Copper Is Getting More Expensive to Mine. 🟠⛏️

The copper bull case is not just demand.

It’s cost inflation.

From 2019 to 2025, mining costs rose sharply across several major producers:

Codelco: +46.9%

Teck Resources: +46.0%

First Quantum: +54.2%

Anglo American: +19.1%

150 Years, 22 Companies.

1 Oil Dynasty 🛢️

It started in 1870 with Standard Oil.

One refinery in Cleveland.

John D. Rockefeller.

The beginning of the modern oil empire.

What followed shaped every war, economy, and geopolitical order since

Gold miners are set to outperform

We are in the 2nd breakout of gold miners after a decade consolidation phase

-1940–1960: consolidation phase

-1960–1980: 25x return in 20 yrs

-1980–2025: consolidation phase

These breakouts after decade consolidation phases tend to be volatile

Russia is selling its gold reserves at a rapid pace:

The Bank of Russia's gold holdings dropped -900,000 ounces in the first 4 months of 2026, to 73.9 million ounces, the lowest since February 2022.

Gold prices averaged ~$4,800 per ounce over the same period.

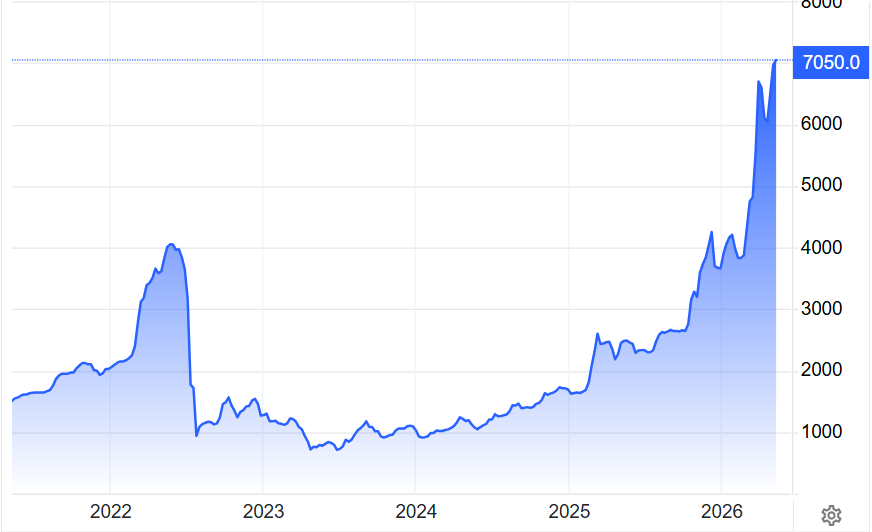

Sulfuric acid is the most important ingredient for our whole industry.

Because of Hormuz and export controls, we have lost a huge chunk of global production.

Sulfur/sulfuric acid is needed for:

Fertilizer -> food

Mining -> copper.

Water treatment

Manufacturing -> plastic.

Major US fertilizer producer Mosaic is losing money in the midst of a fertilizer crisis.

- Sulfuric acid is a major input in phosphate fertilizer production

- ~30% of global sulfur is gone due to Hormuz

- China, the #1 exporter, is banning sulfuric acid

🔴China is DOMINATING the rare earth supply chain:

China holds 44 million tons of rare earth reserves, more than DOUBLE that of 2nd place Brazil at 21 million tons.

China also accounts for ~70% of global rare earth mining, with the US a distant second at 13% and Australia at 7%

Deutsche Bank: Gold target 8,000

Emerging economies are derisking their reserves from Western sanctions

- Since 08 they've added 225 million ounces

- That's more than 2 years of global mine production

- Their dollar holdings fell from 60% to 40%

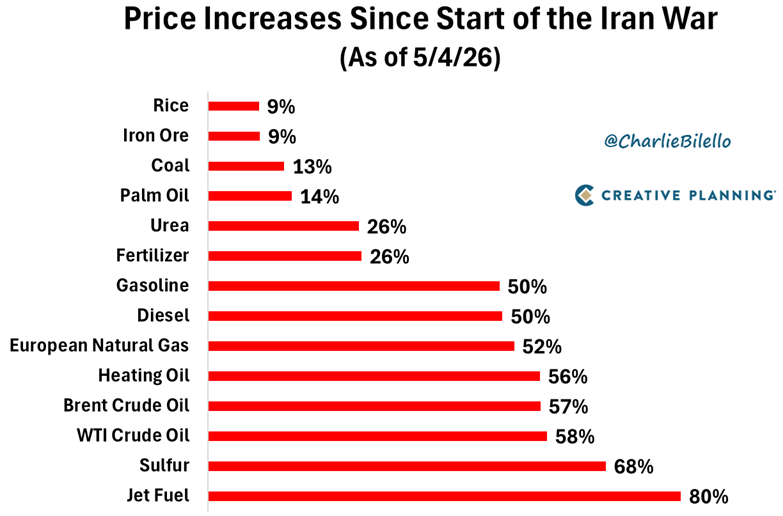

The US farming sector is in deep trouble

The biggest farming input costs are surging

- Diesel up ~50%

- Fertilizer up ~50%

This is leading to 70% of farmers not being able to buy all the fertilizer they need and farming bankruptcies were up 50% in 2025.

The energy crisis is quickly turning into a food crisis

- 30% of global fertilizer production gone

- 20% of global LNG production gone

- Fertilizer depends on natural gas

- ~50% of global food production depends on fertilizer

The world's top 25 copper miners produced this in Q4 2025.

It still isn't enough....

🥇 BHP: 490,500 tonnes down 4% YoY

🥈 Codelco: 397,076 down 3.2% YoY

🥉 Freeport-McMoRan: 290,299 down 38.5% YoY

The largest producers are all declining yoy.

🇨🇬🇿🇲🇿🇼🇲🇱The 20th century was shaped by who controlled oil.

The 21st century will be shaped by who controls cobalt, copper, and lithium.

Africa has seen this movie before... different resources, same dynamic.

🌎The world is facing the greatest demographic COLLAPSE in human history.

136 of 237 countries now have fertility rates BELOW replacement level, up from just 4 in 1950.

Replacement level is the rate needed to keep a population stable across generations.

The Strait of Hormuz closure is the biggest

Oil crisis -> transportation

Fertilizer crisis -> food

LNG crisis -> food/power

Hitting us all at the same time.

Qatar exports almost all its LNG via the Strait of Hormuz.

Goldman shows the export collapse.

Bloomberg shows the equity damage.

Qatar isn't an Iran war loser by accident it's a loser by geography.

No alternate route, no buffer.

The chokepoint is a sovereign risk factor.