50 to 200% returns. First the US market. Now Korea and Taiwan. Indian investors are paying attention.

The returns looked obvious in hindsight. They always do.

But most people chasing global markets right now are not diversifying. They are chasing returns that have already happened.

And while everyone is looking outward, here is something most foreign stock investors have not checked.

The moment you hold anything outside India, your ITR has specific requirements.

-Foreign stock capital gains are not calculated in dollars. They are calculated in rupees, on the dates you bought and sold. A depreciating rupee can inflate your taxable gain even if the stock barely moved.

-You have to mandatorily file ITR-2 the moment you hold any foreign asset. Even if you did not sell a single share this year.

-Every foreign holding goes into Schedule FA. Sold or unsold. Missing this carries a penalty of up to 10 lakh rupees per year.

Global investing is a good decision. Filing it wrong is an expensive one.

ClearTax handles exactly this with 100% accuracy, so you do not have to figure it out on your own.

Zero tax on your capital gains.

Would history repeat itself?

Yes, this actually happened just a decade ago. Zero tax on capital gains was official policy from 2004 to 2018 (14 years).

In fact, this approach goes back even further. In 1948, India scrapped this tax completely because it was hampering economic growth. The reasoning back then was that taxing capital gains could discourage market participation.

This tax relief was directly tied to market growth, giving a steady, long-term lift to overall market activity.

-Foreign capital flowed in.

-Retail investment grew.

-India became a premier destination for global finance.

Although, single factor does not explain an entire market, history does show that tax rules can directly influence investor behaviour.

Recently, the Finance Minister has stated that the government is willing to listen to investors. That is a positive step.

Right now, the rupee is under pressure. Foreign inflows are slowing. And other markets are pulling in the same capital we are trying to attract.

Do you think a policy correction is what the market needs right now?

Everyone's talking about NRIs pulling money out of India. But the data says otherwise.

Look at the latest RBI numbers.

-Total NRI deposits are stable.

NRE inflows are actually surging (USD 4.7bn → USD 7.9bn inflows) this year.

-NRO balances, which capture rent, investments, and pensions earned inside India, are all growing.

-The one category that slowed is FCNR (foreign currency fixed deposits), and even that is mostly global rate dynamics. Nothing specific to India.

There's also something else that is getting missed. NRE accounts hold rupees, but RBI reports them in dollars. When the rupee weakens, the same balance shows up as a smaller dollar figure on paper. There's no major outflow by NRIs. It's just how the number is reported.

And this matches what we see on the ground at ClearTax. Last year's NRI tax filing data showed engagement with India going up, not down. More NRIs filing returns. More buying property. More investing in Indian markets.

So the story is not about withdrawal, it's the opposite. NRIs aren't stepping back from India. They're stepping in.

People look at the new ITR forms and see compliance. I see a pattern.

-House Property now asks for co-owners, tenants, PANs, rent breakup, and interest paid.

-Donations now need transaction references, IFSC details, and in some cases, the recipient’s PAN.

-Exempt income can no longer be entered as plain text. It has to be mapped to a specific section, with tighter validation rules.

The income tax department is not asking for more data. It is asking for verifiable data. Every line in the new form can be cross-checked against someone else's filing. Your return is no longer read on its own. A file like the department already has the other side of the entry.

The PM has asked Indians to hit pause on buying gold until next year.

But Indian households treat gold differently anyway. For us, it is wedding planning, a daughter's future, an emergency fund, and passing down wealth. A spreadsheet simply cannot negotiate away a financial safety blanket.

When our high demand for physical gold started hurting India's import bill, the financial system created paper gold. Sovereign Gold Bonds launched in 2015 as the first major alternative. Over nine years, the government collected ₹72,274 crore for 146.96 tonnes of gold.

But the scheme was quietly paused in February 2024. Why? Not because we stopped buying, but because gold prices shot up so high that paying investors back became too expensive. Early buyers walked away with roughly 205% returns! Even today, older SGBs sell at a 12% premium in the open market because people are still heavily interested in them.

Then came Gold ETFs, another way to invest in gold digitally. Total investments in these funds jumped from ₹59,000 crore in March 2025 to over ₹1.71 lakh crore by March 2026. That is a massive 191% jump in twelve months. Financial Year 2026 alone saw ₹68,868 crore pour in, which is more than the previous five years combined.

In fact, for the first time in Indian market history, people invested more money in commodity funds (like gold and silver) than in stock market funds: ₹99,280 crore against ₹77,780 crore.

