If we gave you 1000 Euro tomorrow where would you invest it for best 5 year returns.

Here is what we would do

Put it in a globally diversified equity ETF, specifically something tracking MSCI World or S&P 500.

Why, it’s the the straightforward option:

Vanguard FTSE All-World UCITS ETF (VWCE) or iShares MSCI World UCITS ETF (IWDA)

Historically delivers 7-10% annualised returns over 5+ year periods

Low fees (0.20-0.22% TER)

Automatic diversification across 1,500-3,000+ companies

No need to pick individual stocks or time markets

But….there are alternatives you could have a slightly more aggressive alternative:

If you can stomach 20-30% drawdowns during the period, allocate 70% to global equities and 30% to a technology-focused ETF (Nasdaq-100 tracker). Tech has outperformed broader markets substantially over most 5 year windows, though past performance obviously doesn’t guarantee future results!!! Remember that.

And for the reckless investor!

Actually aggressive: Emerging market small caps. ETF tracking MSCI Emerging Markets Small Cap index

Higher growth potential from developing economies

Currency risk, political risk, liquidity risk all stacked up

Volatile but historically outperforms during risk-on periods

Could deliver 20%+ annualised or lose 40% and take years to recover

#investing #Risk #stocks #shares #InvestingStrategy

#PortfolioBuilding

#EquityInvesting

#WealthGrowth

#FinancialPlanning

Pancake Day portfolio rankings:

🥇 Plain with lemon and sugar — Vanguard FTSE All-World ETF. Classic. Reliable. Never lets you down. Nobody at the dinner table is impressed, but it quietly outperforms the fancy stuff.

🥈 Nutella — NVIDIA. Everyone wants it. Bit rich. You know you’re going to overdo it and feel sick later.

🥉 The one stuck to the ceiling — Your mate’s crypto pick from 2021. It’s not coming back down.

🏅 Banana and bacon — UK small caps. Sounds wrong. Works surprisingly well. Most people won’t try it because it looks weird.

What’s your portfolio pancake?

For fun.

The secret to a good pancake and a good portfolio are the same thing.

Most people flip too early.

They see a bit of browning on one side and panic. Turn it over. Mess it up. End up with something that looks like it’s been through a war.

The best pancakes need patience. You wait until the bubbles form. You trust the process. Then one clean flip.

Your stocks are the same. The browning isn’t a signal to sell. It’s the compounding doing its job.

Happy Pancake Day. Stop flipping your portfolio.

What’s the stock you flipped too early and still regret?

The balance sheet predicts bankruptcies years before they happen.

The problem is that most retail investors never look at it. They check the share price, maybe the P/E, and call it due diligence.

Five debt red flags that show up before the collapse:

1.Debt Maturity Wall

More than 40% of total debt maturing within 2 years. Forces refinancing at whatever rate the market decides. If conditions tighten, they’re trapped with no exit.

2.Interest Cover Below 2x

EBIT divided by interest expense dropping toward 1.0x. Below 2x means one bad quarter and they can’t service the debt from operations.

3.Rising Debt, Falling Revenue

Borrowing more while the top line shrinks. This is the corporate equivalent of paying your rent on a credit card.

4.Covenant Headroom Shrinking

How close are they to tripping their loan agreement triggers? Usually buried deep in the notes. When they stop disclosing the headroom figure, that’s when you should worry most.

5.Off-Balance Sheet Obligations

Operating leases, pension deficits, guarantees to subsidiaries. The debt that doesn’t appear on the front page of the balance sheet. Check Note 25 onwards.

How many flags does your largest holding have? Be honest.

Every investor has bought a stock because “it looks cheap.”

Most of them found out it was cheap for a reason.

There’s a difference between a stock that’s been unfairly beaten down and one that’s broken beyond repair. The trick is knowing which is which before your money teaches you the lesson.

Genuinely cheap: revenue stable or growing, FCF positive, insiders buying, P/E below its 5-year average by 30%+, debt manageable, clear catalyst for recovery, and the problem is the whole industry not just this company.

Actually broken: revenue declining, cash burn with no path to profit, insiders selling, P/E low because earnings are collapsing, covenants at risk, no turnaround plan, and the problem is specific to this company while peers are doing fine.

Seven checks on each side. Score your watchlist honestly.

If your “bargain” fails more than two on the green side, it’s not cheap. It’s a trap.

How many on your watchlist pass all seven?

CEOs don’t lie on earnings calls.

They just speak a language designed so you hear what you want to hear.

Once you learn to translate it, you’ll never listen to a call the same way again.

“We see significant opportunities ahead”

= Current operations are stalling. We need a new story to tell you.

“We’re investing heavily in the business”

= Margins are about to compress. Brace yourself.

“We remain confident in our long-term strategy”

= Short-term numbers are terrible and I’d rather not discuss them.

