Got reached out by a head hunter for a potential associate role at KKR APAC. Any thoughts?

For context, I am currently in an associate role in an LMM PE focused on SEA buyout.

Story time: When I first started in short activism as a CPA (you’d be surprised... basically no short activists doing accounting work actually have a CPA license, BTW), my boss sent me on a wild goose chase targeting GT Advanced Technologies $GTAT. They claimed to be making unbreakable sapphire screens for the next iPhone, but the CEO was dumping stock like crazy.

Boss’s orders: Camp out at their factory for a week and literally count cars in and out. (I was a pure spreadsheet junkie before this.) CEO goes on @CNBC defending his sales as a 10b5-1 plan (it wasn’t) and bragging that the factories were running day and night on the Apple deal. Reality? Max 10 cars all week. Then bam, random filing the next week, bankruptcy, stock to $0, most assets surrendered to Apple. Never seen anything like it. We’ve seen a lot of wild stuff in the short biz over the years.

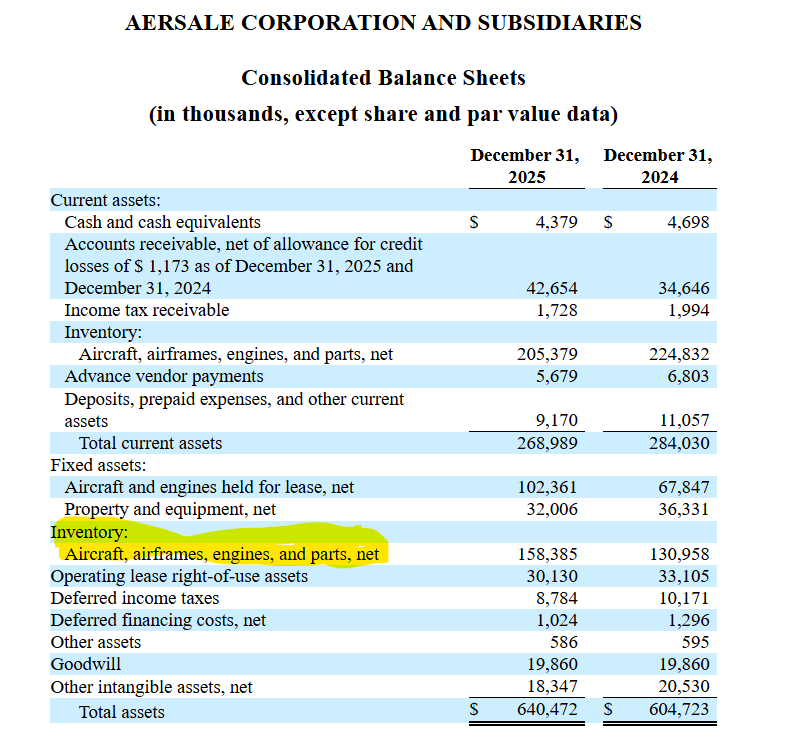

But with $EIF $EIF.TO, it’s the first time I’ve come across an accounting trick I genuinely haven’t seen anyone else pull. A direct peer like AerSale correctly moves aged inventory into long-term assets. Exchange Income Corp hides its aged-out inventory inside Capital Assets (dodging most DSI screens we use), then applies an obscure inventory valuation method I’ve never encountered before. Even as an accounting professor who’s seen pretty much everything. It lets them manufacture artificial margins.

Props to management for the creativity… but we believe it will reverse hard and end badly. Time will tell.

Would love to hear the craziest accounting gimmicks you’ve come across!

Citadel Securities published this graph showing a strange phenomenon.

Job postings for software engineers are actually seeing a massive spike.

Classic example of the Jevons paradox. When AI makes coding cheaper, companies actually may need a lot more software engineers, not fewer.

When software is cheaper to build, companies naturally want to build a lot more of it. Businesses are now putting software into industries and tools where it was simply too expensive before.

---

Chart from

citadelsecurities .com/news-and-insights/2026-global-intelligence-crisis/

The CEO of a $95 billion company just said something that should TERRIFY every software executive on the planet.

Patrick Collison, the man who built Stripe, went on TBPN last week and compared the entire software industry to frozen food.

His words: "Software has been created years beforehand, freeze-dried, and then prepared at the moment of consumption."

That era is ending.

His new model for software? Pizza.

Fresh pizza, made to order, right then and there.

Exactly what you need, the moment you need it.

That is the future Collison sees for all software.

