@AssetoFinance is engineering a compliant platform that integrates traditional finance assets with DeFi, enhancing security, yield, and liquidity for investors.

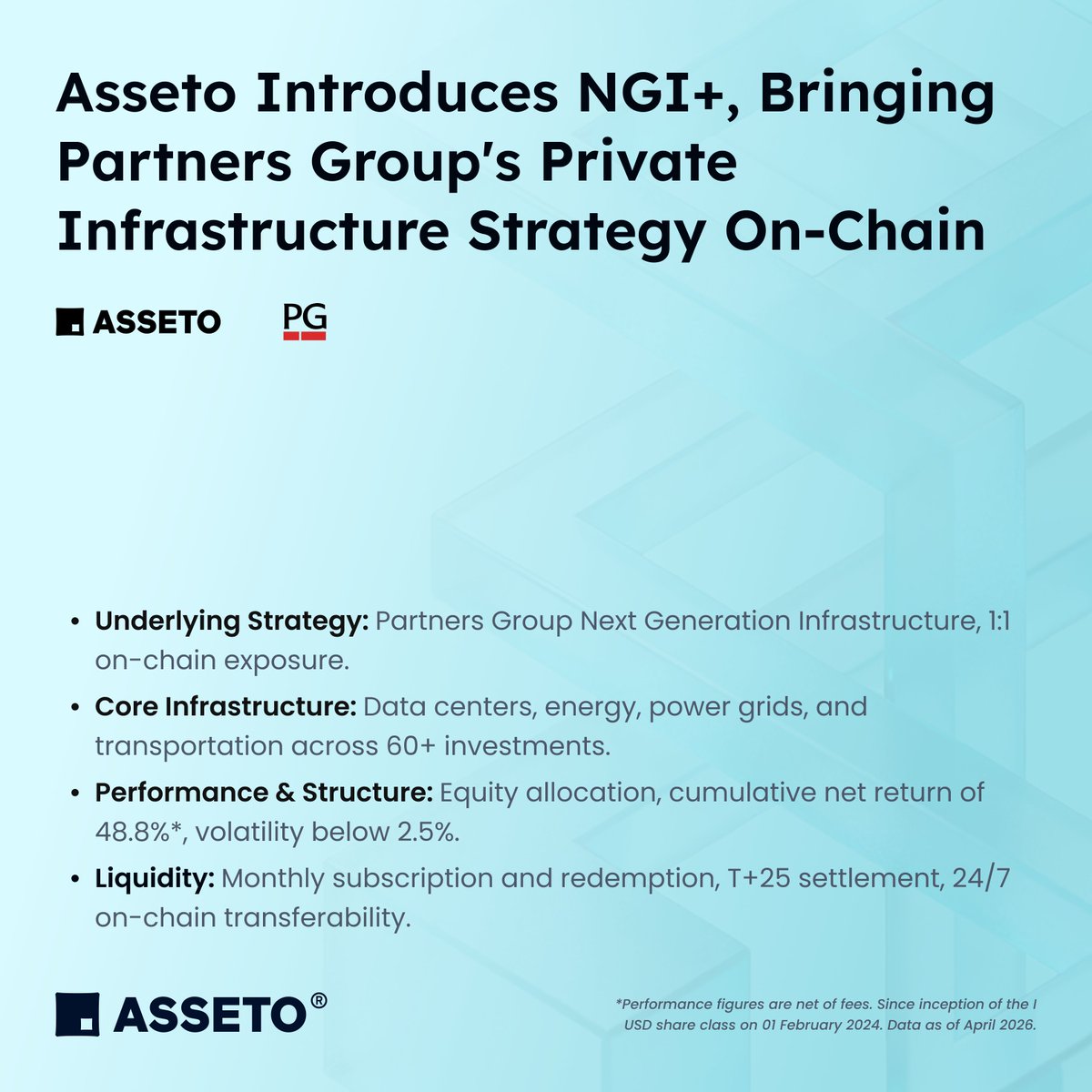

NGI+ is now live, bringing the Partners Group Evergreen SICAV - Next Generation Infrastructure strategy on-chain, with Asseto providing the tokenization infrastructure.

Private infrastructure is one of the most valued allocation asset classes among institutional investors, yet it has historically been difficult to access. NGI+ was designed to bridge that gap, giving eligible investors on-chain economic exposure linked to the net asset value performance of an established global private infrastructure strategy managed by Partners Group.

Asseto built the full on-chain lifecycle infrastructure for NGI+, from aligning legal structures with smart contract logic, to connecting on-chain flows with the underlying fund's operational cadence, to delivering continuous proof of reserves and independent audits. This is the most structurally complex asset we have brought on-chain to date, extending our coverage from money markets, fixed income, and supply chain finance into private infrastructure equity.