“We’re exploring strategic alternatives”

= The board is panicking. Fire sale or hostile bid incoming.

“Adjusted EBITDA was strong this quarter”

= Real earnings were awful so we invented a number where we look good.

The word “adjusted” in any earnings metric is the financial equivalent of “apart from that, Mrs Lincoln, how was the play?”

Tag someone who needs this before earnings season starts.

Every annual report is 200+ pages.

99% of it is filler. Legal boilerplate, sustainability waffle, photos of smiling employees.

You need three numbers. That’s it.

https://t.co/aLnz0CJGyB Cash Flow Yield (FCF / Market Cap)

Above 5%: the company is printing cash relative to its price.

Below 2%: you’re paying for perfection and perfection rarely shows up.

2.ROIC vs WACC

If Return on Invested Capital exceeds their cost of capital, they’re creating value. If it doesn’t, every pound they invest destroys wealth. Most investors never check this.

https://t.co/UfNsTJSZnL Debt to EBITDA

Below 2x: sleeping well at night.

Above 4x: one bad quarter from a covenant breach.

That’s 5 minutes of work that tells you more than any analyst report you’ll never finish reading.

What’s the first number you check? Reply below.

@Investingcom No one reading this should care about “this week” your own title is INVESTING not speculating!!!!

People: thing longer term. Much longer.

Follow me for smart advice not “pretend quick wins”

READ THIS it’s important

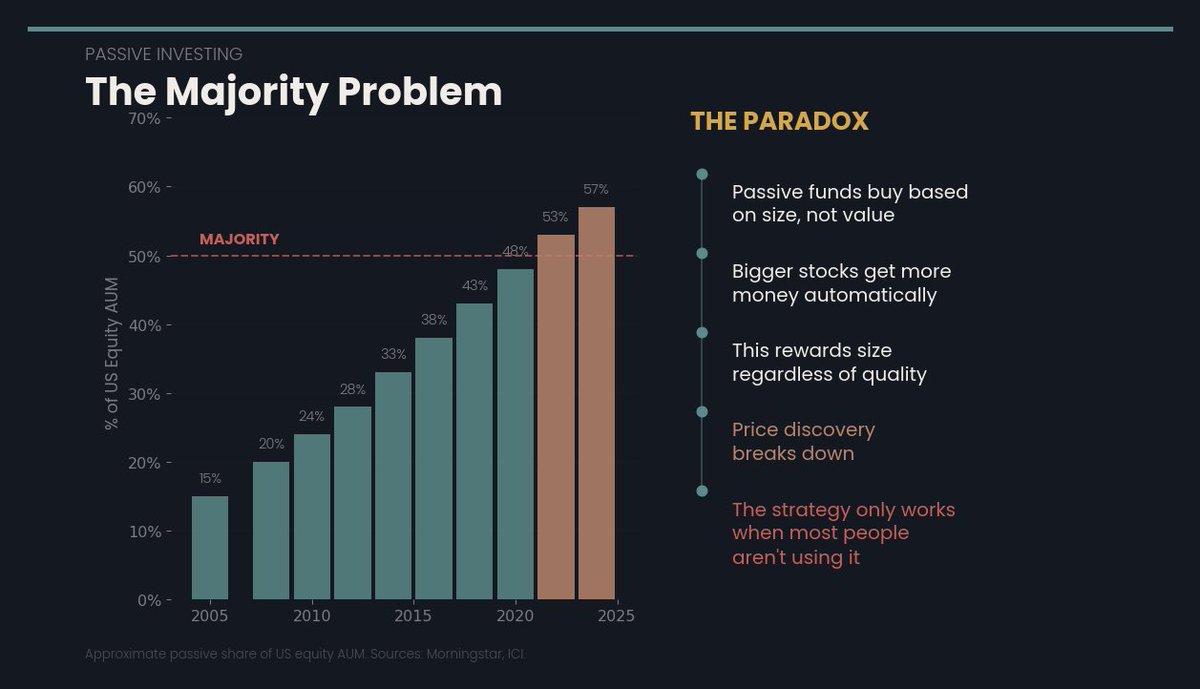

“Passive investing” is the most successful marketing campaign in financial history.

You’ve been told that paying someone 0.03% to track an index is the smart, rational choice.

What you weren’t told:

When everyone buys the index, the biggest companies in the index get bigger simply because they’re already big. Not because they’re good.

Tesla at 1,200x earnings got MORE money flowing in from passive funds, not less. The index doesn’t care about valuation. It just buys.

Passive investing works brilliantly when it’s a minority strategy.

When it becomes the dominant strategy, it breaks the very price discovery mechanism that made it work in the first place.

You’re not being smart. You’re being late to a trade that depends on other people being smart on your behalf.

And fewer and fewer of them are bothering.

Agree? Disagree? Quote this with your take.