What does that actually mean?

It means AI agents will build you custom software in real time.

No subscriptions, bloated dashboards and one size fits all.

Software cooked for you, that moment, then gone.

This is already happening.

Anthropic launched Claude Cowork in January.

Within weeks, $2 trillion in software stocks evaporated.

IBM had its worst trading day in 26 years, legalZoom dropped 20% and the entire SaaS sector is in freefall.

They're calling it the SaaSpocalypse.

The old software model was simple, spend millions building a product, sell it to everyone and collect subscriptions forever.

Fixed cost, infinite monetization and winner takes all.

That game created trillion dollar companies: Salesforce. Adobe, Oracle, Microsoft.

Collison says that game is now breaking.

Why? Because AI introduces real cost at every use.

Inference costs, custom creation costs, every single interaction has a price tag.

No more build once, sell forever and he called it the non-Walrasian software regime.

Translation: The winner take all economics that built Big Software are collapsing.

When every user gets custom software built on demand, there is no single winner.

There are thousands of winners or none.

Think about what this does to pricing.

No more $50/seat/month or enterprise contracts worth millions.

Instead, you pay per task, outcome and for what the AI actually built you.

The entire revenue model of SaaS is being rewritten.

Klarna already ripped out Salesforce and replaced it with AI.

Cursor ditched its paid CMS and built a replacement from scratch.

Companies are doing this now.

The dominoes are falling.

The entire industry is being rewritten in real time.

Imagine: Two animals run the exact same distance.

One chooses to. One is forced.

The voluntary runner gets healthier—better heart rate, blood pressure, glucose.

The forced runner? Gets sicker.

Andrew Huberman says the same rule destroys or upgrades your stress, your workouts, even your life.

And the craziest proof: People who watched hours of Boston bombing news coverage suffered MORE acute stress than those who were actually there.

Your mind doesn’t know the difference between experiencing and relentlessly consuming.

So… what “have-to” in your life are you ready to reframe as a choice?

This 1:58 clip just rewired my brain.

Good rule in investing (& life tbh) is don’t waste time w/ ppl who nitpick on your every exact word when your message is clear enough to anyone w/ even a modestly analytical brain (an ok assumption in this line of work?)

Effective way to filter out bullshit artists / ppl who add no value while trying to diminish your thoughts just bc they want to hear themselves talk & can’t push back w/ actual substance

I’ve found this Deep Research prompt to be a decent way to get up to speed on any company.

Very little focused on valuation, more of a holistic overview

I can’t for the life of me remember where I found the original seven-point framework/template but I fleshed it out to 13 to hit the areas I felt were important. If anyone recognizes it, please link/tag the creator

—————

Analyze [Ticker] using the 13-point framework below.

- Use only verifiable, factual information (annual reports, investor presentations, filings, earnings transcripts, and reputable financial sources).

- Be concise, analytical, and concrete, with no filler or marketing language.

Output format (exact structure required):

Executive Summary (about 150–200 words)

Summarize in plain English how this company makes money, its economic quality, and where its edge and risks lie.

End with one sentence that describes the business to an investor in one line.

1. What They Sell and Who Buys

* Describe the main products or services.

* Define target customers by type, segment, and geography, and why they buy, including the main pain point or motivation.

2. How They Make Money

* Explain the revenue model and pricing logic.

* Clarify whether revenues are one-time, recurring, transaction-based, or hybrid.

* Include key revenue segments and their share if available.

3. Revenue Quality

* Assess how predictable and diversified revenues are.

* Break down recurring versus one-off components, customer or segment concentration, and exposure to economic cycles.

4. Cost Structure

* Outline major cost drivers, such as COGS, labor, logistics, marketing.

* Include gross and operating margins where possible.

* Comment on scalability, fixed versus variable costs, and how margins move with growth.

5. Capital Intensity

* Describe the assets needed to run and grow operations.

* Include capital expenditure levels, working capital needs, and cash conversion efficiency.

6. Growth Drivers

* Identify the main levers for revenue growth, such as volume, pricing, product mix, geographic expansion, or acquisitions.

* Clarify whether each driver is structural and long term or cyclical and short term.

7. Competitive Edge

* Explain what protects the company’s economics from competition, such as brand, cost advantage, switching costs, regulation, network effects, data, or intellectual property.

* Discuss how durable and testable this moat appears, using financial evidence such as margins, ROIC, or customer retention.

8. Industry Structure and Position

* Describe the industry value chain and where profit pools sit.