Talk about timing, though. The newest option is Electronic Gold Receipts (EGRs). The NSE launched this segment on May 4, allowing people to buy digital gold starting at just ₹1,500. This launched exactly six days before the PM's appeal to skip gold.

And it is not just the public buying it. The RBI itself bought 86 tonnes of gold between September 2025 and March 2026, bringing 64 tonnes of it back to India in just six months. Today, our central bank is the second-largest gold buyer in the world.

So, will Indians actually pause buying gold for a year? The numbers answer the question before families even have to.

Every single digital or paper gold alternative has seen record-breaking demand. None of these options reduced India's hunger for gold, and they just gave people more ways to buy it. The appeal is no longer just competing with local jewellery shops. It is competing with the stock exchanges, mutual funds, secure vaults, and more.

But here is the ironic part. The appeal to step away from gold has unintentionally made it the most popular asset in the country right now. It is just a quirk of human psychology - when you ask people to look away from something, they tend to look closer. The appeal was meant to cool things down, but instead, it simply put the spotlight back on the metal, reminding Indian households exactly why they value it so much

We are officially nearing the end of the easy phase of capital markets.

For the last few years, F&O participation has been growing at an unprecedented rate. Retail entered in record numbers, buying the dip became muscle memory, and tracking a daily P&L screen became a regular habit. That approach works right up until a real correction hits. Today, with the Sensex dropping 1,000 points, the limitations are clear.

When volatility strikes, the reflex for many active traders is to trade more. They enter and exit repeatedly trying to offset losses. But reacting with continuous trading exposes a major blind spot: participants focus entirely on market movements while ignoring the fixed cost stack eroding their capital.

The regulator has been publishing the receipts for three years now.

-SEBI's January 2023 study: 89% of individual F&O traders lost money in FY22.

-SEBI's September 2024 updated study (FY22 to FY24): 93% of individual traders lost money. Aggregate losses crossed ₹1.8 lakh crore. The top 3.5% of loss-makers (~4 lakh traders) lost an average of ₹28 lakh per person over the three years. In FY24, 92.1% of new traders lost money averaging ₹46,000 each. 88% of regular traders lost money averaging ₹1.5 lakh each.

-SEBI's July 2025 study (FY25): 9.6 million participants covered. 91% lost money. Net losses crossed ₹1.05 lakh crore in a single year, up 41% YoY. Average per-person loss: ₹1.1 lakh.

Three consecutive studies. Three consecutive years. Loss rates between 89% and 93%. This is not noise. It is the base rate. But, the more uncomfortable details in these studies show where the money went.

In FY24, while individual traders lost ₹74,812 crore, proprietary desks booked roughly ₹33,000 crore in gross profits and FPIs booked another ₹28,000 crore. SEBI's September 2024 study attributed 96% of those proprietary profits and 97% of those FPI profits directly to algorithmic trading. Index options daily premium has grown from ₹4,359 crore in FY20 to ₹64,881 crore in FY25.

The math is plain. Most retail F&O trades have a machine on the other side. Retail puts in the money. Algorithmic desks take it out. Layer on slab-rate tax on net trading profit, STT on every trade, brokerage, exchange fees, and GST. The breakeven hurdle for a retail trader is not small. It is structural.

This correction is the part of the cycle where structural disadvantages surface in account balances. The traders who navigate it intact will be the ones who already understood what the SEBI data has been saying since 2023: In F&O, gross P&L is a paper metric. Net of taxes, costs, and the counterparty on the other side of every trade, the only number that matters is what is left in the capital account at the end of the year.

We built something that fixed broken uploads from three days to ten minutes, a 10x lift in velocity. No engineer wrote the fix. No human shipped it. So who did?

https://t.co/rUIWhhs9gD

Most CFOs believe their tax compliance is under control.

But @ClearTax State of Tax Assurance Report 2026 shows a different picture: many enterprises are still discovering compliance gaps only after a regulator notice arrives.

Our team analyzed 12Cr data points, across 500 enterprises, and responses from 100 CFOs to showcase the gap between the illusion of compliance Vs data-backed reality.

Worth reading for CFOs and finance leaders looking at tax assurance, notice prevention, ITC recovery, and real-time visibility.

Read the report: https://t.co/BdGOW69hds

#TaxCompliance #GST #CFO #EnterpriseFinance #TaxTech #IndiaFinance #ClearTax”

When a broker silently changes their tax statement format, our system used to break, leaving users stuck waiting up to 72 hours for a manual engineering patch.

To eliminate that wait, we stopped looking for faster ways to write patches and built a product that heals itself.

