One week of negative yield to build the reserve that enables more preferred stock issuance, which is the actual positive yield engine. They’ve produced positive BTC yield every single year since 2020. $MSTR

$MSTR’s original model generated positive Bitcoin yield by selling common stock at a premium, then by issuing preferred stock at coupons below Bitcoin’s expected appreciation. Now @Saylor is forcing common shareholders to accept a negative Bitcoin yield just to prop up Bitcoin.

The $100M reserve prevents forced BTC sales like last week’s which wiped 17% off $MSTR It also improves credit quality, unlocking more preferred stock issuance to buy BTC without diluting shareholders. Saylor owns 10% of MSTR so he’s getting diluted too.

so saylor just continued selling mstr shares, $100M to buy bitcoin & $100M to their cash reserves

if he's just gonna commit to diluting mstr holders & buying btc until it goes back up i vote we just ignore bro altogether

MicroStrategy has

- 1500 employees

- almost $100b in Assets (at the peak prices)

- "best team/strategy guys" in finance

And not a single person asked a question why they ran their Cash Reserves to ±6 months runway

???

bunch of yes-men, dangerous game

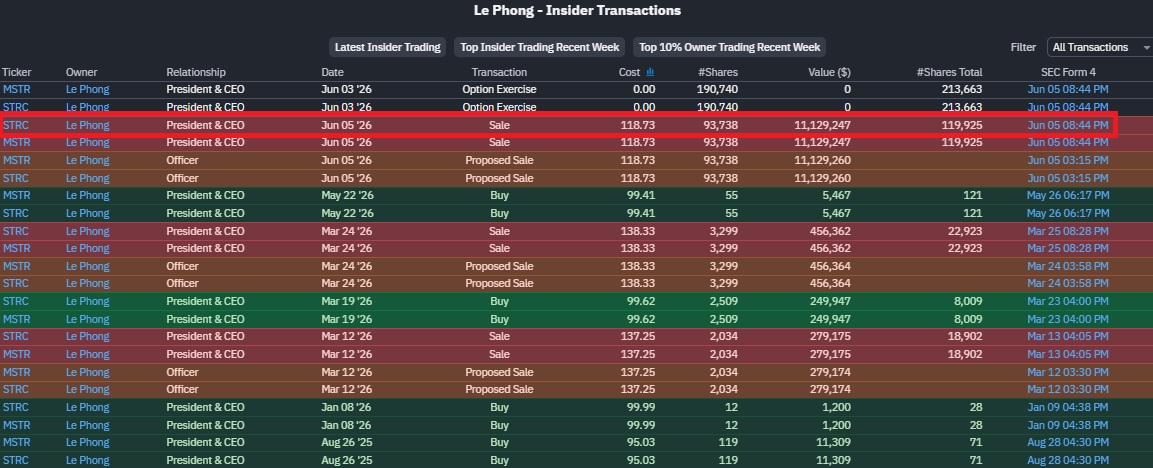

This sale was scheduled over a year ago and he had no say in the timing. He just received ~190k shares as a bonus, sold ~84k to pay the tax bill on them, and kept the rest. His overall holding actually went up. Nothing to see here.

He doesn’t need to sell anything. Debt is covered by convertible notes that repay or convert to equity, dividends covered by cash reserves, new BTC bought through common and preferred ATM issuance. He can sell the Bitcoin, he just doesn’t have to.

Both sales were scheduled over a year ago to cover the tax bill when their bonus shares vested. Neither had a choice on timing or amount. They both kept far more than they sold. Just two executives paying the IRS.

FTX comparison doesn’t hold. SBF had no real assets, just rehypothecated customer funds. Strategy holds 843,706 actual Bitcoin, audited, on a public balance sheet anyone can verify. That’s the opposite of fraud.

If Saylor doesn’t stop fucking around with leverage trying to be cute MicroStrategy will fail.

I 1000% believe that.

Don’t give me your shit on the math he tells you either. Sam told us logical math as well right before FTX took down the market.

Greed = fucks you. Period

This sale was scheduled over a year ago and he had no say in the timing. He just received ~190k shares as a bonus, sold ~84k to pay the tax bill on them, and kept the rest. His overall holding actually went up. Nothing to see here.

He sold to pay a tax bill on shares that just vested, pre-planned since May 2024, and kept 120,000 shares worth $14M. That’s not a man who thinks MSTR is unsafe. MSTR isn’t just Bitcoin exposure, it’s leveraged BTC accumulation per share. Different instrument, different thesis.

Selling $11m because he realizes $MSTR is not safe for his portfolio. Only people that buy it are playing with greed.

If you want Bitcoin exposure buy Bitcoin.

The reserve dropped because they chose to spend $1.38B buying back convertible notes at an 8% discount. That’s retiring debt profitably, not desperation. Still $900M cash, $26B ATM capacity, and 843,706 BTC as backstop. Not a company on the edge.

There's a bunch of DATs that FOMOd billions at the top and there is so much fraud there they haven't even started unwinding

Saylor has 6 months cash runway, so he needs to sell, otherwise if he stops the dividends $STRC goes to $0 and he evaporates $10 Billion of investors money

Misleading framing. BlackRock didn’t sell anything. These are clients redeeming their ETF shares. BlackRock just processes it. That’s like saying Vanguard sold stocks because someone cashed out their 401k.

He sold 32 BTC out of 843,706 to cover a preferred dividend, not to prove anything. That’s 0.004% of the stack. Bitcoin didn’t drop 20% because Saylor sold, it dropped because of Middle East tensions, ETF outflows and macro risk off. Correlation isn’t causation.

Saylor sold 32 $BTC to "prove it had value" and he did indeed prove Bitcoin had 20% less value than expected so I'd say that was a successful experiment

@ActuallyClimber His $15.7M in 2024 was 94% equity tied to performance targets including shareholder return. Saylor took a $1 salary and no equity. A typical S&P500 CEO takes $20M+ in cash regardless of performance. He’s more aligned with shareholders than most.

@TedPillows This sale was scheduled over a year ago and he had no say in the timing. He just received ~190k shares as a bonus, sold ~84k to pay the tax bill on them, and kept the rest. His overall holding actually went up. Nothing to see here.

@ActuallyClimber This sale was scheduled over a year ago and he had no say in the timing. He just received ~190k shares as a bonus, sold ~84k to pay the tax bill on them, and kept the rest. His overall holding actually went up. Nothing to see here.