IC Electricals- Applying with full force as valuations & manufacturing business is attractive as company is having inhouse R&D (cheap valuation (12.82 P/E @Fy26)

What caught my attention is manufacturing business of IC Electricals.

It's the product portfolio:

• Vigilance Control Devices (driver safety systems)

• Battery Chargers

• ERRUs (coach power management)

• Passenger Information Systems

• Alternators & Rotating Machines

• Railway Electronics Manufacturing

On Railway Electrification the Growth ahead depends on:

🔧 OHE renewal/replacement (recurring)

🚄 New line construction (still electrified from day 1)

⚡ Rotating machines & railway electronics (separate vertical, 24+ products)

Export Opportunity- Where there's a real future angle (not now, but plausible):

Nepal, Bangladesh, Sri Lanka run similar broad-gauge, 25kV AC systems close to Indian Railways specs — lowest-friction export corridor if IC Electricals ever pursues it.

Africa's railway modernization (funded by Indian EXIM Bank lines of credit, e.g., Mozambique, Tanzania) sometimes pulls in Indian railway-equipment vendors as part of government-to-government deals — worth watching, not underwriting.

#ICElectricals #IPO

One pager Growth catalysts summarised for Ather Energy

Key triggers include doubling the capacity in H2 of this year and the launch of mass product platform EL .

Disc : Not a buy sell recommendation

Data sourced using @stockscansin

A very good article on building water security in a drying India.

Why Monsoon can't alone solve this crisis?

Important points highlighted as well as shared as short notes

This slide contains the growth plans of key metal recycling companies across copper, lead & aluminium segments

Pondy Oxides, Gravita India, Jain Resource, Baheti Recycling & CMR Green are moving towards value added products, backward integration, downstream manufacturing & higher margin segments