Today, the moment a file fails to parse, the system doesn't notify an engineer, it instead immediately gets to work. An AI agent steps right in and takes over. It reads the document, dissecting the data to pinpoint exactly what layout changed. Instead of just flagging the issue for a human, the AI agent writes the production code to fix it from scratch on its own.

But letting an AI write code for sensitive tax data is risky if left unchecked. So, we built an automated testing process.

Before the AI's fix is allowed to touch the live product, it has to prove it works. The system tests the newly written code against every other user currently facing the exact same error. If the fix fails even once, the AI scraps its own work, rewrites the code, and tries again.

Once it succeeds, it builds its own safety nets to ensure the new code doesn't accidentally break anything else. Finally, a second, completely independent AI agent steps in as a strict quality reviewer to audit the work.

Only after passing this series of checks is the final fix pushed live.

A completely autonomous, self-healing engine. While the AI handles all of this heavy lifting in the background, the user's filing journey seamlessly flows forward. What used to break their momentum is now entirely invisible.

During ITR filing season, a trader's time should be spent purely on strategy: minimizing tax liability, claiming maximum refunds, and building wealth. He shouldn't be breaking his head over a failed capital gains upload or a broken computation.

But delivering that zero-friction experience requires solving a massive engineering bottleneck in the background.

Here is the reality of our tax tech: We support 80+ brokers. Every year, those brokers silently push 300 to 400 format changes to their statements.

We realized that even a single format change meant our standard parser wouldn’t comply. Whenever this happened, our teams would go into overdrive to resolve it within 48 to 72 hours. The moment a support ticket was raised, product managers quickly reviewed the issue, and our engineers stepped up and hustled - investigating, writing, testing, and deploying a custom patch to ensure our users could seamlessly continue filing.

We challenged ourselves to overcome this, because a trader shouldn't have to wait three days just to see his final tax computation. So, we started asking a new question: What if, the exact moment our normal parser fails, an AI instantly steps in to fix the parsing on the go? Making that a reality is how we turned a 72-hour turnaround into a seamless 10-minute fix.

The robot uprising is finally here, but it’s not coming for our jobs. It's coming for our manual work.

NVIDIA’s new Cosmos models help humanoid robots navigate the physical world by teaching them to fix their own mistakes when their surroundings change. At ClearTax, we’ve applied that exact same principle of autonomous adaptation to the tax-filing ecosystem.

Every ITR filing season, brokers change their file formats. In the past, this was a manual crisis - a file would fail, and it would take our engineers 48 to 72 hours to investigate, write a patch, and deploy a fix. In the final weeks of the tax filing deadline, a three-day wait is a dealbreaker.

To solve this, we built an Automated Error Logging & Management System (AELMS). It functions like an AI driven independent robot that encounters a new obstacle and simply calculates a way around it, without the need for human intervention.

The Identification: When a file fails, an AI agent diagnoses the cause immediately.

The Resolution: The AI agent writes the code fix and generates its own unit tests.

The Safety Gate: Before anything goes live, the fix must pass an automated sandbox replay and an independent AI code review.

The Deployment: The system merges the fix and notifies the user that they can now proceed.

By automating the ‘detect-patch-deploy’ loop, we’ve brought the resolution time for our customers down from 3 days to under 10 minutes, and saved 90% of our engineering bandwidth. More importantly, we’ve ensured that a user's tax filing isn't derailed by a technicality they have no control over.

Be it a robot in a warehouse or a parser in a tax engine, the goal is the same: building systems that don't just report errors, but actually fix them.

Indians spent ₹20,000 crore on gold this Akshaya Tritiya. Record headlines. But the real story is buried in the data.

Gold is up 63% from last year. Yet physical volumes actually dropped. The average jeweller moved just 25-50 grams over the entire festival.

So where did the money go?

The physical market recycled itself.40-50% of purchases were paid for by exchanging old gold. No fresh cash. Just existing wealth changing form. India stopped absorbing gold we started circulating it.

The fresh money went digital.₹316 billion into Gold ETFs. In one quarter. Digital gold transactions up 69%.

SGBs, ETFs, PhonePe gold all surging.

The Indian buyer didn't abandon tradition. They upgraded it.Same Akshaya Tritiya sentiment. But the capital is now liquid, market-linked, and actually working.

This is what a maturing financial market looks like in real time.

The next decade of Indian wealth won't be built in vaults.

It'll be built on platforms, APIs, and products that make capital work - not just sit.

The vault era is ending. The platform era is here.

