@itsthatgigi It was never about "upholding democratic principles" for the US. If you haven't realised what US imperial regime change is about and what consequences it historically has had on a region, you need to open a history book.

The $TRIA Community Sale is now live via @NozomiNetwork on @legiondotcc.

On Friday, we took a snapshot of the top 25 cSnappers and top 25 Snappers in @useTria's ACM campaign.

Made the cut? You’ve now got a guaranteed allocation to invest in $TRIA:

→ up to $1K each for cSnapper

→ up to $500 each for Snapper

$AVICI: @avici

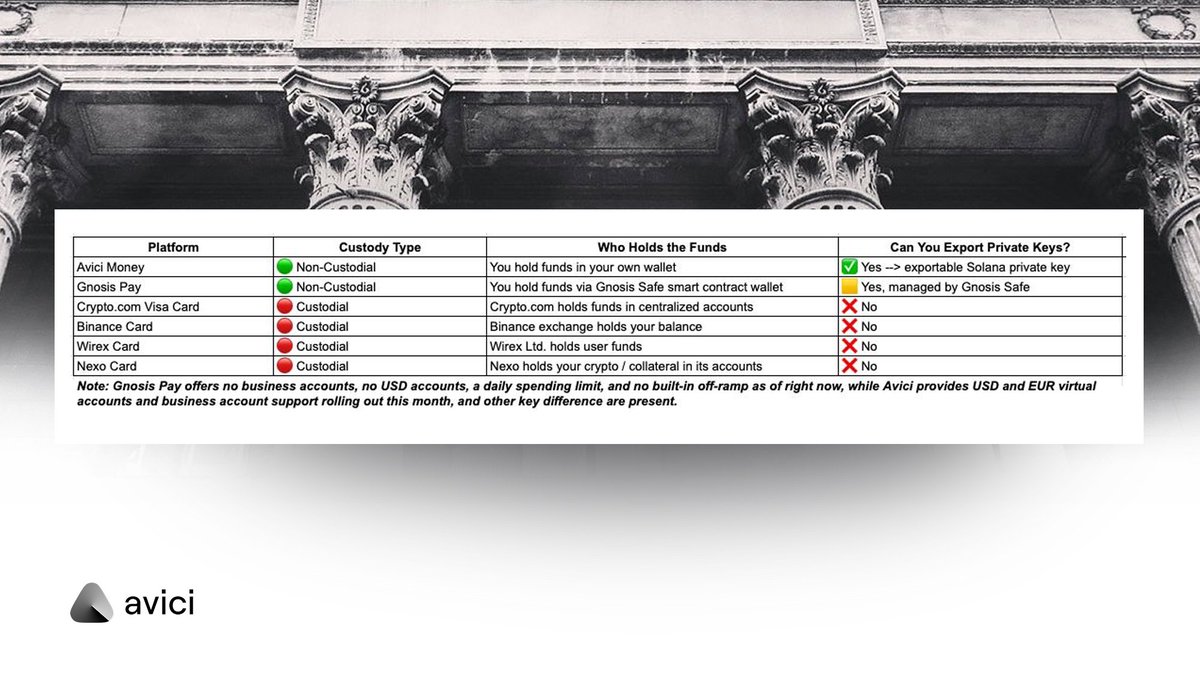

> Non-custodial you hold your own keys, not the project. NOBODY can touch or freeze your funds (unlike many other competitors)