src : Markets by Zerodha

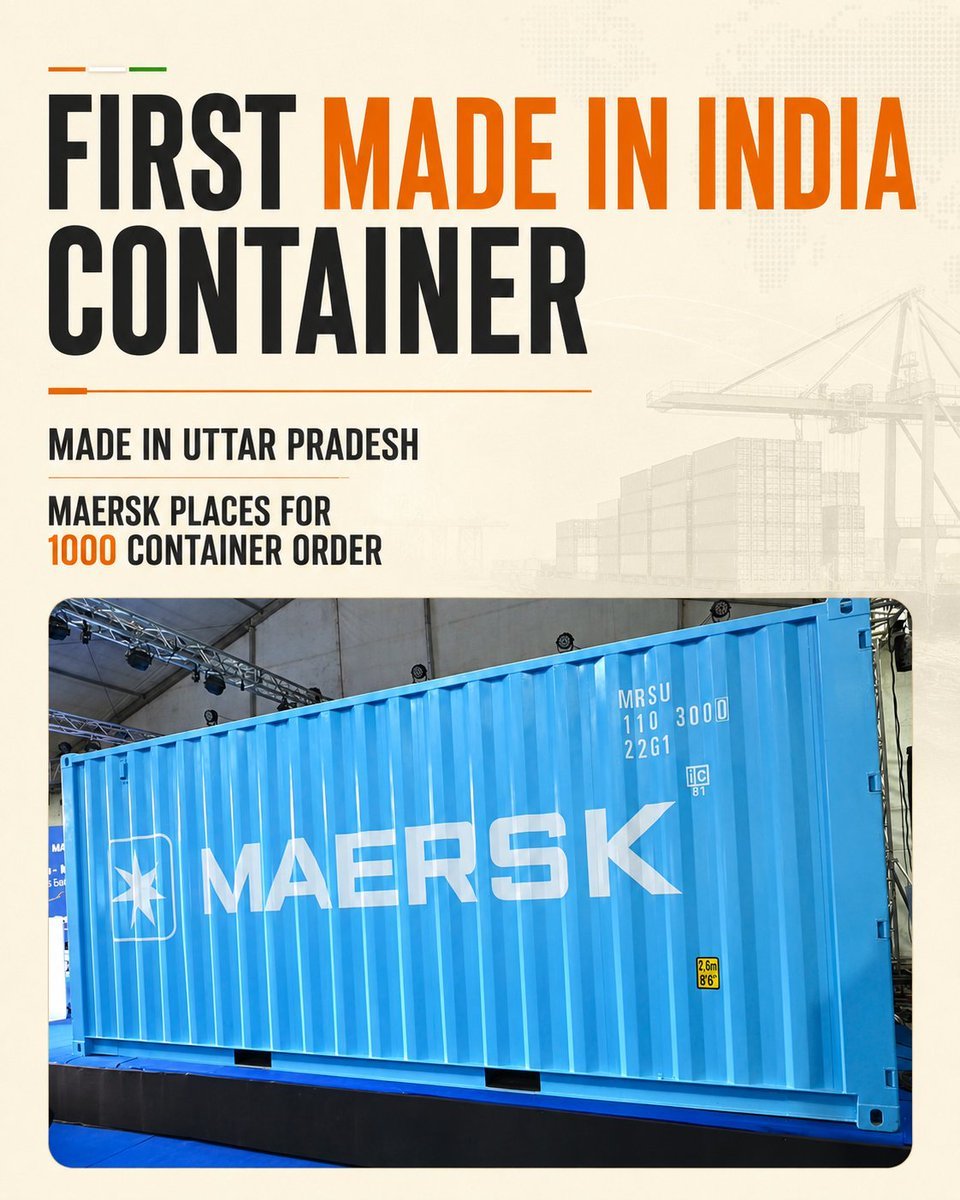

First Made in India container - Made in Uttar Pradesh

India Takes a Major Step Towards Maritime Self-Reliance with First Made-in-India EXIM Shipping Container

Maersk places a 1000 container order

Part of the ₹10,000 crore Container Manufacturing Promotion Scheme (CMPS) framework announced in the Union Budget 2026 for domestic container manufacturing

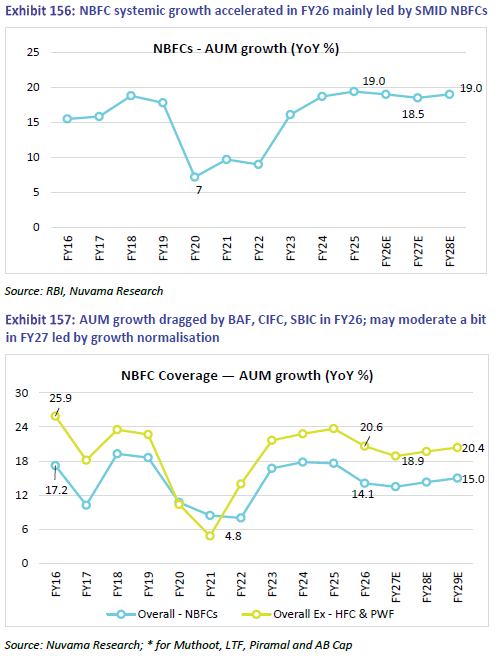

Nuvama take on NBFC

Over the past 3 years NBFC has outperformed banks due to strong credit growth, falling funding cost, margin expansion, improved asset quality and turnaround stores of companies like L&T Finance, AB Capital and Piramal Finance.

Nuvama believes the biggest earnings tailwind is fading because of rate-cut cycle largely over, cost of funds increasing, money-markets are rising.

Nuvama expects FY27 NBFC credit growth around 18.5% (vs ~19% in FY26). Companies will prioritize asset quality and profitability over aggressive AUM growth.

P2P comparison: FY27 P/B

=> Shriram Finance: 2.2X

=> AB Capital: 1.7x

=> Piramal Finance: 1.6x

=> MMFSL: 1.5x

Follow @DhawalDoshi5 for more updates

Source: Nuvama Research

@vishan_29@Anvith_@TrendSpark420@tirthankardas81

Reading this excellent report on EV component manufacturing localisation in India by @ieefa_institute. The report suggests that powertrain, power electronics, and charging equipment could reach 90–100% localisation by 2030. But rare-earth supply, permanent magnets and semiconductor bottlenecks persist, and will continue to limit domestic value addition unless local manufacturing is established.

The report is very well researched and has brilliant figures and tables for EV manufacturing aficionados.

