Our guiding principles:

→ 100% Fee Transparency (We will disclose what we get from the AMC upfront, so you know we are not pushing high commission funds.)

→ We will NOT push an NFO (We know NFOs are incentivized to build the book of AMCs, but you can buy after listing.)

→ We will NOT chase/spam you for investing. (We will ask once, and then that's it. We do not have sales targets. Asking more than once is a sign of begging.)

→ We will NOT ask you why you are withdrawing funds. (It's your money, you can do whatever you like with it.)

→ We will be truthful with you. (In good times, and in bad.)

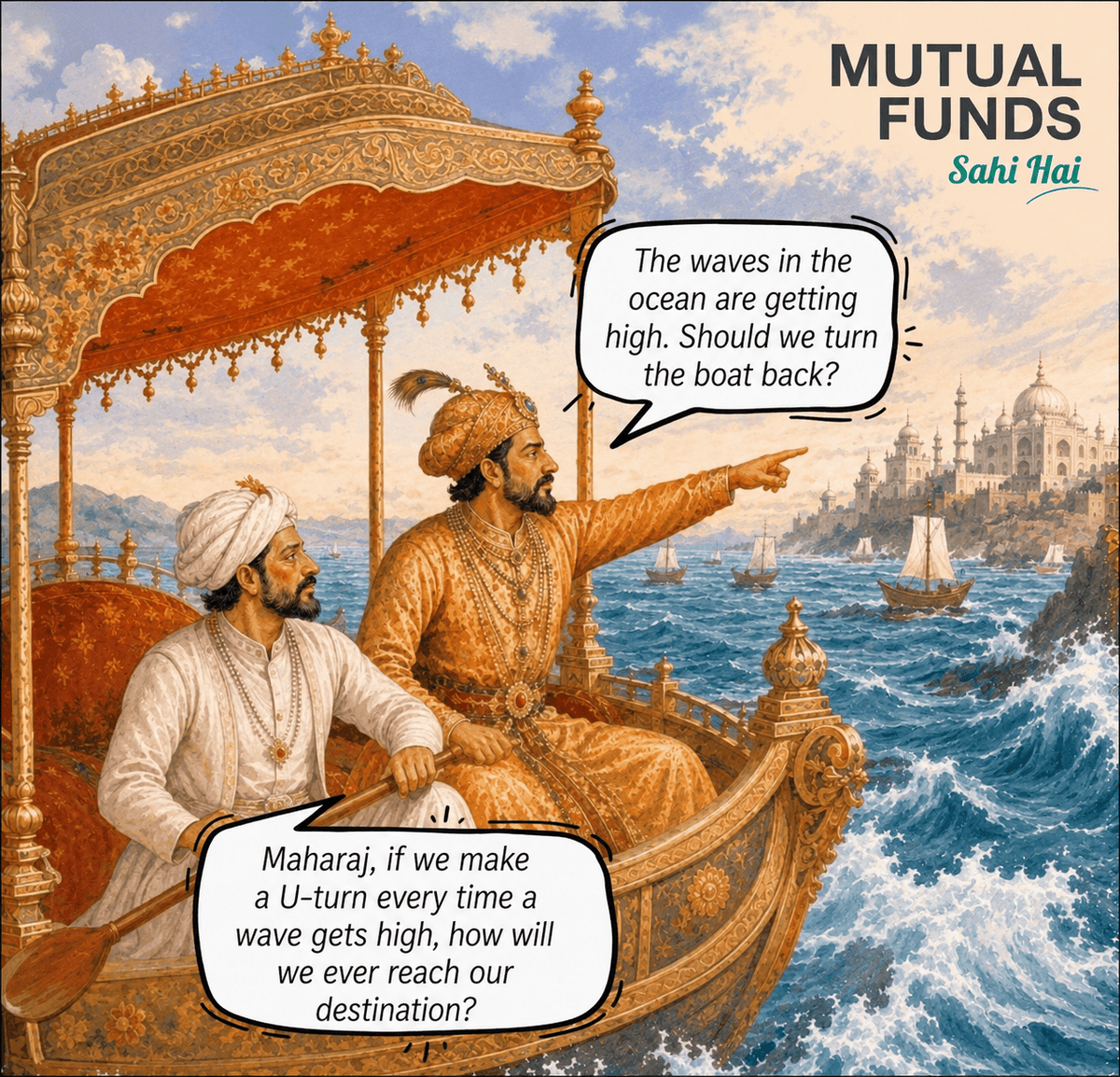

A client shared this with us, nice analogy. We translated this to English for a wider audience in the south.

