Conducts research and publishes educational reports and investigations to inform the public about government accountability and efficient use of taxpayer funds

@ForwardCarolina@SonSquirrel It's not a surge in personal net worth.

It's a number taxes are based on.

A higher assessed value only increases your net worth if someone is writing you a check.

The question is whether local governments should collect 19-20% more property tax revenue

@ForwardCarolina Then how about reporting the truth as property tax increase percentage instead of the misleading stuff about rates?

Greensboro has/had a 21% property tax increase.

Why not tell the truth?

@ForwardCarolina County A has a tax rate of 75¢ per $100 on a $150,000 home Tax bill = $1,125

County B has a tax rate of 50¢ per $100 on a $500,000 home Tax bill = $2,500

County B has the much lower tax rate, but the homeowner pays more than twice as much in taxes.

@ForwardCarolina A low tax rate does not necessarily mean low taxes. A high tax rate does not necessarily mean high taxes.

Property tax is calculated as:

Tax Bill = Property Value × Tax Rate

When property values rise dramatically, taxpayers can pay substantially more even if the tax rate falls

Property Tax Reappraisal Bill 889 Passes NC House by Veto Proof Majority; Guilford and Greensboro May Have to Wait to pass 19% and 21% Tax Hikes as Now, They Can't Lie by Omission With the Help of our Local Compromised Press

According to the Washington Post’s @DanLamothe, the U.S. Navy drone that aided in the rescue of two U.S. Apache helicopter crew members was a Saronic Technologies Corsair unmanned surface vessel (USV). First deployed in the U.S. Central Command AOR in March of this year, the USV reportedly picked up the two soldiers and then took them to a secondary location where a waiting helicopter hoisted them up. Such a rescue would be the first time that such a system was used in this role.

Milton Friedman's greatest regret.

The federal government discovered the perfect crime in 1943: make employers collect taxes before workers ever see their paychecks. You think you earn $60,000 per year, but you actually earn $75,000 and hand over $15,000 to politicians without ever touching it. The psychological difference is enormous.

Before payroll withholding, Americans wrote quarterly checks directly to the Treasury. Picture yourself sitting at your kitchen table, writing a $3,750 check to the IRS every three months. The pain was immediate and visceral. Politicians faced constant pressure to justify every dollar because citizens felt the extraction in real time.

Withholding transforms this concrete loss into an abstract accounting entry. Your employer becomes an unpaid tax collector, and you never experience the actual cost of government. Worse, most people celebrate their tax refunds as government generosity rather than recognizing them as interest-free loans they provided to politicians. The Treasury collects your money throughout the year, spends it immediately, then returns your own cash and receives gratitude.

This system enables the explosion in government spending you witness today. Defense contractors billing $640 for toilet seats, agricultural subsidies for corn syrup, and congressional salaries for 535 people who rarely show up to work. When taxation feels painless, voters stop demanding accountability for how their money gets spent.

Milton Friedman helped design withholding as a wartime emergency measure and later called it his greatest regret. Free market economists recognized that the psychological pain of direct taxation creates political pressure for fiscal restraint. The temporary always becomes permanent in government hands, and the emergency justification disappears while the extraction mechanism remains forever.

North Carolina is projected to be more than 750,000 homes short of our housing needs in just three years. People want to live and work here, but we simply don’t have enough homes to meet the demand. @PittCC is helping to build the state’s construction workforce to meet our housing needs and expand access to good-paying jobs.

North Carolina is projected to be more than 750,000 homes short of our housing needs in just three years. People want to live and work here, but we simply don’t have enough homes to meet the demand. @PittCC is helping to build the state’s construction workforce to meet our housing needs and expand access to good-paying jobs.

FT: "Goldman Sachs analysts are predicting total US equity supply of $1.175t in 2026, consisting of $225b of IPOs, $450b of other corporate stock sales, and another $500b gradually dribbling out from corporate executives and early investors in the IPOs...This has understandably led to fears that the market could suffer severe indigestion. Even one of these big IPOs could be enough to cause a mild case, but the combination could prove painful. That big IPO years tend to presage big downturns has exacerbated those concerns."

As I dissected in my February report on "Price Discovery" (https://t.co/kEx5Z4BJH7), relative market resilience since the GFC has been in part predicated on passive investing reducing equity supply against persistent demand. Less AUM in the hands of active managers means fewer shares traded based on price moves. Meanwhile, passive flows have stayed constantly positive. This has reduced the elasticity of stocks. To quote an Economist recap of one study into this:

"The paper, by Xavier Gabaix of Harvard University and Ralph Koijen of the University of Chicago, sets out their 'inelastic-markets hypothesis.' This contradicts the textbook argument that money flowing into stocks should barely raise prices, since if it did, demand would fall and return prices close to their starting level. In fact, the paper’s authors find that stock market demand is not 'elastic' in this way. It is inelastic, and does not fall much as share prices rise. As a result, an investor who buys $1-worth of stocks using fresh cash (or the proceeds from selling other assets such as bonds) pushes up aggregate market value by $3-8…Most important, funds that maintain fixed allocations can push up prices. Suppose you exchange cash for new units in a fund promising to keep 80% of its assets in shares. The number of shares in existence does not change, but demand for them has risen. The fund can buy shares from another type of investor, but in practice flows between investor groups are low. (This also implies inelasticity, since if demand were elastic, groups with different beliefs, about future earnings, say, would act differently, boosting trading.) The only way to put the cash to work, if all similar funds are to also meet their mandates, is to buy fewer shares at a higher price."

