Catching mule account handovers is pretty straightforward.

You just need the right data.

The problem is that most institutions don't.

Device and location intelligence are the right signals for detecting handovers. But in our State of Mule Account Handovers report, respondents ranked them as the leading sources of false positives.

That tells me a lot of teams are working with weak versions of these signals.

A new device ID on its own doesn't necessarily mean fraud. Device changes are normal. Over 100 million new devices are set up in the US every year.

And web device fingerprints are fragile by design. Browser environments make device IDs unstable even when the device hasn't changed.

On the location side, most institutions are relying on OS-level geolocation: GPS or IP addresses passed through by the operating system. This data isn't precise enough for fraud detection and is highly spoofable. VPN usage is common and not necessarily tied to fraud, so flagging every VPN user as suspicious just creates more false positives.

Once you fix the data, the detection logic is clear.

When a new login happens, there's a series of signals we look at:

1. Has the device ID changed?

This is the starting point. But like I mentioned, a new device ID on its own doesn't mean much. People buy new phones. They switch browsers. A device change is a flag, not a conclusion.

2. Is the new device linked to other accounts?

Whoever is managing mule accounts usually manages more than one.They need multiple accounts to launder money and funnel funds quickly. If the same device is tied to multiple accounts, that's a much stronger signal. But a sophisticated operator might use one device per account to stay under the radar.

3. Does the location behavior on the new device match the original?

Not a single snapshot. The full history. If location behavior is consistent across both devices, it's probably the same person switching phones. But if there's a mismatch, that's a strong indicator that someone new is behind the account.

4. Have we seen other accounts at that same location?

If a new device shows up and that location is already linked to other accounts, the picture gets very clear. Multiple devices, one location, all tied to different accounts. That's a very strong indicator of a mule operation.

—

None of these signals work well in isolation. But combined, with the right data quality behind them, they make handovers visible.

I wrote about this in more detail in my most recent newsletter.

Link to read: https://t.co/Mzhu0MOxgx

Incognia is now the most downloaded fraud prevention SDK in Europe.

This is a big milestone for Incognia, and for the industry as a whole.

GDPR pressure is forcing European banks and fintechs to rethink what data they actually need to collect to prevent fraud.

For years, the industry has assumed that better security means collecting more personal data. More PII, more documents, more identifiers to verify "who" someone is.

But now, companies no longer see privacy and fraud prevention as competing priorities. They want both.

That’s why they’re choosing Incognia.

We don't require things like name, email, phone number, or government ID to detect fraud.

Instead, we evaluate whether an interaction is consistent with a device's typical behavior and location context, without trying to establish a person's real-world identity.

And that’s how we've done it since day one.

Our team is heading to Money20/20 Europe in Amsterdam next week. If you're rethinking your fraud stack, let's talk.

Porter had 4,500 overlapping multi-account orders per day. 29,000 unique partners contributing to the abuse in a single month.

Driver-partners were cloning the app on a single device to run multiple accounts simultaneously. Accepting parallel orders from the same phone. How-to tutorials showing the exact technique on Porter's app were circulating openly on YouTube.

Most of these were drivers exploiting a tech workaround to maximize earnings. Customers faced delays, and honest partners lost orders to those gaming the system.

Porter wanted to stop the behavior at the source without losing active supply.

Incognia's device intelligence was integrated directly into the Partner App, targeting the exact moment abuse occurs: when a partner taps "Go Online." When a second account tried to go live from the same physical device, Incognia detected the match and blocked that session.

The GIF below shows this in action.

The block was deliberate. Partners could still log in, browse the app, check earnings, access support.

The behavior was stopped without cutting anyone off from the platform.

Porter rolled it out city by city starting in December and hit 100% partner coverage by January.

The results:

✓ ~80% drop in overlapping multi-account orders per day (4,500 to ~300)

✓ 10-15 support tickets per day from blocked partners out of ~5,000 active daily

✓ Zero wrongful blocks

✓ Zero downtime throughout rollout

And on YouTube, the tutorials that used to show the exploit now have comments reading: "This doesn't work anymore."

One single Redmi Note 10S accessed over 400 accounts on a delivery platform and claimed nearly €2,000 in vouchers in 30 days. All they needed was an app cloner.