Source: https://t.co/Sj74Mvv0AT

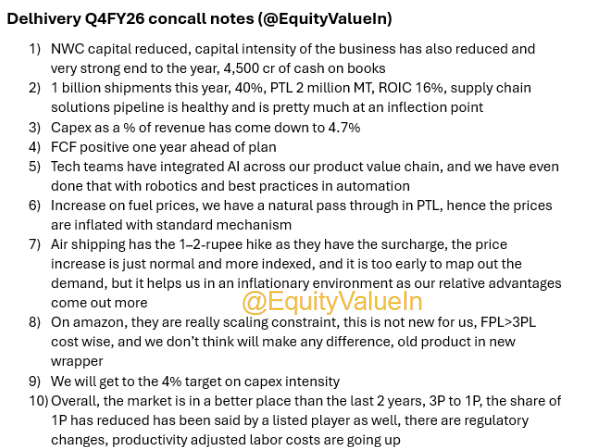

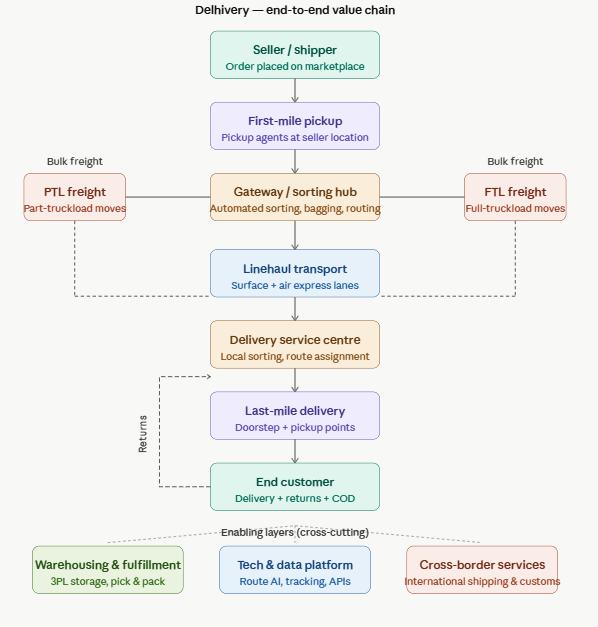

Delhivery value chain , mapping the business and also my recent quarter concall notes , one of the very focused managements out there

disc: biased , so no reco , no advice

15 stocks with very bullish concalls which can double PAT in next 2-3 years:

🔹1. Kirloskar Pneumatic (#KIRLPNU): 20% revenue growth and PAT growth guidance in FY-27 and beyond

🔹2. Aditya Infotech (#CPPLUS): 50% revenue growth in FY-27 (6000-6500 cr revenue in FY-27)

🔹3. GNG Electronics (#EBGNG): 25% revenue growth with 50 bps margin expansion in FY-27

🔹4. APL Apollo Tubes (#APLAPOLLO): 15-20% volume growth and 25-30% PAT growth guidance in FY-27

🔹5. Apex Frozen Foods (#APEX): 30% volume growth in FY-27

🔹6. Aris Infra (#ARIS): 35-40% revenue growth in FY-27

🔹7. Astra Micro (#ASTRAMICRO): 15-20% revenue growth in FY-27

🔹8. Credit Access Grameen (#CREDITACC): 20-25% AUM growth in FY-27

🔹9. AWFIS Space Solutions (#AWFIS): 25-27% revenue growth in FY-27

🔹10. Aye Finance (#AYE): 25-30% AUM growth in FY-27

🔹11. Azad Engineering (#AZAD): 25% revenue growth in FY-27

🔹12. Bansal Wires (#BANSALWIRE): 20% revenue and EBITDA growth in FY-27

🔹13. Cera Sanitaryware (#CERA): 20% revenue growth in FY-27

🔹14. Deep Industries (#DEEPINDS): 25-30% revenue growth in FY-27 and FY-28

🔹15. Gala Precision Engineering (#GALAPREC): 20-25% revenue growth in FY-27 and beyond

A lot of investors get excited when a stock is down 40-50%.

I get curious when a stock is close to its high & the business is still improving. Majority of times the potential winners clearly start showing signs of strength. Sharing these 12 smallcap #Stocks that I am studying. Worth tracking.

• SPARC : ₹239

PE 5.0, PEG 0.05, ROCE 165.0%

• Modison : ₹340

PE 14.0, PEG 0.17, ROCE 30.9%

• Indiabulls : ₹27

PE 19.5, PEG 0.39, ROCE 16.2%

• Kernex Microsys : ₹1,980

PE 37.6, PEG 0.44, ROCE 47.8%

• Cemindia Project : ₹1,259

PE 36.7, PEG 0.54, ROCE 32.8%

• Rashi Peripheral : ₹757

PE 18.0, PEG 0.58, ROCE 16.8%

• Modern Insulator : ₹493

PE 29.1, PEG 0.68, ROCE 19.4%

• GNG Electronics : ₹519

PE 44.8, PEG 0.76, ROCE 20.3%

• Vidya Wires : ₹111

PE 40.8, PEG 1.05, ROCE 20.7%

• Rishabh Instrum. : ₹582

PE 27.6, PEG 1.35, ROCE 14.5%

• Aeroflex Enter. : ₹146

PE 25.5, PEG 1.45, ROCE 12.6%

• ADF Foods : ₹316

PE 36.6, PEG 1.77, ROCE 22.8%

One Pager on Three Interesting Data Center proxies:

Kirloskar Oil Engines: manufactures diesel gensets, industrial engines. Growth driven by 2100cr capex, nuclear genset order, and HHP sales. secured a 192MW data centre genset supply order.