Read more in our latest article➡️https://t.co/z6luDuoTHq

At WebX 2026 in Tokyo, Asseto CEO & Co-Founder Bridget Li joined the On-Chain Finance Forum Tokyo 2026, hosted by @HSKChain, on the panel "Bridging RWA and On-Chain Liquidity: A New Paradigm for Institutional Finance."

Bridget noted that the value of tokenization depends on whether tokens can move through compliant, liquid on-chain markets, and that closing the distance between an asset going on-chain and becoming usable liquidity takes full-stack infrastructure spanning custody, compliance, pricing, and settlement. That is the work Asseto does as a full-stack asset tokenization infrastructure and service provider.

NGI+, recently launched, is one example. Tracking Partners Group's Next Generation Infrastructure strategy, it brings private infrastructure assets on-chain and opens an access route for institutional participants.

Most people assume institutions pick a blockchain on performance. They pick it on risk weighting.

Under Basel Committee (BCBS) rules, assets held on permissionless chains, which lack transaction-level privacy and any accountable compliance entity, can carry a risk weight as high as 1,250%. For a licensed bank, that is not a technical footnote. It is a balance-sheet cost heavy enough to make the asset uneconomic to hold.

This is the real reason public permissioned infrastructure is winning institutional RWA flows, and why compliance is not a constraint layered on top of tokenization. It is the thing that determines whether a regulated institution can hold the asset at all.

The chain question was never really about speed.

5/ 💡 The Asseto View: As yield-bearing Treasuries and blue-chip stocks begin serving as margin for on-chain derivatives, the center of gravity in tokenization is shifting from whether an asset's rights can be confirmed toward whether it can be safely used. The two are not in tension. An asset becomes reliable collateral only when its underlying claim is clear, enforceable, and paired with a compliant path in and out. Collateral without legal certainty is worthless under stress.

Asseto builds the technology and operational infrastructure for exactly that, connecting institutional-grade assets to compliant on-chain distribution within Hong Kong's regulatory perimeter, so issuers and partners can bring assets on-chain, and put them to use, without giving up legal certainty.

Follow us for next week's Asseto RWA Watch brief, and continue tracking the critical evolution of the RWA sector.

The most substantive shift in RWA this week was yield-bearing assets moving from static holdings toward programmable collateral. Several new launches let holders post tokenized Treasuries and tokenized stocks as margin for on-chain leveraged positions without giving up the underlying yield. The backdrop is the tokenized-equity momentum carried over from last month's SpaceX IPO, but the new variable is RWAs becoming the collateral base for on-chain derivatives. Asseto tracks this evolution from confirmation of rights toward usability.

Dive into the critical movements this week. 👇

4/ Market Data: Distributed on-chain RWA value (excluding stablecoins) climbed to roughly $33.5 billion as of July 8, up from about $30.6 billion a week earlier, with the holder base near 961,000. The fastest-moving category is tokenized equities, where monthly transfer volume rose about 105% to $8.4 billion and distributed value is up more than 470% year on year, though it remains a small slice of the total in dollar terms. The carryover from SpaceX's June listing kept 24/7 on-chain stock trading elevated, making equities the most actively traded RWA class rather than the largest. Tokenized U.S. Treasuries remain the anchor at more than half of non-stablecoin value.

DL Holdings (https://t.co/F2PHhSpjmj) welcomes @AssetoFinance NGI+! Backed by PartnersGroup private infrastructure funds ($185B+ AUM), it brings data centers & energy infrastructure on-chain.

Eligible investors can learn about NGI+ via DL & explore on-chain access.

#RWA

DTCC is preparing to bring tokenized equities, ETFs and U.S. Treasuries onto the Stellar public network.

The detail most coverage will skip is the control layer. Whitelisted wallets pass sanctions and AML screening before activation, and DTCC retains override keys at the smart-contract level, able to burn, reclaim or redirect tokens if a court freeze or theft occurs.

This is what institutional-grade assets look like on a public chain: open distribution, central accountability preserved. The infrastructure question is no longer whether, but under whose controls.

Asseto is glad to join The GCC <> APAC Venture Corridor in Hong Kong on 9 July, alongside @brincvc, @Ripple, @AWSCloud, @Cyberport_hk, @ambergroup_io, and @osldotcom.

Our Co-Founder JJ joins the panel on tokenization, stablecoins, and the cross-border opportunities connecting APAC and the GCC.

Attendance is curated. Apply to attend below.

https://t.co/cvf0GWIRrr

The biggest fintech opportunities aren't happening inside markets anymore.

They're happening between them.

As capital, regulation, and digital infrastructure evolve across APAC and the GCC, founders who know how to bridge ecosystems, not just enter them, will be the ones who pull ahead.

That's the conversation we're bringing to Hong Kong on 9 July.

Join leaders from Brinc, @Ripple, @AWSCloud@Cyberport_hk, @ambergroup_io, @Assetofinance, and @osldotcom together with founders, investors, and ecosystem partners shaping the next chapter of financial innovation.

