Last week, @eddymyer_ and I launched MWP Partners, an investment firm centrally focused on conviction investing in the SMID, growth and venture.

A long time in the making, but very much the start line of an exciting journey. I will (endeavour) to share updates on our strategy, philosophy and specific investments ideas here.

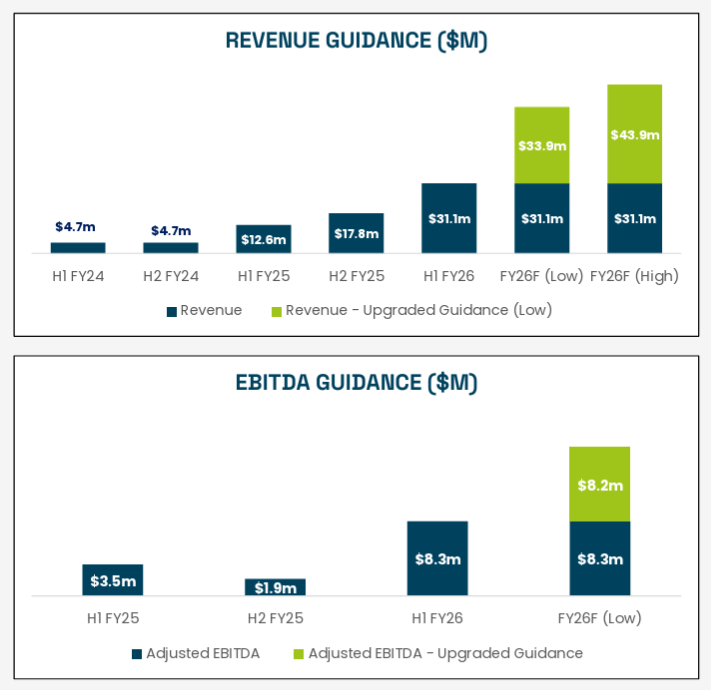

Core position $BXN.AX growing its top line +149% Y/Y for the first half and only in its first 12mo of entering new European markets. Upgraded guidance implies only 5.6x EV / EBITDA (midpoint of FY26 guidance) even after today's small bounce. North American peers trading at double or triple the multiple with lower or negative growth / loss making...

This news is transformational with the precedent in Tasmania (NSW is 15x larger) showing a 7-fold increase in prescription cannabis following the rule change. Huge tailwind for Bioxyne, who manufactures ~40% of Australian medicinal cannabis

https://t.co/BJk9SUpQbP

Great piece from @alex_gluyas at the @FinancialReview telling @michaelfrazis story in full. A genuine reinvention, not just a recovery. Clear example of the mental agility and intellectual honesty necessary to thrive. The numbers speak for themselves. Follow the journey with the recently launched ETF ticker $ROAR.AX

https://t.co/zzGvYHNVMm

@SteveSilver18 Function of three things: PolyNovo is under-penetrated in the US vs peers, there is a lag as new sales staff take ~12mo to become efficient and not all new hires work. Its most mature market Australia reaccelerated to >50% growth for instance in 1H26.

The squeeze looks like its taking shape with $PNV up +18% with a mere 5.8m share traded.

I don't know what assumption to make of short covering volume. ~50% should be conservative. So still at least ~97m shares sold short requiring ~200m shares of trading to fully cover.

The pathway for young Australians to make money is moving offshore. Even just for 5-10 years, this can have a material impact on the start of your compounding journey. Not to mention the benefits of culture, travel, character, network.

@0xgoobinat0r At 90% gross margin (~95% normalised for inventory build) the bridge isn't drastic. 50% operating margins is at maturity / cashflow harvesting mode. So mature sales (and headcount growth) and limited to no incremental R&D.

Applying a 25x operating profit multiple to our base case — not aggressive for this margin profile and growth trajectory — we arrive at approximately 150% upside over three years.

We know this company, its product, and its history. We have sized accordingly and with conviction. (14/14)

This is not financial advice. We are invested in $PNV.

💰 The opportunity from here

$PNV should be capable of 50%+ operating margins at scale, vs sub-10% today. That gap reflects deliberate reinvestment in sales force and R&D.

On FY26 revenue of ~A$155m, a 50% margin = A$77.5m operating profit against an EV currently below A$700m.

That's <9x potential earnings power — before new products or regulatory approvals. (13/14)