Clean Max: India's largest renewable energy provider, Data center contracted capacity grew 10x to 2,400 MW in two years. Over 2-3 years, the company will execute 2,600 MW under construction, expand Datacenter exposure, and reduce leverage costs to 8.5%

Venus pipes: Manufacturer of stainless steel seamless and welded pipes. Expanding into higher margin value added products like fittings and condenser tubes. 20% revenue growth for the next two years. 185cr LOI for a liquid cooling fluid network from data center operator.

Curated a list of 25 companies that can double their PAT in next 2-3 years

Sharing free 12-15 page Research reports on each for further research.

https://t.co/SWWc7bQfqA

One Pager on Three Interesting Stocks from the List:

Azad Engineering: Turbine blades for gas turbines. Scaling aerospace segment, supplies APUs, landing gear actuators. LTAs with rolls-royce, safran for engine components.

Kirloskar Oil Engines: manufactures diesel gensets, industrial engines, and energy transition products for power generation, defense, and infrastructure. Growth driven by 2100cr capex, nuclear genset order, and HHP sales.

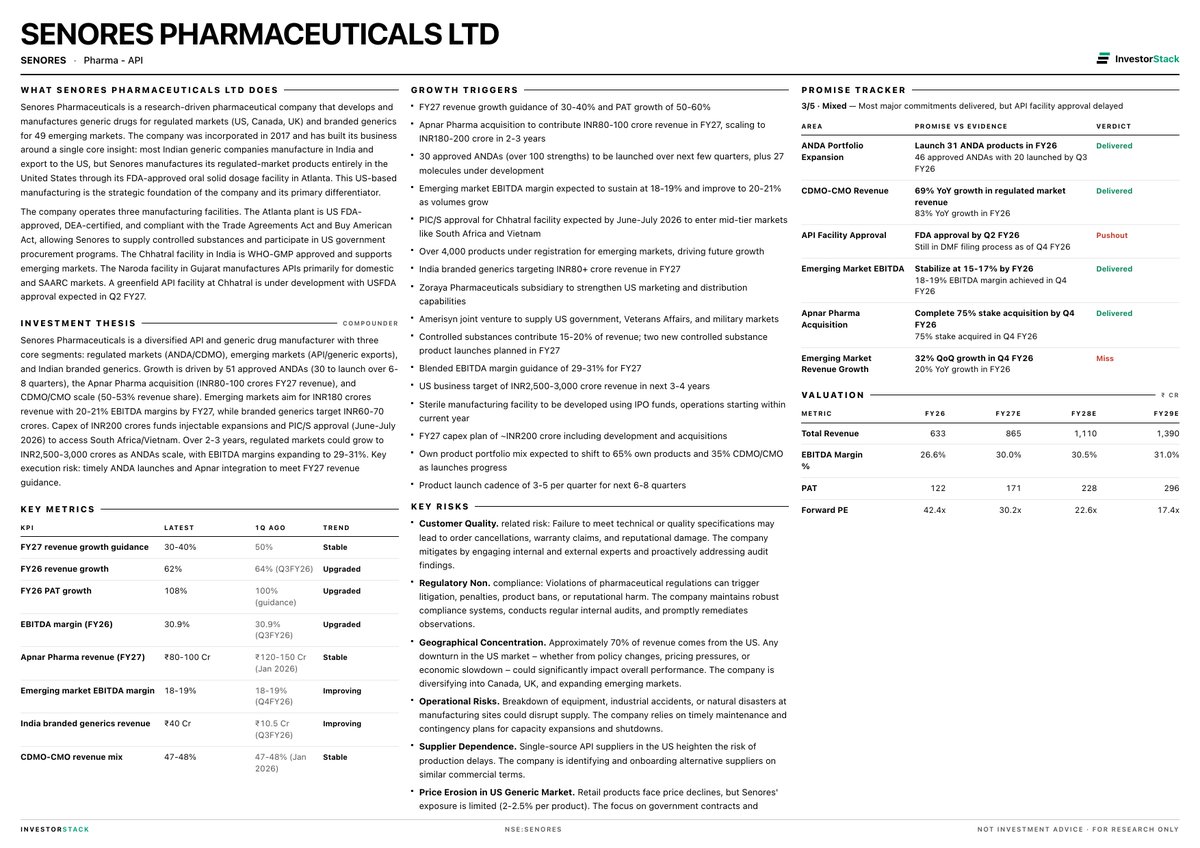

Senores Pharma: API and generic manufacturer with three core segments: regulated markets, emerging markets, and Indian generics. Growth is driven by 51 approved ANDAs (30 to launch over 6-8 quarters), Apnar Pharma acquisition, and CDMO/CMO scale. Over 2-3 years, regulated markets could grow to 2,500-3,000cr as ANDAs scale, margin expanding to 29-31%.