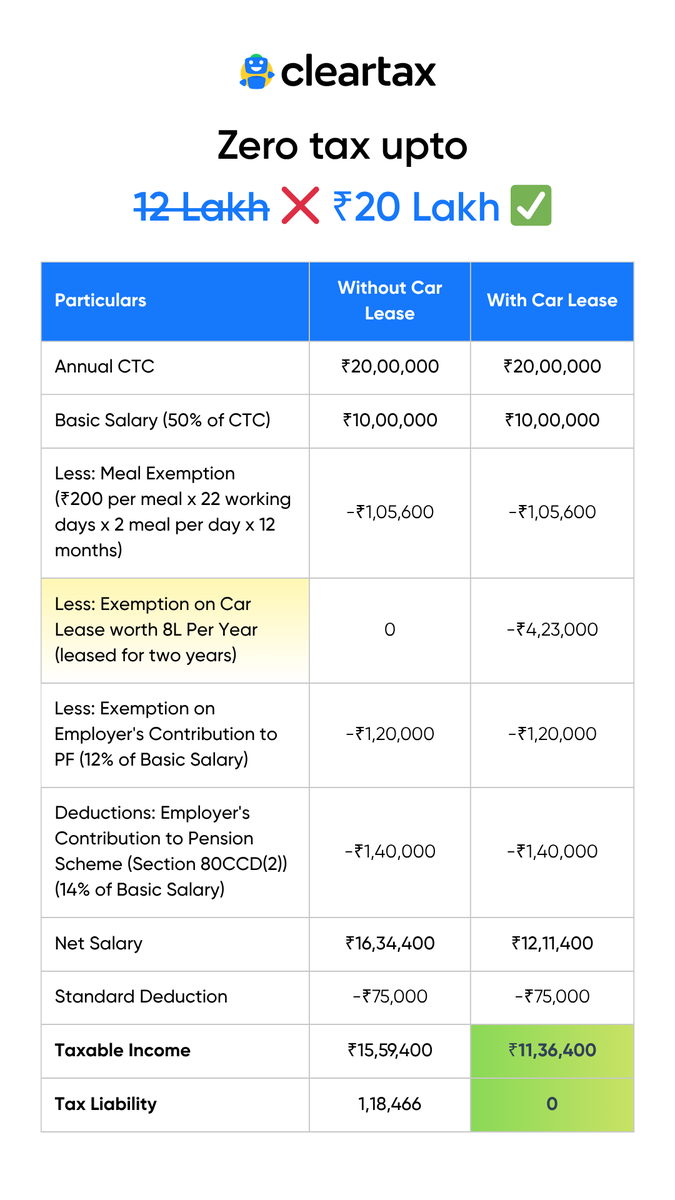

@_karantrivedi_ Actually, the new regime still allows for certain tax-free benefits. While most deductions are gone, items like car leases and meal vouchers are treated as perquisites. These are excluded from your taxable income before the tax slabs even apply.

New Income Tax rules just handed HR a cheat code.

You can give your team a real, meaningful raise roughly 6% more in take-home without touching your salary budget.

The tool? A simple car lease.

It's one of those structuring moves that most companies are sleeping on.

The only downside I can think of is more cars on the road. Silk Board is going to be unbearable.