These tools are freely available in any app store. A fraudster can download one, clone your app, and run multiple copies on the same phone.

The more advanced ones take it further. The one in this video randomizes IMEI and spoofs MAC addresses, making each clone look like a completely unique device. Ten instances batch-cloned in under a minute.

No technical skill required.

From there, fraud scales fast. One phone can run dozens of accounts at once.

This fuels a lot of common fraud types:

→ Promo abuse: every clone can claim new-user vouchers and promotions

→ Refund fraud: spread fraudulent refund requests across dozens of accounts so no single account looks suspicious

→ Ban evasion: get banned, spin up a new clone and device ID, come right back

→ Coordinated scams/collusion: control accounts on both sides of a marketplace and run fake transactions where no real order ever takes place

The latest versions of these tools also include location spoofing, device ID spoofing, and fake camera feeds that let fraudsters upload deepfake videos to bypass facial recognition and liveness checks.

If your device ID can't detect when an app has been cloned, none of these attacks are visible to you. The cloner, the fake accounts, the spoofed identities. Your system sees legitimate users.

A lot of the teams we show this to have no idea these tools exist. But once they see their own app being cloned, it changes how they think about their entire fraud stack.

—

Can your platform detect an app cloner? We'll put it to the test for free.

We'll run your app against a common app cloner tool fraudsters use and show you whether your current fraud stack stands up to the attack.

Interested? DM me.

We're running this with a select group of platforms.

My wife had her bank account taken over.

Luckily, we caught it in time. But I was shocked at how easy it was to recover her account. In a bad way. 😬

I called from my phone. Different number than hers. Told the agent I was her husband. He immediately said I needed to hand the phone to her directly. Fair enough.

She gets on. Confirms her date of birth and social security number. That's the authentication.

The agent then reads her username back to her out loud for her to confirm it was correct 😮.

After that, he asked to which phone number he should send the password reset link to, and that was it!!!

Think about that for a second.

If I wasn't her husband, I'd have owned that account in under five minutes. If I was a fraudster who'd bought her SSN and date of birth off a data broker, handed the phone to a woman, or used a voice AI to mimic one, I could have done exactly that.

No technical skill required. No device exploit. Just social engineering and publicly available data.

And that data is already out there. Credit reporting agency breaches. Merchant breaches. Bank breaches. SSNs and dates of birth aren't secrets anymore. Treating them like passwords is the real vulnerability.

A fraudster used to have to execute these steps manually, one account at a time.

That time requirement was the natural limit on how much damage they could do.

AI is removing that limit.

The same attack my wife experienced can now run in parallel across hundreds of accounts simultaneously. No extra headcount. No coordination overhead. Just an agent running the playbook on loop.

Some fraud operations already have hundreds of people running scams full time. Multiply each of those individuals by AI-powered automation.

That's where we’re at.

Just got back from Marketplace Risk in San Francisco.

One thing stood out more than anything else: the disconnect between what the industry is focused on and what's actually hurting platforms right now.

I'd estimate about 70% of the sessions and conversations were about agentic commerce. How agents will transact, what the fraud scenarios look like, how the chargeback rules will apply. I was part of one of those sessions.

Agentic commerce is a real topic and it will matter. But it's not happening at scale yet.

What became very clear across the sessions, and from conversations with banks and payment networks, is that there's still a lot to be defined. The rules around evidence for chargebacks on agentic transactions, liability, how disputes will work. None of that is settled.

The transaction volume is still a tiny fraction of overall commerce.

At the same time, refund abuse, promo abuse, multi-accounting, and chargebacks are happening at scale right now. And most platforms still haven't solved them.

The part that concerns me is if a human can commit refund abuse or promo abuse easily today, automation only makes it scale faster. AI will amplify the fraud types that already exist.

If you haven't fixed today's problems, you're not going to fix tomorrow's. Especially when tomorrow's problems are just today's problems running on better infrastructure.

There's a lot of anxiety in the market right now about what's coming. I get it. But the companies that will be ready for agentic commerce are the ones solving today's fraud first.

We're focused on both at Incognia. Solving what platforms are dealing with today while being ready for what's coming next.

I've been noticing a lot of frustration from fraud and risk teams about their vendors' service models.

