📢Alert: Seasonality Strategy (With Code)

Santa Claus Rally 🎅

Is a well known and documented effect in indices across the globe.

Rules:

Long 5 Days before End of Year.

Exit 2 Days into Jan.

Here I explore multiple combinations of entry exit on NIFTY/BANKNIFTY 👇

Retail/semi-pro would be better off if they spend their mental bandwidth and energy on understanding source of P/L. What makes money for them and why.

They get paid because they take a risk.

Edge isn’t time of day, super indicator, trading parameters or tech latency.

One of the biggest challenges in retail algo trading has always been market data latency. Even the best broker feeds often came with delays of up to a second.

Access to a faster feed can be a genuine game changer for retail traders and developers building execution-sensitive strategies.

Really impressed by what the Arrow team has built @vivbajaj 👏

Link below:

@GoldenDustbin Your edge isn’t sensitive to latency. Unless you have quantified it to be, which I wouldn’t know of.

Most of the source of PNL is risk Premia and statistical analysis. None of which is really dependent on latency.

And thus latency induced PNL is noise. It washes off.

@Souvik131 You’re not retail. Vast majority of retail has no reason to be trading less liquid tickets on SSO. You have every use for latency sensitive.

This Hollywood Boulevard, one of the most iconic and busiest streets in Los Angeles.

You can see a group of American tourists dancing for a reel bang in the middle of the road.

But no one is going to use racist remarks against them. That's reserved only for Indians enjoying tourist spots.

Some part of me is internally happy that AI tools such as Claude or Codex have made backtesting so easy.

I just hope a high percentage of such traders start putting their alpha systems to trade in live markets.

#congestion

@airindia your rude and impolite staff ensured that the infant and his grand parents were separated on a flight. That too when we paid for business class tickets.

What kind of horrible air crew do you employee who forces this?

@airindia What is your policy around an infant on a business class ticket crying on board? Your crew seems to be suggesting that infant be moved to a lower cabin along with the mother because “other passengers are getting disturbed due to the infant”. On a god damn long haul flight.

Is this how Air India cares for families with infants? Is that how @TataCompanies values and ethos are upheld?

@the_avid_trader@airindia There are two levels of absurdity in this.

1. A passenger complaining

2. The crew using it as a crutch to harass on flight.

I’ve had much better experience with some of the other airlines.

@airindia What is your policy around an infant on a business class ticket crying on board? Your crew seems to be suggesting that infant be moved to a lower cabin along with the mother because “other passengers are getting disturbed due to the infant”. On a god damn long haul flight.

Is this how Air India cares for families with infants? Is that how @TataCompanies values and ethos are upheld?

Mock foodpharmer all you want but a part of this change has to be credited to him for making people aware of what they are consuming. Else nobody would have given a rats ass about consumer benefits

@livelearnadd True edges are usually fleeting. More traders discovering the same edge leads to crowding and degradation.

Statistical edges would be cyclical anyways. They don’t always show up.

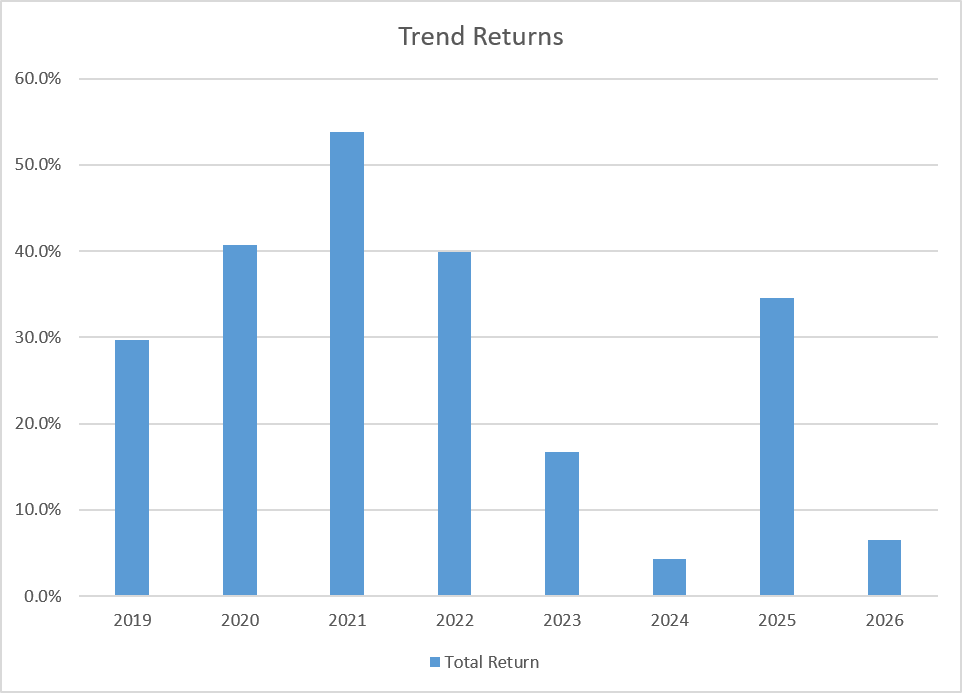

A trend strategy that annualizes 34% return went through following on an yearly basis. Assess when would you quit if you started after '21.

Linear P/L only exists in backtests and usually has hidden risks. Risk premias do not go away, and its important to distinguish between an eroding edge vs cyclical under-performance of risk-premia.

That’s a good frame to think through.

One way to think about is what’s a risk premia and what’s an edge. Risk premia persist through time and cycles.

Equity risk premia, vol risk premia, skew risk premia, etc. And there are many ways to harvest these.

Edge can be under two categories, and they both can erode when market evolves.

1. Market inefficiencies that you identified.

Forced market behavior around certain events/periods, Statistical edges, inefficient price discovery, regulatory constraints driven behavior, are a few examples.

2. Enhanced Risk Premia.

Small/weak effects that on their own wouldn’t classify as useful. But when overlayed with an existing Premia might improve risk adjusted performances.

That’s a good frame to think through.

One way to think about is what’s a risk premia and what’s an edge. Risk premia persist through time and cycles.

Equity risk premia, vol risk premia, skew risk premia, etc. And there are many ways to harvest these.

Edge can be under two categories, and they both can erode when market evolves.

1. Market inefficiencies that you identified.

Forced market behavior around certain events/periods, Statistical edges, inefficient price discovery, regulatory constraints driven behavior, are a few examples.

2. Enhanced Risk Premia.

Small/weak effects that on their own wouldn’t classify as useful. But when overlayed with an existing Premia might improve risk adjusted performances.

@drrizzz Agree. But the point here wasn’t about just trend. It was about variability of returns when sampled even at yearly frequency. And that can happen with many strategies.

Traders are focusing on the annualized returns, and missing the whole point about this tweet. The actual returns are irrelevant here. The message is to understand variability in yearly performance that may prompt you to take a decision to stop a strategy.

A trend strategy that annualizes 34% return went through following on an yearly basis. Assess when would you quit if you started after '21.

Linear P/L only exists in backtests and usually has hidden risks. Risk premias do not go away, and its important to distinguish between an eroding edge vs cyclical under-performance of risk-premia.