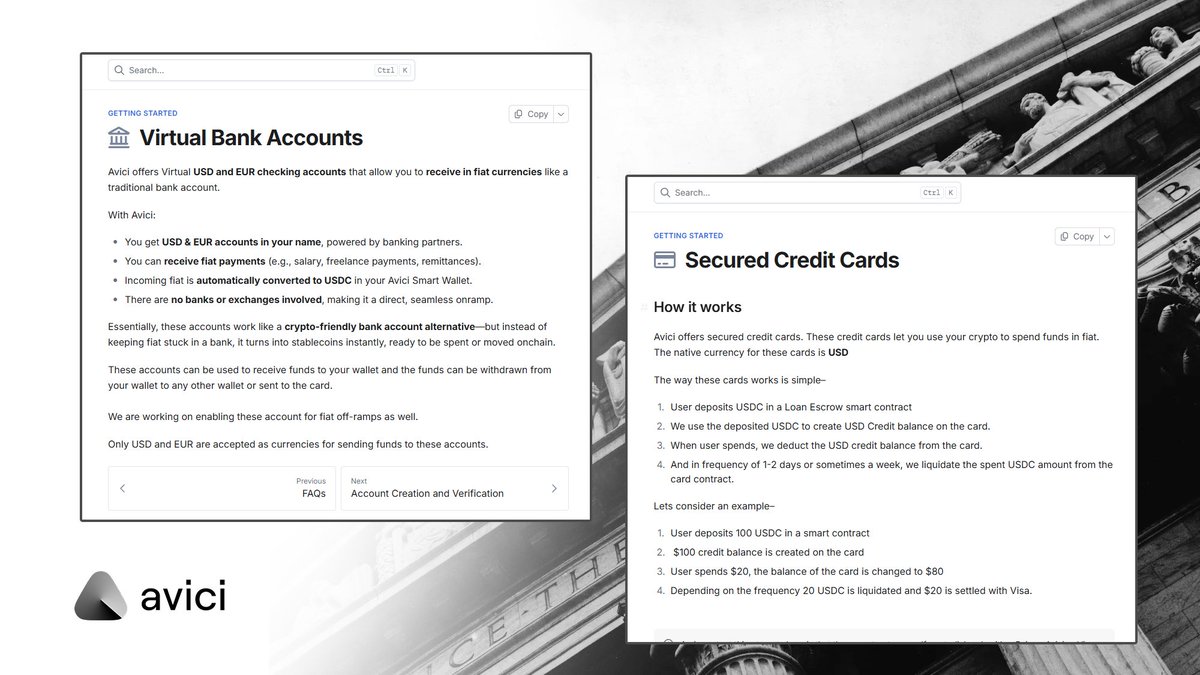

> You’ll have an IBAN account, simply put, users can receive (and send) salaries in fiat (same for businesses with their income) directly, which will be auto-converted to USDC.

> It offers a VISA Card with no top-up fees, no FX markups, no transaction fees, no payment limits, if you want to spend millions in a day, you can.

> Avici BIZ will be launching soon —> business accounts for startups, DAOs, institutions etc.

> DAO-owned: 0 VC or team allocation, a treasury spending cap (unless the DAO decides otherwise), and 100% circulating supply.

> Revenue model is sustainable: Visa interchange fees + FX spread + Premium tiers, and future lending yield (already live & generating revenue).

> 3.5M was raised out of 34.2m committed, many people got refunded, shows that the team is here to last.

> App is already live on iOS & Android, already showing good functionality even in beta.

> Even the CEO of @KASTcard, a competitor is interested in buying $Avici & helping the Avici team.

Just a fraction of what Avici is building is summed up here. With all the functions they’re planning to add, there simply won’t be much need for individuals to use traditional banks, something the crypto space has waited for, for a long time.

What Avici achieved in their beta so far:

- Total spend with Visa card: $1M+,

- Avg growth of spends: 35% average MoM

- Retention for active users*: 70% MoM (people are satisfied with their product)

- Total onramp volume (USD,EUR): $800k+

- Cards created: 5k+

- Total signups: 9K+

Avici is already generating revenue in its beta. 90% (if not more) of projects never reach this stage, and for $AVICI, it seems like the standard rather than the goal.

Avici consists of two main products:

1. The credit cards, which let you spend your crypto directly and this card can even be added to Apple Pay, Google Pay, etc.

2. The virtual banks, bank accounts with an IBAN, that allow you to on-ramp fiat to crypto via simple transactions, such as receiving your salary. The fiat is auto-converted to USDC and sent to your Avici wallet.

You can basically see it as a crypto bank that gives you a Visa card (physical + virtual), lets you receive and send money like a normal bank account (thanks to your own IBAN), and lets you hold, swap, and spend crypto directly from your wallet. And because you’ve got a Visa card, you can spend crypto worldwide.

One of the biggest pros here is the safety aspect. Most cards e.g., https://t.co/syA5WAcNul, Wirex, Binance, etc. are custodial, meaning they hold your money. If the company goes bankrupt or freezes your account (like FTX), you simply lose access to your funds, and they could very well be gone. Avici is non-custodial, meaning you own your wallet and private keys. They (and nobody else) can freeze your money or touch your funds in any way.

Fee-wise, it’s also beating competitors + there are no payment limits, you can spend millions if you want.

I’ve seen some questions regarding the card purchase fees, which is between $10 and $30 (and $20 annually for the signature tier) for the virtual cards. However I think every user will prefer a fixed fee in dollars that doesn't increase when you spend more over a high recurring percentage fee that ''eats'' into every transaction and basically scales with your spending because it's a percentage, not a fixed amount of $. If you need a discount or setup help, DM @AviciHelp. They got support on X and TG.

Avici can basically be seen as the crypto bank everyone hoped for > one that’s able to deliver on the promises the crypto space has made to us: real usage of crypto, worldwide, as a means of payment, without any centralized institutions able to touch your funds.

I bought from here. Jup has the best liquidity. https://t.co/9sgxeWFO9A

Projects buying featured spots on WOM on a "slow Sunday."

Team working around the clock on a "slow Sunday."

First major campaign locked on a "slow Sunday."

At this point, nothing about WOM is slow.

A woman is killed by a man every 3 days in the UK...

78% are murdered by a partner/ex

Yet not once have I heard Reform talk about this

Not once have I heard them back measures to protect women’s safety

In fact, they voted against them

So ask yourself...

Why the concern for women only when the perpetrator is a migrant?

@RupertLowe10 Build more social housing, storm the palaces, expropriate your lords.

