$META está construyendo dos nuevas líneas de negocio.

Llevan meses testando suscripciones de pago en sus aplicaciones. Ahora, las escalan globalmente porque los datos son positivos.

🟣 Instagram Plus: $3.99/mes

🔵 Facebook Plus: $3.99/mes

🟢 WhatsApp Plus: $2.99/mes

Estas suscripciones no quitarán anuncios, ofrecerán funciones prémium, verificación de identidad, mayor visibilidad y soporte prioritario para el usuario.

Y eso no es todo. Zuckerberg acaba de decir en la junta de accionistas que entrar en el negocio del cloud computing "está definitivamente sobre la mesa" si tienen exceso de capacidad en sus centros de datos.

Demasiados mensajes. Misma pregunta.

$ASTS

¿Qué vas a hacer? ¿Vas a vender?

¿Hasta dónde la ves? ¿Y si esto se gira?

Voy a contestar una vez

Sin filtros

No recomiendo nada

No soy asesor

No vendo cursos

No cobro suscripciones

Voy a explicar cómo lo veo YO

Y por qué creo que la próxima fase puede ser una de las más violentas que hayamos visto en @AST_SpaceMobile

Hilazo 👇🧶

$ASTS

Few understand how Disruptive that Ast Spacemobile will be to the World of telecommunications.

Ast Spacemobile will be as, if not more Disruptive than Bell Labs discovery of the Fundamentals of the T Carrier system, that evolved into using laser and glass to transmit data.

(Fiber optics)

I spent a lifetime in this field, and to this day, still wrapping my head around how technically advanced Ast Spacemobile is compared to any potential NTN ubiquitous 5G/ 6G competition. ( BTW, there is no competition.) The 3,800 US Patents and Patents Pending has solidified and moated this technology.

I chuckle when the Street looks at Starlink as our Competition. $2T IPO?( smile)

I can not make anyone that doesn’t have a telecommunications background understand the difference.

The Street has yet to wake that Ast Spacemobile will not have any competition for a very long time.

Soon to be understood.

AT&T, Verizon and T- Mobile have done Due Diligence

$IBRX

Listen to this.

If Fox Business is right and Makary’s resignation was tied to Sen. Ron Johnson pressing for answers on the FDA’s rejection of cancer drugs and immunotherapies, that is a massive storyline.

This is exactly the kind of pressure the FDA needed.

Cancer patients do not have time for arbitrary gatekeeping, politics, or endless delays while promising immunotherapy platforms sit waiting.

Makary is out, Kyle Diamantas is acting FDA commissioner, and the whole oncology approval conversation just got a lot more interesting for $IBRX.

I could verify Makary’s resignation and Diamantas being named acting commissioner from current reporting, but I’d still phrase the Ron Johnson/Fox angle as “if Fox Business is right” unless you have the clip linked.

🚨 Saudi Arabia just approved a breakthrough cancer treatment for lung cancer.

Americans? Still stuck with only one narrow bladder-cancer use.

Dr. Patrick Soon-Shiong on Chris Cuomo:

✅ IL-15 based therapy (ANKTIVA)

✅ Strong survival data in lung, breast, pancreatic & glioblastoma

✅ Same drug, same data — different access

Over 13,000 U.S. patients are now requesting it.

Why are Americans being left behind?