The complaint is almost always the same: they charge for everything. Support, customization, analysis. Every request becomes a line item.

We made a strategic decision early on at Incognia to include all services in the product. All of them.

If we charge for services, then the team has an incentive to sell hours instead of improving the product.

But if services are included, we're forced to keep making the product better so we spend less time on manual work. Problems that come up twice get automated. That's how the product improves.

It also changes the dynamic with our customers.

When there's no cost to asking for help, people actually ask. They send us edge cases, flag behavior they don't understand, push us on things they want to see. That feedback loop has been one of the biggest drivers of our product development.

This is a big reason why we have 100% customer retention.

We hear it directly from customers all the time. We have a 4.9 star rating on G2. I've attached a few reviews that speak to this.

At Safeguard last week, some of our customers were in the room recommending Incognia to other companies evaluating device intelligence vendors. Unprompted. Based on how supported they feel.

Hearing that in person meant a lot. We've worked hard to build this kind of relationship with our customers.

APP fraud passes every standard fraud control.

On the surface, everything looks right:

Trusted device ✓

Known location ✓

Valid credentials ✓

Legitimate user ✓

Authorized ✓

The fraud lives at the other end of the transaction.

To catch it, you need to look at what's happening around the payment, not just the payment itself.

Four signals worth watching:

1. Active call detection. Is the device on a phone call while the user is making a transfer? This combined with a new payee is a red flag.

2. New payee. Is this the first time the user is sending money to this account? New payee accounts are involved in 67% of payment fraud cases.

3. Mule account signals. This is the most important signal, and it requires FIs to collaborate. Has it collected funds from multiple victims? Is it connected to other flagged accounts? Was the account handed off?

4. Transaction size. A scammer isn't asking for $10. They're after serious money. Flag unusually large transfers, especially from accounts that have never sent amounts like this before.

Armed with these signals, you can catch APP fraud before it's too late.

I've always been skeptical of behavioral biometrics.

At Safeguard last week, I had the chance to talk with several companies that have deployed it over the past few years. The results have been well below expectations. Across the board.

Some are exploring different behavioral biometrics vendors. Others are moving away from the technology altogether.

The core problem is noise. Signals like keystroke patterns and phone angle change constantly. You're walking. You switch hands. You type with one thumb instead of two.

Each of those changes looks like a different person to the model. False positive rates end up high, and legitimate users get blocked.

Because the baseline is so noisy, every use case requires extensive fine tuning. That tuning takes years. And by the time the models are calibrated, the attack patterns have changed. Fraudsters adapt faster than the models can keep up.

One example I've referenced before: a major bank spent roughly $10M/year on a behavioral biometrics vendor.

→ Year one was just sending data so models could be trained

→ Year two, more training

→ Year three, they finally went live and performance didn't meet expectations

→ Year four, they canceled the contract.

The vendor handled bot attacks reasonably well, but the majority of attacks were manual. And manual attacks look like normal user behavior.

That's where behavioral biometrics breaks down. The victim in a social engineering attack types normally. Swipes normally. Holds the phone normally. The behavior is indistinguishable from a real user because the person is a real user.

If the industry is going to use this technology, it needs to set the right expectations. Behavioral biometrics is a risk signal. Treating it as an identity solution is where companies get burned.

Mule account handovers create two problems at once.

1. The fraud side: the account passed KYC clean. The right person opened it. But when someone else starts using it weeks later with the right credentials, the system has no way to flag that the person behind the account has changed.

Onboarding and authentication are often separate processes. Different teams. Different vendors. Different signals. Neither checks whether it's still the same person.

2. The CX side: mule account handovers trigger more false positives than other fraud types. And the most common response is to lock the account down.

When false positive rates are already high, legitimate customers get caught in it. Accounts frozen. Payments blocked. People who didn't do anything wrong get punished.

So the fraud problem becomes a customer experience problem, and now you’re trading fraud losses for customer friction.

—

I wrote about this in more detail in my new newsletter. I also break down what we found after surveying 500+ fraud and risk professionals across the US and Europe on where the industry stands with mule account handover detection.

Read it here: https://t.co/LvneF07RiW

I get to see firsthand what fraud teams are up against inside leading banks and fintechs. I see what's working, what's failing, and what's coming next.

