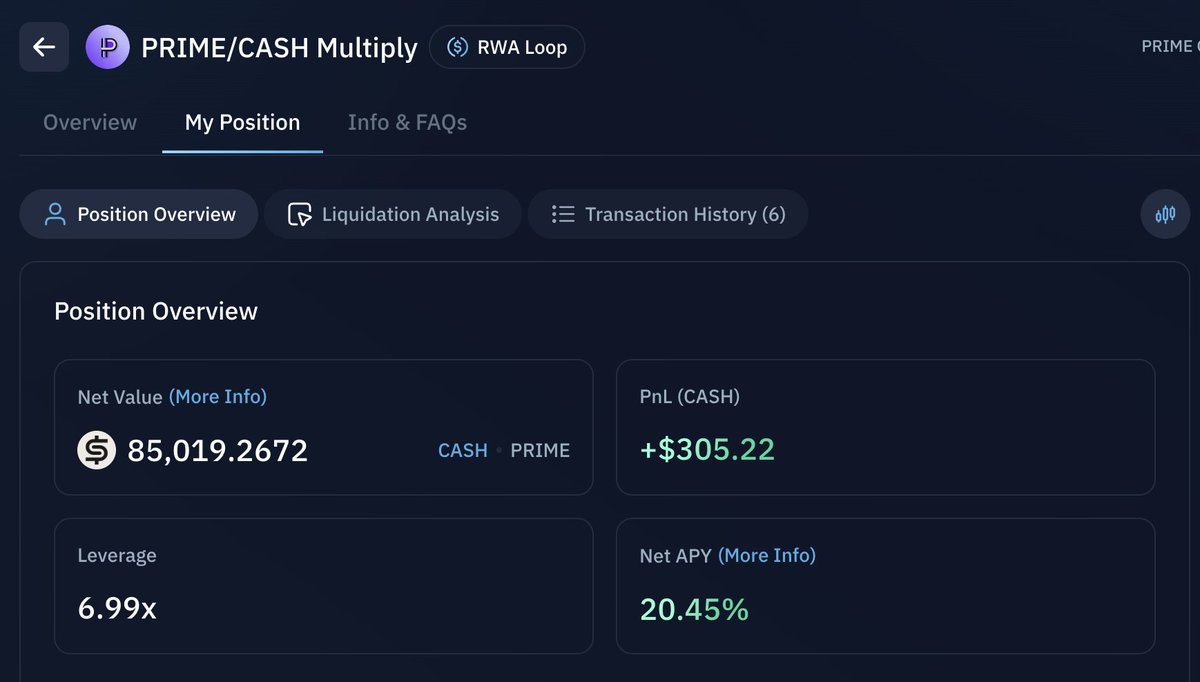

3 days ago I put ~$84.7K into the PRIME/CASH Multiply Loop on @kamino before the pool capped.

Across those 3 days the position generated:

• $305.22 in PnL

• $51 in $CASH rewards

~$120/day.

51.7% APR.

On a stable loop.

• $CASH is a stable-coin.

• PRIME is even simpler: its yield comes from real borrower interest on real Figure-originated loans (HELOCs and other consumer credit).

Clean on-chain access to traditional credit cashflows.

A loop built on a stablecoin and an RWA yield source backed by actual borrower payments is about as close to “institutional-grade safety” as DeFi gets.

Kamino Swap is the most advanced swap aggregator on Solana.

10 routes aggregated, RFQ, active price simulations.

And, of course, zero fees, hidden or otherwise.

September 19-26 liquidations update:

Some stats:

- 1773 liquidations, 580 loans, 88 liquidators

- $5.8m collateral redeemed

- 0.12% avg. liq bonus* as % of collateral (all loans)

- 0.07% avg. liq bonus as % of collateral (SOL loans)

As one of the more painful events of the last few months, I am pleased to say that the liquidator infrastructure performed extremely well once again with very little pain to the borrowers while giving lenders peace of mind.

First things first, this was a brutal drawdown as we fell from the DAT narrative peak, but, in reality the smallest drawdown of this bull (-24%).

The liquidation infrastructure and the liquidation participation in Kamino looks really competitive - 88 wallets participated in liquidations with extremely quick responses (measured as % from liquidation point).

This week is an extremely illustrative example of why liquidating more at once (higher close factor) is better for the borrower. As we are standing at the bottom of the recent range, having liquidated loans when SOL was $240 means they sold the top and lost much less capital.

On the other side, health-based liquidation bonus ensured that liquidators showed up to offer peace of mind to lenders. In practice, a health-based liquidation bonus acts as an auction - making the process competitive but not unprofitable, just the right balance to ensure liquidators do show up. This competition for liquidations makes it better for both borrowers (low bonus) and lenders (high availability).

Finally, a view on how the liquidation bonus was calculated between collateral types:

SOL collateral ->

All collateral ->

Overall, looks extremely good and this is even before more updates, currently being tested in our staging environment, are pushed.

I keep thinking of the best way to run liquidations that achieves the best outcome across a set of dimensions: borrower relief, lender peace of mind, liquidator availability and speed, across all scenarios - small dips and heavy fast drawdowns - and I think health-based bonuses on partial liquidations is one of, if not the most, optimal method.

As a SOL bull this was personally painful, but most people had partial soft unwinds to their position at elevated prices.

(*avg liq bonus means the liquidation bonus paid at that liquidation event as % of the total collateral of the position)

On fuzzing / property based testing:

- There is something special about just throwing thousands and thousands of inputs at a function and seeing that it works well.

- It’s the Proof of Work equivalent of Formal Verification

- Few things are as satisfying as increasing the number of iterations on generative property based tests and coming up with invariants to assert.

- Without the property based tests libraries, I probably would have never fully switched to Rust, years ago. Weird inflection point.

Anyway, this analysis brings me a lot of joy.

Check out the results 👇