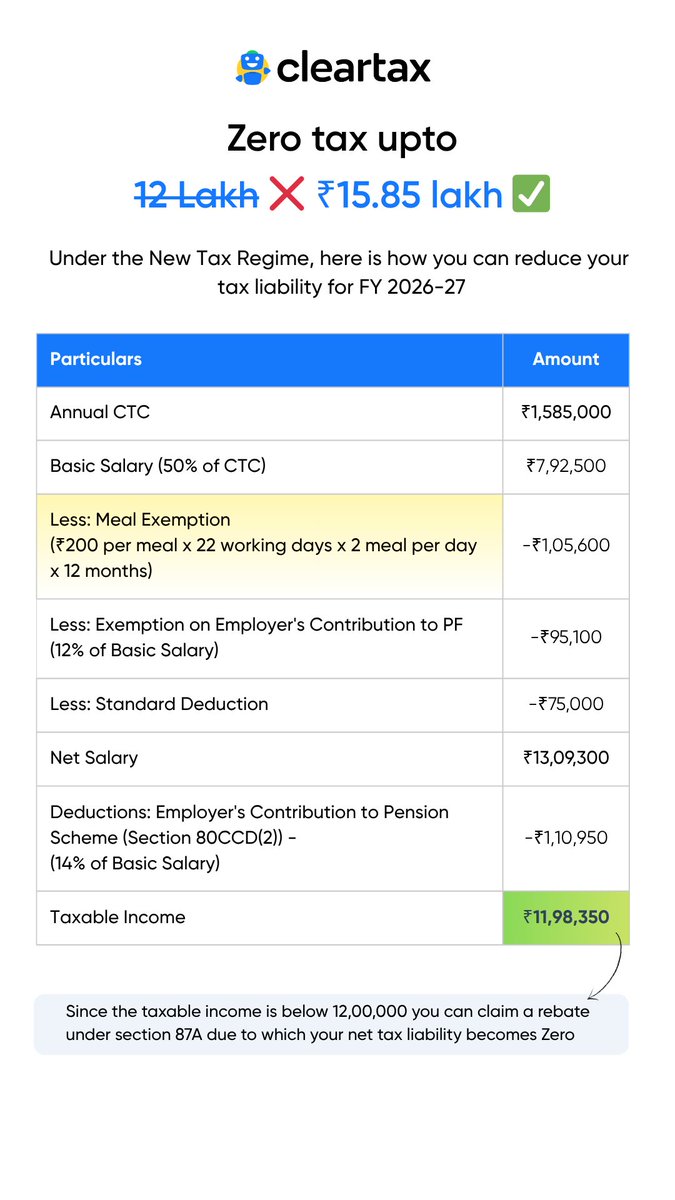

Most people treat their CTC as a fixed number. In 2026, that is a mistake. If you think your zero-tax limit is 12 lakh, you are still living in 2024.

Under the 2026 income tax rules, the effective zero-tax ceiling has quietly moved toward 15.85 lakh. This happens because the system is shifting away from broad deductions and moving toward structured benefits that most people are still ignoring.

At ClearTax, we’ve always believed that complexity is the enemy of the taxpayer. But when complexity creates an opportunity like this, it’s our job to translate it into take-home pay.

Everyone's racing to use Claude Opus 4.6 and GPT-5.4.

We route millions of WhatsApp messages using classification prompts on smaller models.

Here's why:

The routing decision in our tax filing bot isn't a reasoning problem. It's a classification problem.

"How much refund?" → Filing Bot (calculation)

"When will refund come?" → Support Bot (status)

You don't need a $25/MTok model to tell the difference between ‘how much’ and ‘when’

What you need is:

→ Structured signal decomposition (question words, verb tense, entity-action pairs)

→ DB-stored weights that product can tune without code

→ An app layer that does the scoring math

The LLM returns categories. The app looks up scores. The same classification always produces the same route.

This runs on a model that costs 10-15x less than the flagship.

The expensive model is reserved for where it actually matters: the filing conversation itself, complex reasoning, edge cases.

Result: 50%+ cost reduction. Higher accuracy. Fully explainable decisions.

The lesson isn't ‘don't use big models’

It's ‘match the model to the task’

Classification? Small and fast.

Reasoning? Large and capable.

Routing? Deterministic and tuneable.

The teams winning at AI aren't throwing Opus at everything.

They're engineering the right model for each layer of the stack.

#ClearTaxCodeToCraft #AIEngineering

March 2026 marked a turning point in Indian capital markets, not because of the fall but because of who bought the dip. We saw the biggest drop since COVID-19 as foreign investors pulled out nearly ₹1.23 trillion. In the past, this would have caused the market to collapse.

But this time, it became a buying opportunity. This is how the rich are getting richer. While the world panicked, domestic investors saw the 11% drop as a chance to buy, thus adding ₹1.05 trillion into the market. Local investors are no longer just following the trend. They are now the driving force behind it.

I believe this will lead to one of the most detailed tax seasons so far. Last year, ClearTax saw a 45.4% explosion in ITR-3 filings and a 17% surge in ITR-2 filings. As more people move into these segments, keeping your tax reporting accurate becomes the next step in growing your wealth.

As you start making bigger moves in the market, your tax filing needs to keep up. We make sure your taxes are as strong as your growing portfolio.

Indian capital markets have seen a $100 billion exodus of FII, since the July 2024 tax hikes on capital assets. There has been a strong cover up from DII, lately. But, it would require an active tax cut (Capital gains and STT) to keep the momentum of DII up. Historically, in bear markets we have seen the government being responsive to market feedback. I see this happening again, just like when the government updated the old tax limits for children's education and meal allowances to finally match today's higher costs.

While most are busy complaining about global uncertainty, the door has quietly swung wide open for NRIs. The real smart money move isn't just earning in dollars, but realizing that the correction in Indian markets along with a currency gap is the smart way to building long term wealth.