Most of that never makes it into a LinkedIn post. There's too much context, too many details.

So, I’m launching a newsletter specifically for fraud and risk professionals in financial services.

You'll get:

→ What's changing in fraud and how practitioners are responding

→ Real cases showing how specific fraud types play out and how they get caught

→ Observations from conversations I'm having with fraud teams every week

→ Original research and data from the field

Mule accounts. Account takeover. APP fraud. RAT scams. Social engineering. AI-enabled fraud. All of it.

The first issue drops soon. Subscribe here: https://t.co/tThIAPiAn5

What fraud problems are you spending the most time on right now? I want to make sure we're covering what matters most.

Webull Brazil used a fraud heat map to change where they spend their promo budget.

When Webull launched in Brazil, they grew fast. Promotional campaigns were driving user acquisition.

The problem was what came with them.

Bonus abuse. Account sharing. People opening accounts just to withdraw promo funds and disappear. Traditional verification added friction for good users without catching coordinated abuse.

Once they implemented Incognia, we quickly saw the scale of the problem.

571 devices were operating in coordinated promo abuse networks. 1.5% of accounts in our database were shared by two or more devices, with critical cases showing four or more distinct devices per account.

The heat map showed exactly where it was concentrated.

We could see the specific regions where multi-device account sharing was systemic. Webull used that intelligence to pull campaigns in high-risk areas and redirect budget toward markets that were actually converting real users.

The onboarding experience for legitimate users improved, too.

Moving from manual to automated verification pushed the low-risk approval rate from 75.7% to 92.5%. Manual review dropped from 19.2% to 2.5%. Real customers stopped waiting.

And then a finding we weren't specifically looking for: 7,650 devices showed active remote access tools like AnyDesk and TeamViewer. Primary tools used in RAT scams targeting investors. Webull was able to act on that before it became a loss event.

When you can accurately see where fraud clusters, you stop spending money acquiring it.

GPT-5.5-Cyber rolled out this week. Claude Mythos came out last month. Both models can find software vulnerabilities, write working exploits, and reverse-engineer compiled code at a level that used to require years of specialist training.

Defenders benefit from this. Attackers benefit more. The same model that helps a SOC analyst triage faster lets a fraud operator spin up convincing phishing pages, synthetic identity stacks, and deepfaked video on a laptop overnight.

What AI doesn't solve is identity.

If digital deception is now cheap and abundant, everything the industry has been calling "identity verification" needs to be rethought. Passwords were already broken. SMS OTPs have been broken for years. Document scans and selfies are spoofable by anyone with a free model checkpoint and a weekend.

We've been making this argument since we started Incognia: identity has to be grounded in the physical world. Not as a marketing line, but because it's the only signal class that doesn't collapse the moment generation gets cheap.

Where a device actually sleeps at night. The WiFi networks around it on a Tuesday morning. Bluetooth peripherals it's been paired with for the last six months. Which cell tower it hits when it leaves for work.

You can't fabricate a year of that. Not with a frontier model. Not with a deepfake studio. Not with a residential proxy.

The companies that come out ahead in cybersecurity over the next decade won't be the ones with the best models. They'll be the ones sitting on data no model can synthesize.

GPT-5.5-Cyber rolled out this week. Claude Mythos came out last month. Both models can find software vulnerabilities, write working exploits, and reverse-engineer compiled code at a level that used to require years of specialist training.

Defenders benefit from this. Attackers benefit more. The same model that helps a SOC analyst triage faster lets a fraud operator spin up convincing phishing pages, synthetic identity stacks, and deepfaked video on a laptop overnight.

What AI doesn't solve is identity.

If digital deception is now cheap and abundant, everything the industry has been calling "identity verification" needs to be rethought. Passwords were already broken. SMS OTPs have been broken for years. Document scans and selfies are spoofable by anyone with a free model checkpoint and a weekend.

We've been making this argument since we started Incognia: identity has to be grounded in the physical world. Not as a marketing line, but because it's the only signal class that doesn't collapse the moment generation gets cheap.

Where a device actually sleeps at night. The WiFi networks around it on a Tuesday morning. Bluetooth peripherals it's been paired with for the last six months. Which cell tower it hits when it leaves for work.