Bris getting upset at centuries of colonialism coming home to roost is comedy gold 😂

@MigrationWatch@juice8882 Build more social housing, storm the palaces, expropriate your lords.

Bris getting upset at centuries of colonialism coming home to roost is comedy gold 😂

Last Friday delivered one of the worst altcoin wipeouts in crypto history, and the post-mortem of it has been a whisper.

When LUNA blew up, it owned the news. When FTX collapsed, it ruled the cycle. When we had our COVID crash, Crypto Twitter couldn’t stop talking about how we almost went to zero and what saved us.

But this time, a week later, there’s near silence. Instead, we’re told it was just a tweet. That’s not serious analysis. Yes, late Friday, Trump dropped a trade-war headline after U.S. markets closed: 100% tariffs on China and new export controls. That was the spark.

But a single tweet doesn’t send alts down 70% in minutes or vaporize entire portfolios within an hour.

The violence came from structure, from a breakdown deep in crypto’s plumbing.

During the flush, Ethena’s synthetic dollar, USDe (ticker USDe), printed as low as $0.65 on Binance while holding near $1 on other venues. This wasn’t a global depeg. It appears to have been a Binance-local pricing failure, an oracle and order-book divergence that instantly slashed collateral values for users on Binance’s unified margin system.

When your collateral is repriced that far down on a single venue, everything built on it collapses.

On Binance’s unified / cross-margin system, traders can post multiple assets, including USDe and wrapped tokens, as collateral across all their open positions.

When Binance’s feed suddenly marks USDe at $0.65 instead of $1.00, the user’s collateral value shrinks, maintenance ratios blow up, and the liquidation engine begins selling their other assets, often high-beta alts, into an already collapsing market.

Those forced sells push prices lower, triggering more liquidations across the exchange and, through arbitrage, across the entire crypto market.

Example:

Imagine a trader with $200,000 total equity.

$50,000 in USDe collateral

$150,000 in long altcoin positions

Binance marks USDe at $0.65, so that $50,000 becomes $32,500; In this case, $17,500 in margin cushion vanishes instantly.

The system detects the shortfall and auto-liquidates part of the alt positions to rebalance. Those sells slam into thin order books, driving alt prices down another 20–30% almost instantly.

Now the trader’s remaining alts, which weren’t yet liquidated, are worth even less, cutting collateral ratios further and triggering the next round of liquidations.

Each liquidation dump pushes prices down for everyone else using the same assets as collateral, igniting a chain reaction. By the time the loop finishes, hundreds of millions in positions are forcibly sold, and the cascade becomes self-fueling, a liquidation spiral that consumes everything in its path.

What started as a local pricing glitch becomes a global liquidity collapse.

Arthur Hayes @CryptoHayes summed it up perfectly: “USDe didn’t depeg. Binance did.”

The Ethena protocol remained solvent and over-collateralized. The problem was the venue’s internal feeds and book structure under stress.

When an exchange values collateral based on its own shallow order book instead of a broad market reference, small cracks become sinkholes.

This doesn’t absolve Ethena, any asset printing 35% below peg, even locally, shows fragility. But this wasn’t another LUNA.

It was a mechanical failure, a venue-specific collateral mispricing colliding with excessive leverage and opaque cross-margin rules. The result was one of the largest liquidation waves in crypto history, nearly $19 billion in forced unwinds within 24 hours.

That doesn’t happen from headlines. It occurs when margin engines and oracles fail under stress.

Binance has since promised to compensate affected users and rework how wrapped and synthetic assets are priced. That alone is an admission something broke. And yet, this event has been largely swept under the rug thus far.

We’ve seen bigger macro shocks before: Liberation Day, COVID, and even FTX contagion, yet none triggered alts to implode 70–99% in an hour.

This wasn’t fear. It was faulty design.

One venue’s pricing feed dislocated, collateral collapsed, and liquidation engines spread that contagion everywhere. The industry’s core issue is now undeniable: Too many opaque, venue-specific risk systems govern leverage, collateral, and liquidation.

When one breaks, the entire system pays for it. Design flaws, not tweets, keep blowing up the market.

If this reconstruction is wrong, then @binance and @cz_binance should publish the data:

Which feeds broke and when?

Which collateral assets were hair-cut, and how many users were liquidated? How is the compensation being calculated?

And @ethena should release a venue-by-venue chart showing USDe pricing, redemptions, and hedging during the event, to prove solvency and pinpoint where the break occurred.

Roughly $19 billion didn’t vanish into thin air. People were liquidated, portfolios erased, and careers ended because the pipes broke. If this wasn’t the cause, prove it. If it was, fix it.

Because headlines aren’t destroying crypto, it’s being destroyed by its own infrastructure.

This can’t be another story buried under “macro fear.” The silence is the loudest signal of all.

Systems failed. Users paid the price. And the industry owes them an explanation.

If we don’t fix the plumbing now, the following “tweet” could light the same fuse, and eventually, there might not be much left to save.

Because if a tweet can burn $19 billion, it’s not the tweet that’s the problem; it’s the system.