Watch the full clip 👇

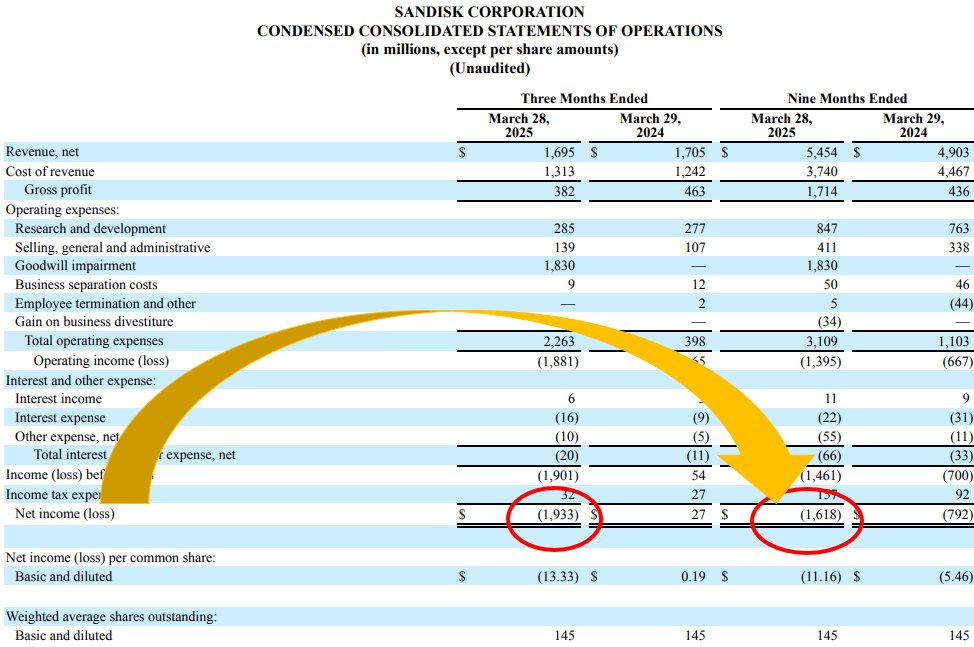

1 year ago, SNDK was under $30, its up 5200% at $1560.

SNDK lost $2 billion every quarter, but GOOG AMZN needs their chips.

Right now, there's 7 companies under $30 exactly like SNDK:

1. $POET — $11.19 🎯 PT: $80

Optical interconnects that replace copper inside AI data centers.

Customers: Lite-On, $SMTC, NTT now targeting Marvell's ecosystem

Catalyst: Malaysia plant ramping 30,000+ Infinity optical engines in 2026

2. $NOK — $12.82 🎯 PT: $15

5G + optical networking backbone for every hyperscaler buildout.

Customers: Amazon, Google, Microsoft €1B in orders from them in Q1 alone

Catalyst: Raised optical network growth outlook to 18–20% on exploding AI demand

3. $EOSE — $8.70 🎯 PT: $30

American-made zinc batteries powering the grid AI data centers drain.

Customers: Utilities, IPPs, CAISO & ERCOT grid operators

Catalyst: $303.5M DOE loan finalized — funds 8 GWh annual production by 2027

4. $DGXX — $6.45 🎯 PT: $30

Building GPU data centers to rent compute directly to AI companies.

Customers: Cerebras Systems (AI chip maker)

Catalyst: $1.1B, 10-year colocation deal signed $2.5B potential with expansion

5. $LWLG — $16.41 PT: $120

Electro-optic polymers that make AI fiber speeds physically possible.

Customers: Tower Semiconductor, GlobalFoundries, 4 Fortune 500 companies in Stage 3

Catalyst: PDK 1.1 ready for high-volume foundry transfer tape-outs begin H2 2026

6. FLNC — $24.50 🎯 PT: $28

Battery storage that keeps AI data centers powered without grid failure.

Customers: Two major hyperscalers (MSAs just signed), utilities globally

Catalyst: Record $5.6B backlog + first hyperscaler order converting Q3 2026

7. $PLAB — $49.50 🎯 PT: $55

Photomasks for every advanced AI chip no mask, no chip, period.

Customers: $TSM, $INTC, Samsung, UMC the entire chip foundry food chain

Catalyst: Record high-end IC revenue driven by AI chip packaging and advanced logic nodes

Remember, these have 1000%–2000% potential like $SNDK. My favorite is POET, but I like PLAB too since it makes photomasks which is needed in every chip on earth.

♻️ RESHARE this post and share 1 comment, and I'll DM you my BUY ZONES for each of these.

$ASTS All ive been seeing is this and heres my thoughts to everyone who can spare a couple minutes…

All my timeline is filled with :

“space is unforgiving’

“Management is false”

“Satellites cant be made”

“We need large scale”

“Amazon will catch up”

“Delays are compounding”

“2026 will be flat”

“Re-rating to $30”

“No service until 2028”

“Market doubts launches”

“Mgt has found serious flaws”

The list goes on and on and on…;

First of all. This is a high risk and high growth stock. You cant expect 100% moves to the upside without 50% moves down.