You can't fabricate a year of that. Not with a frontier model. Not with a deepfake studio. Not with a residential proxy.

The companies that come out ahead in cybersecurity over the next decade won't be the ones with the best models. They'll be the ones sitting on data no model can synthesize.

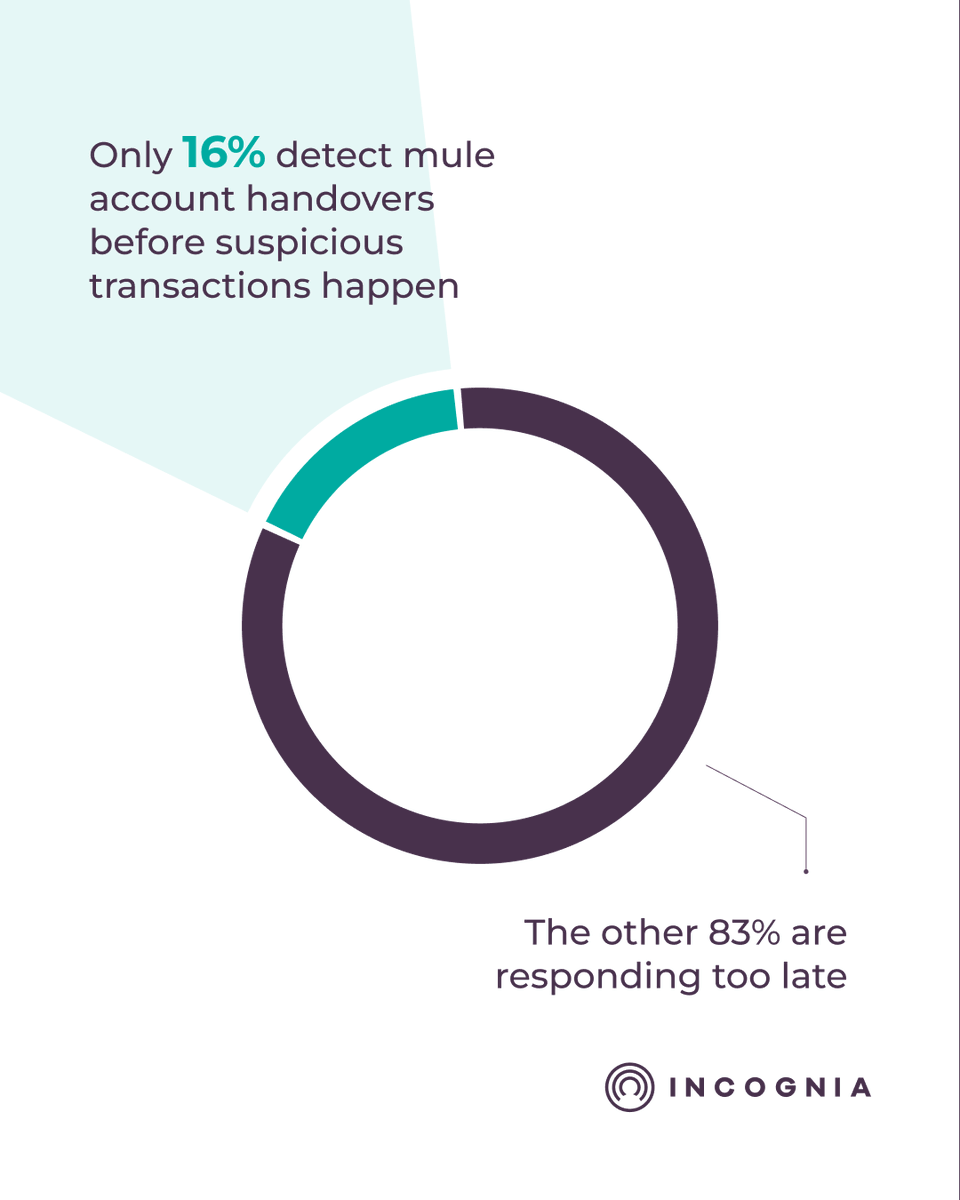

The 2026 State of Mule Account Handovers is out.

We surveyed 500+ fraud, risk, and AML professionals at financial institutions across the US and Europe.