Attendance is curated to keep the conversations meaningful.

Apply to attend: ( https://t.co/kYotKWxcFR )

Tokenization is quietly rewriting how regulators classify a security.

Once transfer rights, voting governance and yield can each be programmed as separate on-chain attributes, a single asset can trigger securities, swap and derivatives treatment at the same time, depending on who holds which right. The SEC and CFTC have opened public comment on exactly this, what the industry is calling the modular product problem.

The next phase of RWA is not a token standard debate. It is a question of which legal wrapper survives contact with programmable ownership.

A US$300M tranche of Chinese new-energy mobility infrastructure, EV charging and transit assets, is being structured for offshore tokenized issuance.

The significance is not the single deal. It is the channel. The cross-border RWA pathway opened by China’s February 2026 multi-agency framework is now carrying real, cash-generative infrastructure assets to global capital. An asset class that was effectively closed to foreign direct participation is becoming reachable through regulated on-chain issuance.

Watch this corridor.

5/ 💡 The Asseto View: When central banks begin accepting tokenized instruments as collateral and sovereign debt settles atomically on-chain, the tokenization question shifts from “whether” to “on whose rails.” The value of a tokenized market now depends less on the token standard and more on whether on-chain records stay legally enforceable and operationally sound across jurisdictions. That is a compliance and infrastructure problem before it is a technology one. Asseto builds the technology and operational infrastructure that links institutional-grade assets to compliant on-chain distribution, supporting issuers and partners as this settlement layer matures.

Follow us for next week’s Asseto RWA Watch brief, and continue tracking the critical evolution of the RWA sector.

4/ Market Data: Distributed on-chain RWA value (excluding stablecoins) stands at $30.62 billion as of July 3, down 3.5% over the trailing 30 days as headline value consolidates. The participation picture runs the other way: total asset holders reached 954,348, up 11.6% over the same period, while represented asset value climbed to $428.79 billion, up 18.5%. Tokenized U.S. Treasuries remain the anchor category at more than half of non-stablecoin value. The divergence is the signal. Value is cooling slightly while the holder base broadens, consistent with institutions treating on-chain yield as a standard portfolio allocation rather than a tactical trade.

3/Settlement and Collateral Rails Go Live: The European Investment Bank issued the first DLT-native commercial paper, a €77.5M 10-day note, on Clearstream’s D7 platform with Citi as dealer. The milestone is what happened next: DekaBank and Eurex Clearing pledged the tokenized paper as eligible central bank collateral to the Bundesbank through the Eurosystem Collateral Management System (ECMS), the first time a tokenized short-term instrument has closed the full central bank refinancing loop.

In parallel, Tradeweb facilitated the first on-chain U.S. Treasuries transaction on the Canton Network. Franklin Templeton transferred tokenized Treasuries to Virtu Financial against tokenized cash (USDCx) in a single atomic delivery-versus-payment settlement, removing settlement lag and counterparty risk and pointing to 24/7 liquidity for sovereign debt.

2/Regulatory Clarity Sharpens on Both Sides: Hong Kong’s FSTB and HKMA completed the first phase of their review of DLT in the fixed income market, confirming that current law already supports the day-to-day issuance of tokenized bonds. The Companies Registry clarified that a DLT-based register of debenture holders satisfies the Companies Ordinance, provided the register is complete, exportable to hard copy, and secured against tampering. A second phase targeting fully paperless issuance and clearer rules on on-chain ownership and transfer is set for H2 2026.

In the U.S., the SEC and CFTC jointly requested public comment on harmonizing their portfolio margining frameworks, aiming to let offsetting securities and derivatives positions net across accounts. Freeing this trapped collateral would remove a structural drag on capital efficiency for on-chain regulated assets.

The RWA sector is entering its “settlement rails” phase this week. From Europe’s first DLT-native commercial paper being accepted as central bank collateral, to the first on-chain U.S. Treasuries trade settling atomically against tokenized cash, tokenized assets are moving out of the pilot sandbox and into the core clearing and collateral plumbing of global finance. Asseto tracks this shift as the industry crosses from proof of concept to production-grade market infrastructure.

Dive into the critical movements this week. 👇

The hardest part of tokenization is everything that happens before the token exists. Asset selection, legal structuring, compliance across jurisdictions, custodial design. By the time a product goes live onchain, the work that matters most is already done. That is where Asseto operates, and where we spend most of our time.

Trust remains the highest barrier for institutional capital entering the onchain world, and that kind of trust can only be built incrementally through verifiable structures and transparent operations.

Regular independent audits, fully backed 1:1 asset reserves, onchain-verifiable NAV anchoring: none of these mechanisms are new on their own, but executing and maintaining all of them consistently across every single product requires systematic operational capability and a long-term commitment to detail.

Asseto has made these a product standard, not a marketing talking point.