Which, of course, begs the question: what will a flood of new supply mean if demand doesn't spike to meet it. Difficult question to answer given we've not seen an IPO wave of this scale at a time when passive vehicles control this much AUM. I'll be digging in for answers in the days and weeks to come. But as I warned in the report: "The benefits of inelasticity on the upside could do the equal and opposite on the downside."

Learn more about Sage Road Research here: https://t.co/Wgwz2xnvR6. Interested in subscribing? Message me.

FT link: https://t.co/0mb9o48ZWR

Chart of the Week - The Speculation Generation

Today’s chart is one for tomorrow’s history books.

It shows US households running the highest allocation to equities on record (and [as a result] the stockmarket trading at record high valuations).

This is the type of shift you see only once in a generation, and it means a fundamental change in market structure with significant implications for the economy, politics, and the forward looking risk vs return outlook.

But to be fair, with the S&P500 gaining more than 10x off the March 2009 lows — it’s an entirely understandable development!

And even though it got this way for very logical reasons (strong earnings growth, waves of tech disruption, low interest rates, passive flows), it’s important to acknowledge that this is not normal and we live in highly unusual times.

Investor confidence is near record highs, earnings optimism is at euphoric levels, defensives and diversifiers are in the dustbin, and social media chatter is saturated with an almost desperate sense of greed (with investors growing accustomed to 2x, 3x, 10x returns, and the bull market minting many geniuses).

This is the speculation generation.

p.s. this is neither good nor bad, it’s just a thing… and that’s the thing: as market analysts we ought to not got get bogged down in good or bad, bullish or bearish, optimism or pessimism —but rather what is the lay of the land? what does the data tell us? and what are the most pragmatic next steps we should take (or prepare to make…)

Bottom line: a generational shift in investor behavior has been observed.

🚨 Sam Altman warns OpenAi and Anthropic are experiencing severe pullback on Ai spending as companies put significant restraints on spending to restrict costs. The company warns investors it’s the first time this has happened in Ai and something we never expected. The buildout costs aren’t sustainable to allow profitability to hyperscalers or end users.

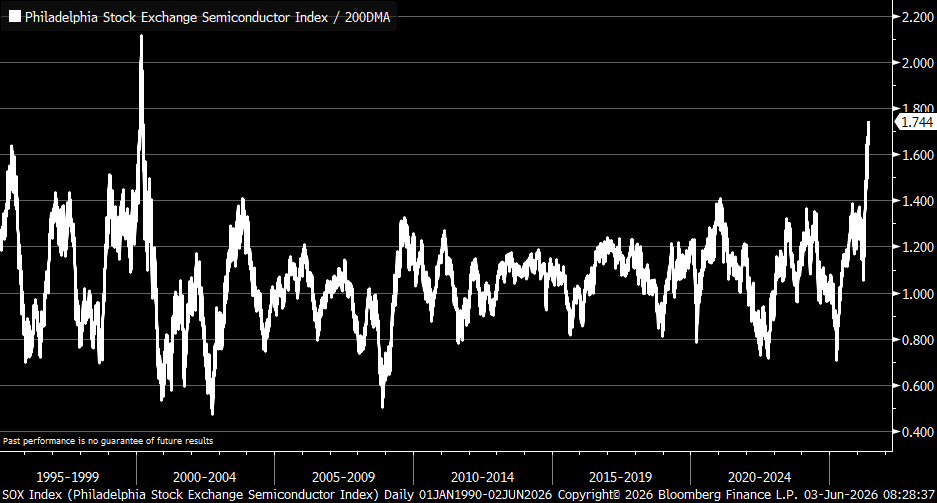

$soxx $dram

Deutsche Bank on the huge stock market run-up:

"Since WWII, the only other time the S&P 500 has risen this rapidly (except after a recession) was months before a huge market crash."

![Callum_Thomas's tweet photo. Chart of the Week - The Speculation Generation

Today’s chart is one for tomorrow’s history books.

It shows US households running the highest allocation to equities on record (and [as a result] the stockmarket trading at record high valuations).

This is the type of shift you see only once in a generation, and it means a fundamental change in market structure with significant implications for the economy, politics, and the forward looking risk vs return outlook.

But to be fair, with the S&P500 gaining more than 10x off the March 2009 lows — it’s an entirely understandable development!

And even though it got this way for very logical reasons (strong earnings growth, waves of tech disruption, low interest rates, passive flows), it’s important to acknowledge that this is not normal and we live in highly unusual times.

Investor confidence is near record highs, earnings optimism is at euphoric levels, defensives and diversifiers are in the dustbin, and social media chatter is saturated with an almost desperate sense of greed (with investors growing accustomed to 2x, 3x, 10x returns, and the bull market minting many geniuses).

This is the speculation generation.

p.s. this is neither good nor bad, it’s just a thing… and that’s the thing: as market analysts we ought to not got get bogged down in good or bad, bullish or bearish, optimism or pessimism —but rather what is the lay of the land? what does the data tell us? and what are the most pragmatic next steps we should take (or prepare to make…)

Bottom line: a generational shift in investor behavior has been observed.](https://pbs.twimg.com/media/HJ7aWwvbMAAgbF4.png)