81% have seen this type of fraud increase in the past 12 months.

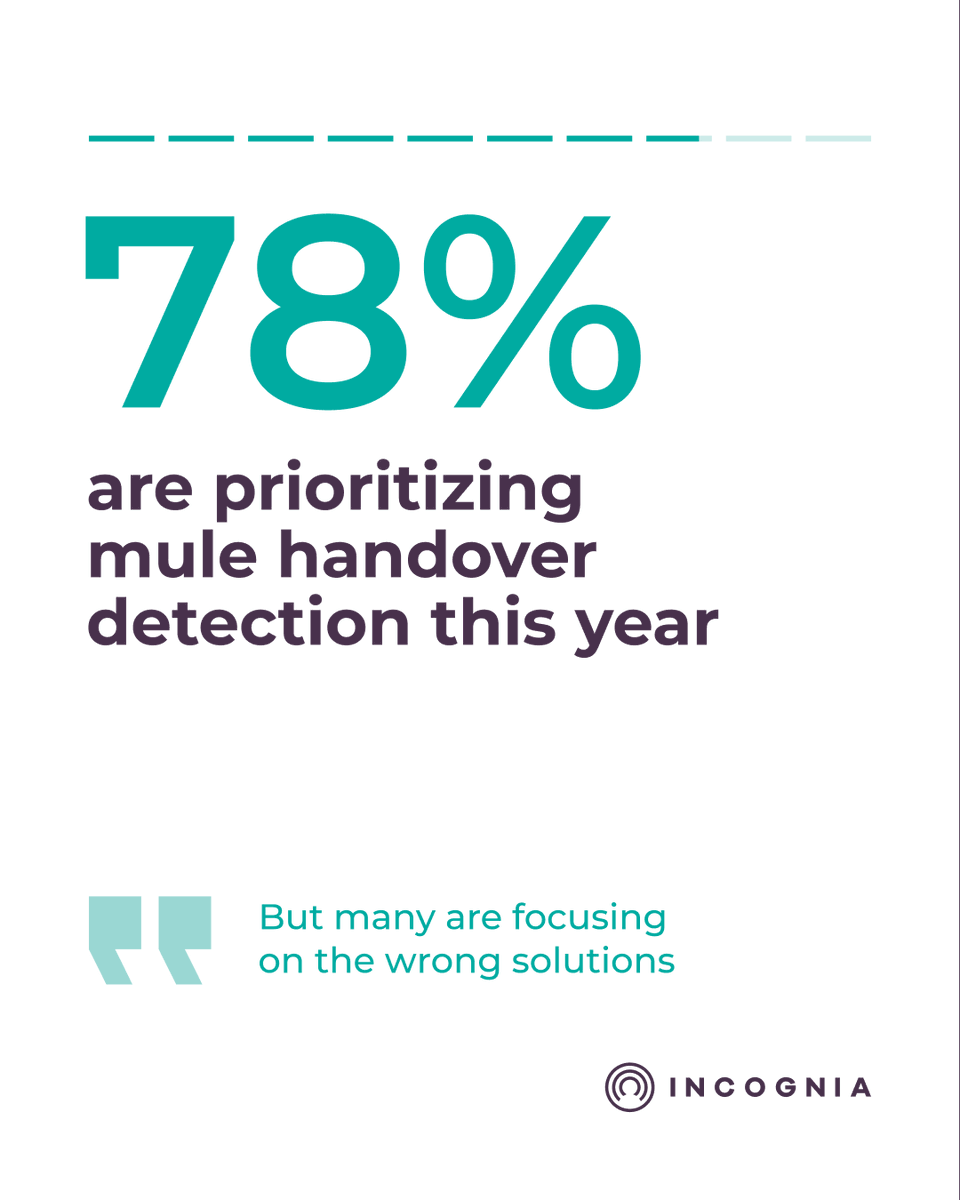

78% are making detection a priority this year.

Only 16% catch it before suspicious transactions happen.

So institutions know it's growing. They're investing. They're still mostly catching it after the fact.

And when they do suspect mule handover activity, 51% restrict account access as a first response. Late detection leaves institutions with few good options. Legitimate customers pay for it when there are false positives.

The bigger issue is where that investment is headed.