* Explain market structure, for example fragmented or consolidated, presence of pricing power, and key regulatory factors.

* Place the company within this context, including market share, relative scale, and whether it acts as a price setter, a price taker, a niche specialist, or a platform.

9. Unit Economics and Key KPIs

* Present unit economics at the relevant level, such as per customer, store, device, transaction, or cohort.

* Include metrics such as CAC, LTV, churn or retention, ARPU, utilization, occupancy, and payback periods where applicable.

* Comment on whether these unit economics and KPIs are improving, stable, or weakening over time.

10. Capital Allocation and Balance Sheet

* Summarize historical capital allocation across organic investment, acquisitions, buybacks, dividends, and debt reduction.

* Describe balance sheet strength, including leverage, debt maturity profile, liquidity, and any major off balance sheet obligations.

* Assess whether capital allocation has likely created or destroyed value.

11. Risks and Failure Modes

* Identify key risks, such as competitive, technological, regulatory, macroeconomic, customer concentration, or currency exposure.

* Describe in simple terms how the equity story could fail, and what would need to happen for this to occur.

* Highlight areas where uncertainty is especially high or information is limited.

12. Valuation and Expected Return Profile

* Compare current valuation with the company’s own history and with peers, using the metrics that best fit this business, such as P/E, EV/EBIT, EV/Sales, FCF yield.

* Provide a simple scenario framework with bear, base, and bull cases, including rough assumptions and implied upside or downside.

* State explicitly what must be true for the current price to be attractive, fair, or expensive.

13. Catalysts and Time Horizon

* List near and medium term catalysts, such as product launches, margin inflection, regulatory events, refinancing, or index changes.

* Note any slow building catalysts, such as mix shift or operating leverage that accumulates over time.

* Explain the expected time horizon for the thesis to play out and how the market is likely to recognize the value if the thesis is correct.

Tone: Analytical, neutral, precise.

Goal: Produce a concise yet rich narrative that lets an investor understand how this business works, how resilient and valuable its economics are, and whether the stock looks attractive at today’s price.

One the most common questions I get on here is around management incentive programs- the sweat equity award for PE operators.

Makes sense... these programs are the #1 reason to be a private equity operator. They can be life changing (believe me).

But these incentive programs (which go by all kinds of acronyms: LTIPs, MIPs, MIEPs...) can be extremely complicated.

So below, I have compiled a list of questions to help you evaluate the equity opportunity.

These programs are often highly structured and complicated. It is important to realize that their value is not just in your ability or the company's potential - it also lies in how the program is structured.

The questions below are intended to help you evaluate the potential value an equity award when considering a role within a PE-backed portfolio company.

These questions will demonstrate you have some understanding of the mechanisms behind these programs and the key drivers behind creating value.

And, it forces the PE firm to reveal assumptions they may be glossing over.

Even if they get a little squirmy, they will be impressed with your understanding and it will likely increase your leverage.

Couple notes...

- I've added a 🔑 logo next to the ones I thought were most important

- Some questions are bigger than just the structure, but they will help you evaluate the value to you personally

- I've left some similar/repetitive questions in as they appear in a different context/section

Hope you find this helpful...

Comment with any additions and I will try to compile a follow-up to this so we all have a collective resource.

-----

1. Structure & Terms

Mechanics

- What form of equity am I receiving (options, profits interests, RSUs, phantom equity, direct units)? (helps understand tax implications) 🔑

- What is the total size of the management equity pool? Has it been reset before?

- How many executives participate in it, and how are allocations typically adjusted over time?

Vesting & Triggers

- Is vesting time-based, performance-based, or hybrid? 🔑 *beware time & performance based i.e. IRR and MOIC which can make hitting thresholds much harder

- What are the hurdles for each vesting tranche? 🔑

- Are the hurdles based on PE firm performance, overall performance, or something else? 🔑

- What are the specific time-based cliffs and intervals? 🔑

- What happens to unvested equity on an early exit, recap, or sale?

- Is there accelerated vesting on change of control or termination without cause? 🔑

Valuation

- What is my strike price or unit price at grant?

- How was that price determined (latest 409A or transaction value)?

- What is the expected range of unit prices at various IRR/MOIC outcomes? 🔑

- What is the window and process to exercise after departure?

- Are taxes due on exercise or only at liquidity? 🔑

Liquidity & Exit

- When can I actually convert equity to cash? Only at exit or also at recaps?

