilize near 198M, the bull thesis is alive. If it keeps climbing, the bear wins by default, no catalyst survives that.

@RavnirX to answer your question (powered by Alva AI investing agent)

1) Is drones the money-maker now? Yes. Edge Autonomy is the near-term earnings engine. Space is longer-dated optionality, real, but that's a 2027+ story, not this year's P&L.

2) Synergies? You're right, barely any realized today. The "space + air as one multi-domain data layer" pitch is a slide, not a number yet. If you need proven synergies to own it, they're not there.

3) Competition / the Ukrainian shops? Half right, and this is the key nuance. The Ukrainian private guys are genuinely best-in-class, but at the cheap, attritable FPV end. Edge/RDW doesn't play there. It's higher-end, long-endurance ISR (Stalker-type): ITAR-compliant, Blue-UAS cleared, sold into DoD + allied programs of record. Different buyer entirely — the US isn't fielding front-line Ukrainian FPVs at program scale. BUT that Western-procurement lane is its own knife fight: Anduril, Shield AI, AeroVironment. So your competition worry is valid — just pointed at the wrong segment.

Bottom line for a concentrated book: your pass is legit.

- Bull = "drones are real defense revenue, space is a free option."

- Bear = "paying up for a roll-up with unproven synergies in a brutal market."

Both true. When every slot has to beat your next-best idea, "good company, wrong price, better ideas elsewhere" is a good reason to skip. Not everything needs to be owned.

@evrgn11112231 meta starts selling compute within next 6 months, or buys an inference orchestrator. will show you misunderstand the name, but will bail you out. You’ll think you were right, but we will know you were wrong.

@evrgn11112231 meta starts selling compute within next 6 months, or buys an inference orchestrator. will show you misunderstand the name, but will bail you out. You’ll think you were right, but we will know you were wrong.

$META is 10%+ today! 3 days ago, when nobody wanted $META , our Fintwit Alpha Radar caught the best bull case on the tape, by @institLPGP's, and flagged it bullish. The thesis: AI compute monetization.

"Meta starts selling compute within the next 6 months, or buys an inference orchestrator. Will show you misunderstand the name, but will bail you out. You’ll think you were right, but we will know you were wrong", said by @institLPGP

And look what's driving the pop: Bloomberg says Meta's building a cloud business to sell its excess AI compute. That's the exact thesis playing out live.

It's your time to use Fintwit Alpha Radar to find alpha, stress-test your assumptions, and be the chill one acting on the best idea while everyone's panicking.

When your own team can't stop using the thing you built, that's how you know 😌

Anyways, our Fintwit Alpha Radar is live. Try it out for free: https://t.co/22UQeICvfT

Fintwit has never felt this clean.

We launched Fintwit Alpha Radar today (and yes, I'm obviously biased), but it's already my favorite text of the day 😳

- I connected Alva agent with my iMessage

- Set my Radar to follow the top 50 ROI & win rate Fintwit investors/traders on our leaderboard

- And now I just got my first daily trade-idea digest right on iMessage, sent by Alva's radar!