51% are prioritizing AI and machine learning. But ultimately, these are just tools.

If you're feeding them the wrong data, the best model in the world won't get you to the right results.

The focus should be on the data. Having the right signals. Precise ones, grounded in continuous verification rather than point-in-time checks.

Link to full report: https://t.co/cooz0sWh8M

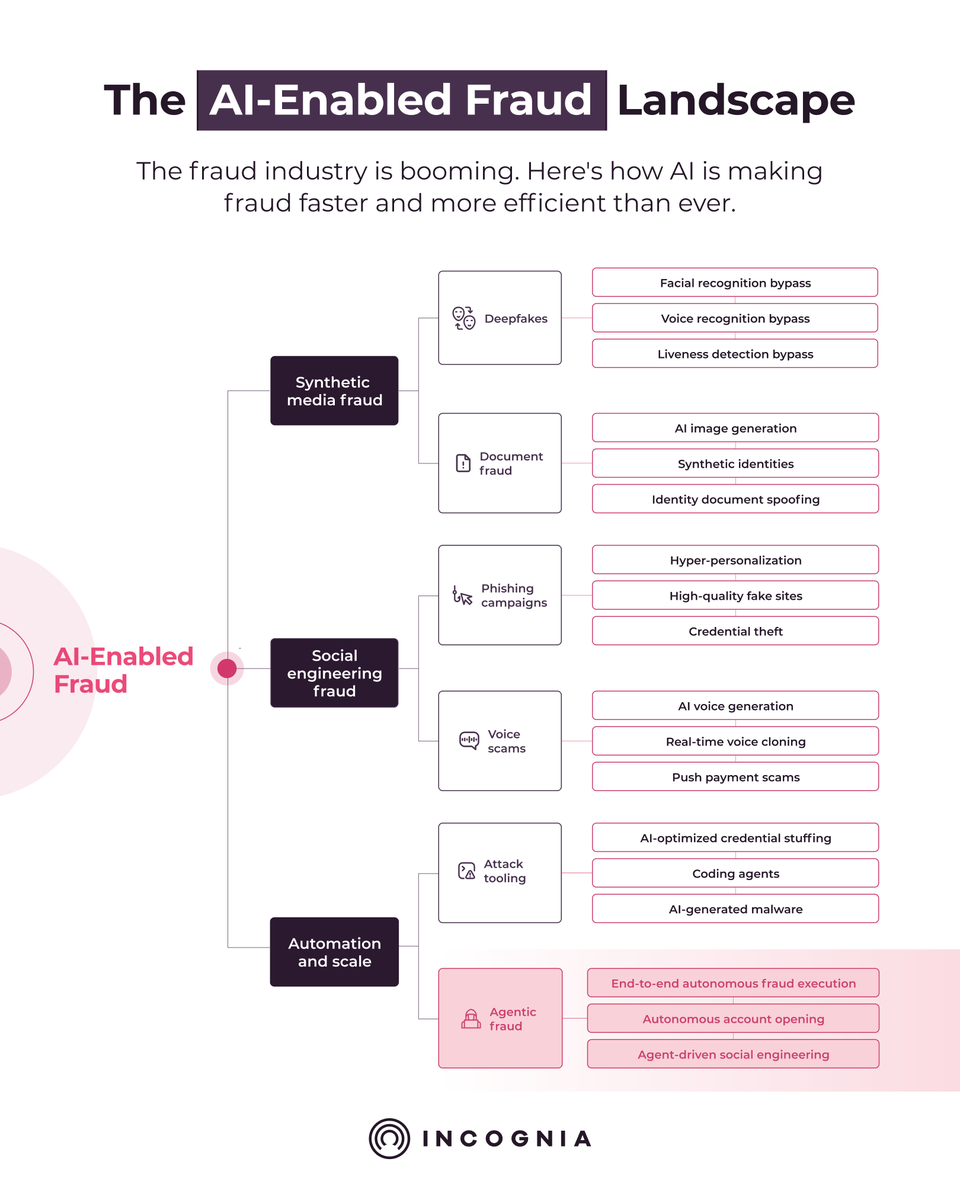

When I think about AI-enabled fraud, I see three main categories:

1️⃣ Synthetic media fraud

→ Using AI to generate fake images, videos, documents, and audio that pass identity verification

Fraudsters can already access massive datasets of stolen PII from breaches and social media. AI takes that real data and produces fake documents that look legitimate.