- Are management participants allowed to sell pro rata in secondary or recap events?

- Are there drag-along or tag-along rights for management?

- Is there any right of first refusal or forced sale language?

- What is the post-exit lockup, if any?🔑

Dilution & Co-Invest

- What is expected dilution from future issuances, M&A, or refresh grants? 🔑 (I like this question just to hear how the firm thinks about it)

- Will I have the option to co-invest cash alongside the fund? On what terms? 🔑 (you should be able to invest on same terms as PE firm, otherwise, don't do it)

- How are future refresh grants handled if the hold extends beyond the expected period?🔑

I built an analysis of the 50 best and WORST industries for acquisition in 2025.

50 industries. 20 factors. one ranking per industry.

To get a copy of the analysis, RT and comment "industries"

I like the biography of Ed Thorp because it highlights a less popular path to success than what is in fashion today. Ed leads a life of wonder in many different fields, stumbling into several monumental achievements along the way. He meets Buffett at 35 and invests in Berkshire, he is the first LP in Citadel, he invents the first wearable computer with Claude Shannon, he launches the first quant hedge fund, has a very successful marriage, and he somehow always looks thirty years younger than he is. The book tells of how he is able to jump into some esoteric thing, master it against all odds, and then bail out and move on to the next thing without a care in the world. What’s most striking is his ability to just have enough and walk away.

Thorp is the super-genius version of the very common archetype of a person who just can't commit to one thing and therefore never does anything of note, except that he is such a genius he achieves 99th-percentile outcomes in everything in which he dabbles. This is in itself quite remarkable, but one cannot help but imagine that there is an alternative path for Thorp in which he doesn’t dabble and wins a Fields Medal, becomes Ken Griffin or James Simons, or at least ends up as the greatest gambler in history.

One cannot help but wonder if Thorp could have elevated himself to the pantheon of world greats instead of being this kind of very underrated, interesting guy, who had all these run-ins with and influence on these historical figures.

In an interview shortly before he died, Kobe had this idea about how the next twenty years of his career were going to vastly outshine the last twenty years. Of course, there is no possible way this is true, both in a literal sense and not. And yet it is quite common. You get the feeling George Clooney might really believe that his satellites over Darfur are his most important contribution, or Gates with his foundation. What’s common is a certain amount of denial that the greatest thing the person will ever do is behind them. It indicates a kind of longing for a Thorp or Feynman or Rooseveltian existence where every chapter gets more interesting than the last. Where they intersect with many great events and great men, but their great work seems to be the collage of their lives in toto. The young and ambitious like to say that each successive thing one does in their career ought to make the previous appear like a mere footnote in their hypothetical biography. I am not so convinced. Maybe it is life itself that should be so grand that it reduces any particular thing to a footnote.

Ultimate Market and Commercial Diligence Template

How the big shop's frame an asset and vet the CEO’s plan

Quote post, follow (so we can auto DM), like and comment to get a copy

DMing first will break the automation

WILL AI DESTROY YOUR SOFTWARE COMPANY? OR: WHICH SOFTWARE COMPANY SHOULD I BUILD?

I'm a software private equity investor. I look at 10-20 software businesses each week to acquire. I see good, bad, and everything in between.

***I am reposting this since apparently all the pods think software is cooked (it isn't)***

I keep getting this freaking dm 'Now that I can build ANY software company with AI (lol) what should I build?'

I've also seen this nonsense going around of 'software is dead'. I'm going to address both of these here.

First things first, software is not just software. Software exists across a variety of dimensions/attributes. We have to cover these as they play a massive role in which software will be 'fine' and which software is 'at risk'. This should also tell you indie builders out there which software to go after.

For the purposes of this exercise, I'm going to use a darling example company to analyze these attributes: Calendly.

Here are some of the attributes I think about when I look at acquiring a business:

1) 'time to yes': How long does it take to sell your software after a customer learns about it? Is it a 3-6 month sales cycle? Is time to yes instant? DO I NEED TO TALK TO SOMEONE ON THE PHONE TO PURCHASE IT? If, like calendly, I can buy it myself with my corporate card? Time to yes has knock on effects on so much: price, churn, etc. It is an important attribute to cover. Calendly's time to yes can be instant.

2) 'implementation time': Software that takes a long time to implement. I call this 'implementation time'. Others in my space call it something else. This is the amount of time it takes between wiring the money and the company actually USING the software. An example might be vertical software for a veterinarian. It could take a full month to configure the software, get all the users onboarded, work through bugs, etc. How long does it take to implement calendly? Well about 4-5 minutes.

