Indian equities, fixed income, and the macro in between. Earnings deep-dives, market frameworks, bond market coverage. CA (ICAEW) | London Business School

Going to use this account to share how I think about Indian capital markets — equities, fixed income, and the macro that connects them. A thread on what to expect.

Ujjivan SFB:

Stock doing well in line with the update. Already up 10 percent since the start of the month.

Results and guidance will be key and will help see how the bank is growing and plans to grow in the coming time.

Markets doing well post the scare on Wednesday.

TCS result was in line with expectations, nothing spectacular, nothing too worrisome. Has resulted in some buying in IT stocks.

More results as we get into next week.

Extremely volatile day with Trump's comments.

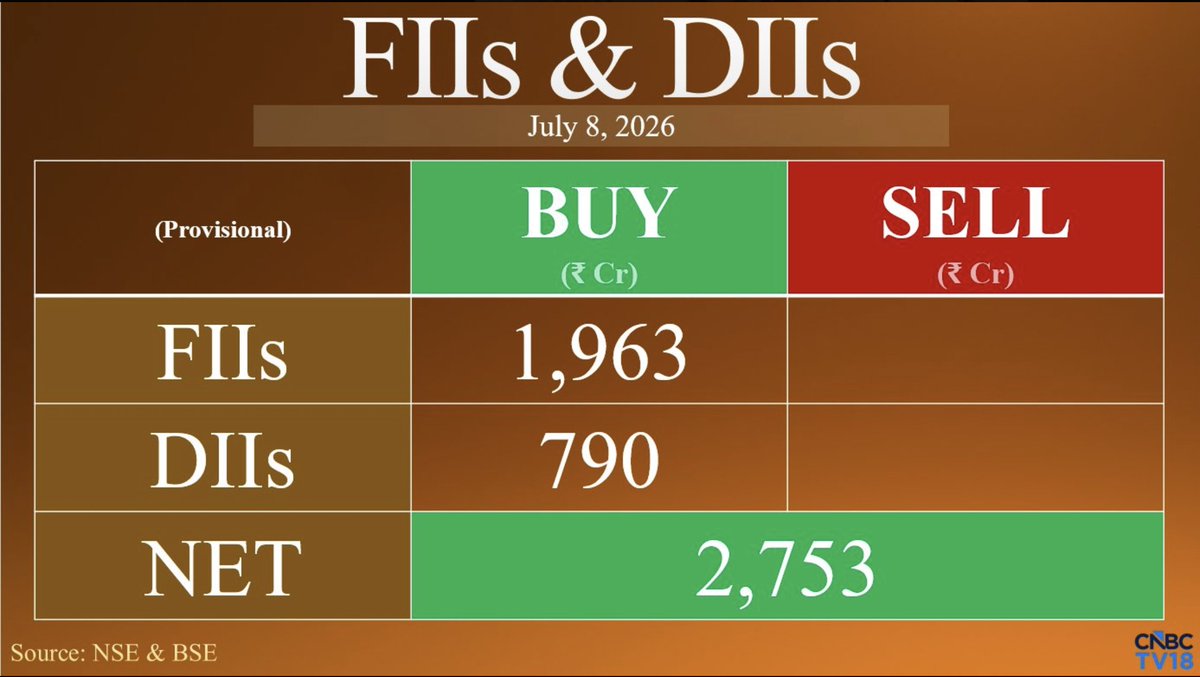

FIIs and DIIs both net buyers in the panic stricken day, lets see how the global situation develops from this

Markets trading in the green today, bouncing back from the huge sell off yesterday after Trumps statements caused panic as they hinted the Middle East conflict might not be over as it was believed.

Any further statements from Iran/US might cause short term knee jerk reactions in the market.

Extremely volatile day with Trump's comments.

FIIs and DIIs both net buyers in the panic stricken day, lets see how the global situation develops from this

Another day of FIIs buying. Quantum isn’t big but there are a few signs the selling is cooling down, let’s see how it progresses over the coming days and weeks

Markets trading marginally in the red. Not a big surprise after a long rally, also impact of global market being down. Nasdaq corrected 1.16%, S&P down 0.45% yesterday.

Nearing the start of results, which will be factor in determining where the market is headed in the short term

Another day of FIIs buying. Quantum isn’t big but there are a few signs the selling is cooling down, let’s see how it progresses over the coming days and weeks

The tax changes for FPIs are already showing up in the data.

Foreign investors poured a massive ₹41,773 crore into the Indian bond market in June alone - more than 4x the cumulative net inflows of around ₹9,405 crore seen from January to May 2026.

This is an early but encouraging sign that removing tax frictions is making Indian G-Secs far more attractive to global investors. Add in the expansion of the Fully Accessible Route (FAR) and improving prospects of inclusion in the Bloomberg Global Aggregate Bond Index, and the structural case for Indian debt continues to strengthen.

If sustained, higher foreign participation could deepen liquidity, improve price discovery and, over time, help lower the government’s cost of borrowing.