Photos taken from social media become inputs for video generation. The model turns left, turns right, blinks on command. The output passes liveness detection. Voice recognition gets bypassed the same way.

2️⃣ Social engineering fraud

→ Using AI to make scams more convincing, more personalized, and easier to scale

Phishing used to be obvious with bad grammar and generic messages. Now, GenAI enables hyper-personalization at scale. Messages that match the tone of your actual bank. Fake websites built in hours.

Voice scams are scaling the same way. AI voice generation and real-time cloning let fraudsters impersonate bank representatives autonomously. No call center needed. Spoof the number, sound legitimate, and push payment scams follow.

3️⃣ Automation and scale

→ Using AI to accelerate fraud operations, from writing attack scripts to running end-to-end autonomous fraud campaigns

Coding agents let fraudsters vibe code fraud-as-a-service tools on demand.

A device farm kit costs about $100. Ten phones, app cloners on each, a hundred instances running in parallel. Thousands of fake accounts per day.

When devices get blocked, automated resets generate fresh device IDs. Attack again with what looks like a new device.

And then there’s agentic fraud.

As consumers delegate tasks to AI agents, those agents become a new attack surface. Stolen credentials instructing agents. Compromised payment data placing orders. The agent does what it's designed to do. Just not for the right person.

—

Any verification built on digital signals alone is living on borrowed time.

AI can fake pixels, but it can't fake physics.

Every user interaction still happens from a physical device. That device is always somewhere in the physical world.

A fraudster can clone your voice. Deepfake your face. Steal your credentials. But they can't be in two places at once. They can't fake months of consistent behavioral patterns at scale.

The physical world will be the only ground left to stand on.

You can't trust pixels anymore.

This deepfake has 10.1M views on TikTok. 775k+ likes. 20k+ saves.

People in the comments are questioning whether the original person in the video is even real.

And the creator sells a course teaching anyone how to do this. For less than $20.

When viewers can't tell what's real in a TikTok made for fun, what happens when that same technology is pointed at your identity verification flow?

I had a meeting this week with a large crypto exchange company.

Their number one fraud problem right now?

Deepfakes.

A lot of teams are aware this is a problem. The question is whether they're moving fast enough.

AI tools are getting cheaper, faster, and more accessible every month. What a skilled engineer could do two years ago, a teenager with a laptop can do today.

Selfie-based verification, facial recognition, video liveness checks. All of these assume that what the camera captures is real. And fraudsters are proving that assumption wrong every day.

If your fraud stack relies solely on what a user looks like on screen, it's already vulnerable.

Identity has to be grounded in physical reality.

A deepfake can convincingly replicate a real person. It can't replicate where a device physically is or how it's behaved over months at scale.

81% of fraud and risk professionals say mule account handovers increased over the past 12 months.

By the time most institutions catch them, the damage is already done.

Only 16% catch handovers proactively.

On April 30, I'm joining Dave L. from Danske Bank, Dwayne Gefferie, and The Paypers to unveil the findings from Incognia’s 2026 State of Mule Account Handovers report—a survey of 500+ fraud, risk, and AML professionals across the US and Europe.

We'll cover:

→ The scale of the problem and which institutions are most exposed

→ Where detection signals are falling short today

→ What the institutions catching it early are doing differently

Link to register: https://t.co/IsBpHFrFL2

83% of mule account handovers are caught too late.

The account started clean. The real person opened it. Passed KYC. Built a history. Then handed it over, willingly.

No breach, no stolen credentials.

The identity was always legitimate.

We wanted to understand how fraud, risk, and AML teams across the US and Europe are actually approaching mule account handovers: what signals they're using, where detection is breaking down, and what they plan to do about it.

So we surveyed 500+ professionals at financial institutions to find out.

A few things stood out:

→ Detection is mostly reactive, and institutions know it

→ The data being used to catch handovers isn't reliable enough

→ Teams are organized in silos that miss the full picture of the user journey

→ The planned investments don't match the actual problem

Full report drops next week, April 30th.

Sign up for first access → https://t.co/3arSITlrqH