3) 'Time to Utility': This is the time between 'the customer can actually use the software' and 'the customer has derived utility'. If we are using calendly as an example, again this near instant. If this is vertical SAAS for managing a veterinary clinic, this time might be a month or two. Sure the software is making the business run 'smoother' but the time to utility might be longer than you think.

4) 'Tear Out Time': some people call this switching cost, but I delineate the two. How long does it take a customer to 'tear it out' and switch? This is NOT the same as switching cost, although some people mistakenly (imo) lump them together. This is measured in TIME. Calendly's tear out time? Near instant for most people.

5) Switching Cost: How much does it cost me to switch? This can be a real number. Let's say I want to switch my CRM from Salesforce to Attio. Not only do I have a probably high 'tear out time', I also have to pay SOMEONE to migrate my sales data from Salesforce to Attio. There's a real dollar cost here, even if Attio claims to have the softawre to do it. What's my switching cost from Calendly to Cal? ...near 0.

6) ACV: Average contract value. Finally we get to price. How much are you charging for your software? If you are Salesforce, this could be 20k. If you're calendly? 8 bucks a month.

7) Churn: self explanatory.

8) Data Moat / Network Effects: Does your business collect data that is difficult to collect via LLM? Do you have data that drives product utility that is difficult to attain? Do you have network effects?

THESE ATTRIBUTES ARE THE LENSE THROUGH WHICH YOU SHOULD THINK ABOUT SOFTWARE.

Now, getting back to the question: 'will AI destroy my software company?'. Buddy, if you have high time to yes, a high implementation time, and a low time to utility, AI is unlikely to cook your software company. AI DOES NOT REPLACE A 3 MONTH SALES CYCLE AND A HIGH IMPLEMENTATION TIME. Customers are NOT just going to churn because some guy is billing half as much. CEOs value time and attention. If your software is mission critical, tear out time is high, AND switching cost is high? No one is churning. If you ask a CTO if they would tear out Gitlab to save 50%, they'd probably laugh in your face.

Now: to the inverse. Let's talk about Calendly. Calendly is the perfect example of a business that I think will be in trouble due to AI. Why? (I'm a calendly customer btw)

1) My time to yes is instant. If someone comes to me with a $2 a month replacement, I can instantly say yes.

2) My implementation time is instant. I cancel calendly. I synch my email to new service. Done.

3) Time to utility is instant.

4) TEAR OUT TIME IS 5 MINUTES. YIKES! This is problematic software.

5) Switching cost: Near 0.

6) No data moat. No network effects (rly).

To all you indie hackers out there: these are the types of businesses you might want to copy. Why? YOU DON'T NEED AN ENTERPRISE SALES TEAM TO SELL YOUR PRODUCT. Like it or not, even if AI can make a copy of software, spoiler alert you have to go out and SELL IT. There's a reason some B2B SAAS companies NEED venture funding: the sales cycles (time to yes, imp time, time to uitlity) ARE LONG LOL. You NEED those venture dollars to sell this software that will (hopefully) have a very low churn rate. Many of these businesses are fine. Their main problem is people above and below them in the vertical chain. Not addressing this here.

What's that mean? DISTRIBUTION MATTERS MORE THAN EVER. If calendly can be copied, learning how to distribute in a low cost way becomes more valuable than ever before in software. SEO. Partnerships. Large scale cold email. Having influencers on board from day 0. These things matter even MORE.

So is software dead? Hell no...but companies like calendly will surely have some problems.

So to you boot strappers out there, here's what you want:

1) Time to yes can be instant.

2) Time to utility should be as fast as possible.

3) Low Implementation time.

4) Keep price low enough that someone can say 'yes' without needing to call you on the phone but high enough that can make some serious dough.

5) Hopefully find a way to get data that's hard for someone else to get. That'll help with competition and switching cost.

YOU WILL HAVE CHURN. But you can also build a 5mm ARR business with 4 employees.

Good luck anon

https://t.co/DvD5vhSx05

Re-post this tweet, message us your email, and we’ll send through our model on Floor & Decor ($FND).

If you’ve done this before and didn’t receive a model that’s our fault - DM us again and we’ll be sure to send it.

assorted thoughts on fintwit, on L/S equity, fund management, analyst vs pm, knowledge of self, mental capital…some lesser known, underdiscussed parts of the game…long, loooong thread.