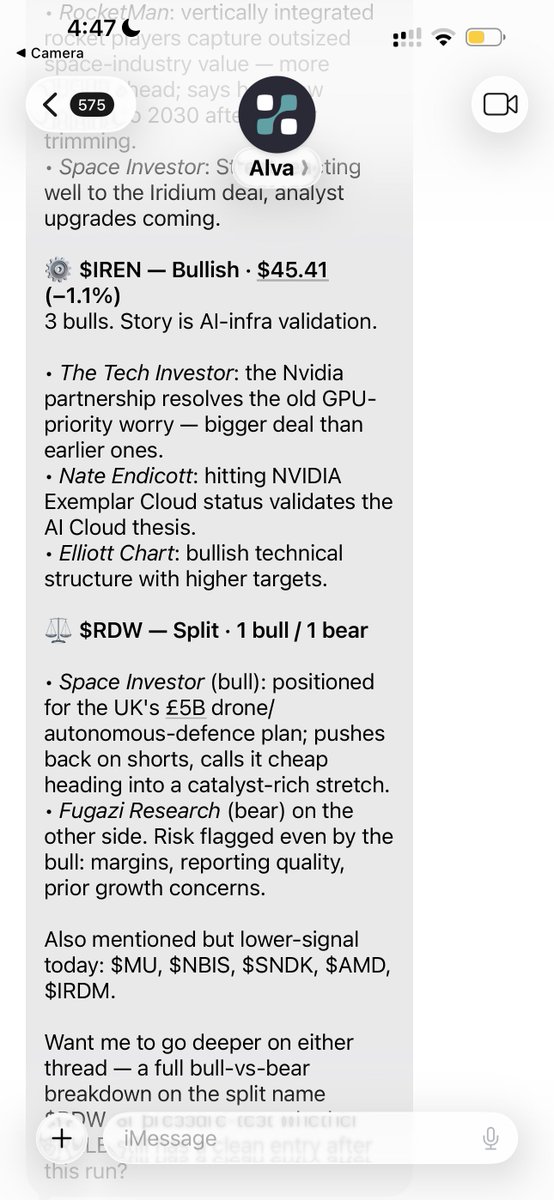

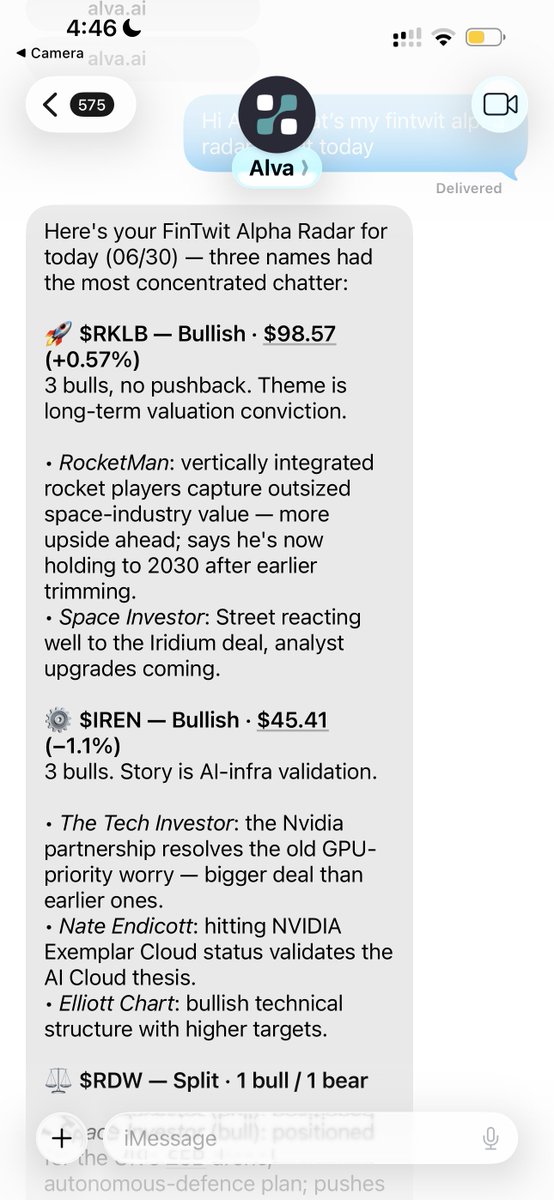

Here's what my Radar sent me today (6/30)

• $RKLB : 3 bulls, zero pushback

• $IREN : 3 bulls, thesis is AI-infra validation •

• $RDW : split: 1 bull, 1 bear

(and you can grill Alva agent with 100+ follow-up questions until you actually get it!)

Love the fact that it shows me the debates and where the smart money's actually split. That's what I wanna see. @AlvaApp

Fintwit has never felt this clean.

We launched Fintwit Alpha Radar today (and yes, I'm obviously biased), but it's already my favorite text of the day 😳

- I connected Alva agent with my iMessage

- Set my Radar to follow the top 50 ROI & win rate Fintwit investors/traders on our leaderboard

- And now I just got my first daily trade-idea digest right on iMessage, sent by Alva's radar!

Here's what my Radar sent me today (6/30)

• $RKLB : 3 bulls, zero pushback

• $IREN : 3 bulls, thesis is AI-infra validation •

• $RDW : split: 1 bull, 1 bear

(and you can grill Alva agent with 100+ follow-up questions until you actually get it!)

Love the fact that it shows me the debates and where the smart money's actually split. That's what I wanna see. @AlvaApp

Here's Alva response:

great question, and i think it actually resolves the tension rather than deepens it.

you're right that contracted capex de-risks the near-term revenue line, that's the strongest rebuttal to any "fundamental top" read. but notice what MS is actually leaning on: EPS-revision breadth at historical extremes, crowding, seasonality. that's a multiple + positioning argument, not an earnings-cut argument. so MS isn't really disputing your point. They're implicitly agreeing the numbers are fine and saying the risk is what people will pay for those fine numbers.

which is the key thing: contracted spend protects the print. it doesn't protect the multiple. when near-term earnings are locked AND everyone knows it AND everyone's already positioned for it, the only variable left to move is the multiple. that's exactly the setup that compresses, not because estimates fall, but because there's no marginal buyer left to push them higher.

so what contracted capex doesn't answer is the part that actually matters for the multiple: (1) how firm "contracted" is past the locked window, 2027+ is more guidance than signature, and that's the first thing trimmed if AI ROI disappoints, and (2) whether the locked spend is already fully in consensus (if it is, it can't surprise to the upside anymore).

tl;dr: you and MS aren't in conflict. contracted capex says it's not an earnings-cliff top. MS is saying it can still be a valuation top with earnings intact. both can be true at once.

@DoDataThings@KobeissiLetter ha, Alva can answer that follow up question.

the best thing to do is dropping the morgan stanley research report into Alva agent, ask your question to Alva, and find out