The amount of MNOs this company has partnered with is absolutely unbelievable and is a MOAT no company will be able to replicate. Why? Because other MNOs want the same advantage as their peers. You dont think these multi-BILLION dollar corporations have done their DD and thoroughly coordinated with mgt to see the true capability of the tech?

Do you honestly believe a company will take the time to file 3800+ patents for no reason?

As ive said before- its taken longer than anyone anticipated for the batches to become ready BUT no space company has actually ever stuck to their guidance (pointing at Space X, BO and RKLB)…

The fact of the matter is that if you believe this company is a dud and they wont get sats shipped then join the shorts … but WHEN these sats start rolling out after 8-10 things will move extremely fast. Can you tell me thats false?

Weve seen how fast narrative can change in an INSTANT with Semis, Memory, Photonics etc…

The same will happen with $ASTS As soon as the market starts seeing the production work as its planned to. In the grand scheme of things weve had 4 months of delays since theyve announced the stacking issue and since tested and maybe found a few other tweaks to polish out.

The company is still growing, hiring and expanding production capabilities…

Thats a sign of an adapting company not a collapsing one.

Thats just my two cents. Take it as you please but to me the theory is valid. Yes you can complain about opportunity cost and missing the post Iran pump blah blah blah…

Thats not how real investing works. You buy companies you wish to hold for the future and in this aspect why would you buy $ASTS for a quick flip when the real value comes when its PRINTING FCF?

Thank you for your time.

Ben Jawanda.

🚀 AST SpaceMobile $ASTS acelera su capacidad industrial en EE.UU.: un movimiento estratégico clave

AST SpaceMobile anunció hoy una expansión masiva de su huella manufacturera en Texas y Florida, llevando su capacidad total a 500.000 ft² y elevando su plantilla estadounidense a más de 1.800 profesionales, más del doble que hace seis meses.

Este paso consolida a la compañía como uno de los actores industriales más integrados del sector espacial en EE.UU. y refuerza su posición como líder absoluto en conectividad celular directa desde el espacio.

🔧 Escalando producción a nivel “hyperscaler espacial”

-Nuevos sitios en Texas y Homestead (Florida) incrementan capacidad de producción y ensamblaje.

-ASTS alcanza 95% de integración vertical, desde materiales hasta satélites finalizados.

-El corazón de la expansión: fabricar más BlueBirds, más rápido, con mayor control y menores riesgos de cadena de suministro.

🛰️ BlueBird de nueva generación: salto tecnológico

Las nuevas instalaciones permitirán acelerar la producción del satélite BlueBird Block 2, equipado con:

Antena phased-array de 2.400 ft² (la mayor jamás construida en LEO).

ASIC AST5000, diseñado para multiplicar por 10 la capacidad de procesamiento.

Velocidades pico de hasta 120 Mbps por celda, habilitando voz, datos y video directamente a smartphones 4G/5G estándar.

Este nivel de tecnología —junto con más de 3.800 patentes— sitúa a ASTS varios años por delante de cualquier competidor en el segmento direct-to-device.

🇺🇸 Seguridad, soberanía tecnológica y escala industrial

El mensaje de fondo es claro:

AST SpaceMobile se posiciona como infraestructura crítica fabricada en EE.UU., alineada con prioridades gubernamentales en conectividad, defensa y autonomía tecnológica. Con socios como AT&T, Verizon, Google y American Tower, la empresa está construyendo la única red satelital global totalmente compatible con redes móviles existentes.

📈 Lectura estratégica

La expansión de capacidad y talento fortalece la tesis de inversión:

Mayor velocidad de despliegue de la constelación.

Reducción futura de costes unitarios.

Ventaja competitiva difícilmente replicable.

Posicionamiento favorable frente a clientes MNO y Gobierno.

ASTS no solo construye satélites. Está construyendo una industria completa.

@MyInvestorES Imposible realizar movimientos, cuando el mercado esta asi colapsais. Lo siento pero sois un auténtico desastre. No son cosas puntuales. En cuanto pueda me piro de aquí