The reforms seem to be working.

Yesterday the Government issued an ordinance exempting foreign investors from all tax on G-Sec investments - both interest income (previously 20% withholding) and capital gains (previously 12.5-30%) - effective April 1, 2026.

The timing is deliberate. FPIs have pulled out ₹2,63,784 cr from India in 2026 - one of the worst FPI outflow years in recent memory.  Rupee at record lows. Bond yields ~7%. The government needed to do something to make Indian sovereign debt more attractive to global capital.

Post-tax returns for foreign investors on Indian G-Secs improve by 15-20% with this change - meaningfully narrowing the gap with other sovereign bond markets they compare us against.

Why this matters beyond the tax saving:

→ India is now part of major global bond indices - JPMorgan EM Index, Bloomberg EM Index. Tax friction was the key remaining hurdle for passive index flows to fully materialise

→ Pension funds, sovereign wealth funds, insurance companies - the long-term stable capital - require clean post-tax return comparisons before allocating. This removes that barrier

→ FPIs currently hold only ~3.34% of outstanding G-Secs — ₹3.75 lakh cr out of a total ₹112 lakh cr stock.  The headroom for participation to increase is enormous

→ More FPI demand for G-Secs = better price discovery = potentially lower government borrowing costs over time

One policy change won’t trigger a flood of flows overnight. Global risk appetite, crude prices and the geopolitical backdrop still matter more in the near term.

But this removes a structural friction that was holding back India’s integration with global fixed income markets. A well-timed and well-designed move. ☕

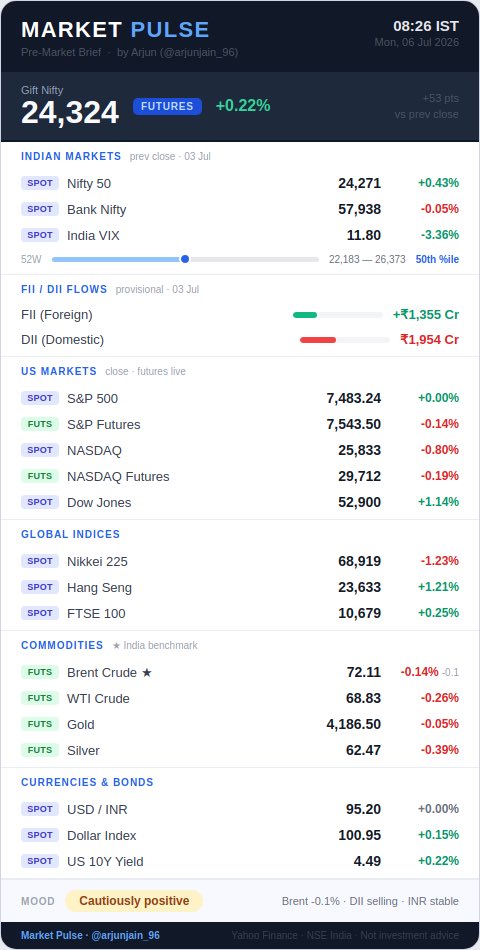

A positive start to the week expected for the markets as indicated by the Gift Nifty. A continuation of the past couple of weeks.

IT results will start the Q1 27 results this week, and will be keenly looked out for commentary on how the near term future for growth looks like

#1QWithCNBCTV18 | HDFC Bank Q1 Update

🔴Gross Advances Up 15.4% YoY At Rs 30.61 Lk Cr

🔴Deposits (Period End) Up 14.7% YoY At Rs 31.70 Lk Cr

🔴CASA Deposits Up 9.4% At Rs 10.25 Lk Cr

🔴Advances Under Management Up 12.4% YoY At Rs 31.27 Lk Cr

IDBI Bank Q1FY27 business update looks healthy

Total business: ₹5.84 lakh cr, +15% YoY

Deposits: ₹3.25 lakh cr, +10% YoY

CASA: ₹1.42 lakh cr, +7% YoY

Net Advances: ₹2.59 lakh cr, +22% YoY

The key positive is the strong growth in advances, clearly ahead of deposit growth.

The bank has come a long way from where it was a few years ago. Now the next leg will depend on sustaining growth, keeping asset quality under control and improving profitability.

Privatisation remains the big optional trigger. If and when that progresses, IDBI could potentially enter a very different phase of growth.

Worth tracking. Not advice. DYOR.

IDBI update :

Moneycontrol article says Fairfax could bid $5 bn for IDBI Bank, and is said to offer to fully divest from CSB Bank

Additionally there is expectation that two of Faifax's large non-lending businesses:

- GoDigit General Insurance

- IIFL Capital Services

will likely be folded into IDBI Bank as its subsidiaries.

JM Financial's PAT jumped 46% YoY to ₹1,202 cr in FY26.

Yet it trades at just ~10x P/E and ~1.1x book.

Here's the thing - most people still think of JM as "that investment banking company."

It's actually 5 businesses stitched into one platform. 🧵