What it means in investing

The boat = your investment journey.

The destination = your financial goals.

The waves = market crashes, corrections, volatility, bad news, elections, wars, etc.

The king = the nervous investor.

The navigator/captain = the experienced advisor.

If you stop investing, redeem your mutual funds, or keep changing direction every time markets become volatile, you may never reach your long-term financial goals.

But... ignoring every wave is not wisdom either.

If the destination is wrong, the boat is damaged, or the navigator is incompetent, changing course may be exactly the right decision.

Don’t abandon a sound long-term plan because of temporary volatility. But do reassess when the fundamentals change.

#mutualfundssahihai

Looking to secure your future? 💰

Considering ULIPs for investment and insurance, or term insurance for pure protection?

Before you jump into a ULIP, PLEASE read this...

✨ #ULIP#TermInsurance#SIP

👇🏼

https://t.co/ms3MVpSwZ5

@deepakshenoy The govt could introduce Tax Free Bonds again, that would bring in a good corpus and reverse the tide.

The last time the govt introduced tax free bonds, plenty of NRIs had invested.

We talked about this earlier. AMC are also facing delays in getting their brokerages and GST stuff sorted out.

@amfiindia sufficient time should have been given to roll this change out. A more centralized approach would have been better to smoothen the GST collection.

If you're a Mutual Fund Distributor with under ₹20L turnover, your monthly income just dropped ~15%.

Permanently.

From 1 April 2026.

On the same AUM, the same investors, the same AMCs.

Most of your peers haven't done the math yet.

Here's the field manual we wish someone had handed us. 🧵

DSPNetra May 2026 edition is here.

This is the 60th edition of DSPNetra.

When we began, the intent was simple: to deliver factful, data-backed, and unbiased insights.

The method was to put these insights together in a way that was useful, authentic, and independent.

It was never about catering to any section of the market.

It was never about playing to the gallery.

The intent remains the same.

Forecast-free. Data-backed. Authentic.

We don’t know where we are going.

But we can make an attempt to understand where we are.

Read the thread or download:

https://t.co/EAs0OFwzfX

Wrapping up.

This is not legal or tax advice. Read it as field notes from one MFD shop to another. Talk to your CA before acting on anything.

If this was useful:

• Save the thread. The full picture is here — there's no separate long-form to chase down.

• Share with one MFD friend who hasn't run the post-1-April math yet.

• Reply with corrections. We'd rather be wrong publicly and fixed publicly than wrong privately and stuck.

If you're a CA or GST counsel and any item in tweet 18 has a settled answer in your practice — please reply directly to that tweet with the cite. The MFD community needs the cleanup.

Last thing — the mental hinge that made this regime change clarifying for us: once you accept that

1% inclusive ≡ 0.85% base + 0.153% GST

every downstream economic outcome falls out of one question: who keeps which slice of the split?

The whole field manual is just answering that one question for four MFD profiles.

— Team BayFolio

If you're a Mutual Fund Distributor with under ₹20L turnover, your monthly income just dropped ~15%.

Permanently.

From 1 April 2026.

On the same AUM, the same investors, the same AMCs.

Most of your peers haven't done the math yet.

Here's the field manual we wish someone had handed us. 🧵

Where we want CAs and GST counsel to weigh in.

These are the items in our master reference still tagged ⚠️ Verify or ⚡ Contested. Reply or quote-tweet if you have a settled view:

1. ⚡ §24(vii) "agent" classification — strongest current ruling either way?

2. ⚠️ Retro-penalty posture for sub-20L MFDs with un-filed returns from 2017–2025. AMFI has been lobbying for §74 (willful evasion) waiver. Status?

3. ⚠️ Does the new BER apply to OLD AUM (pre-1 Apr 2026 SIPs and folios), or only to flows after that date? Need a SEBI clause cite.

4. ⚠️ Canonical CAMS / KFin policy page on the exact monthly invoice cycle dates (10–15, 15–25, ~30, by 20, ~14). We could not find a single consolidated source.

5. ⚠️ Platform spread numbers (AssetPlus / Wealthy / NJ / Prudent) — current AMC empanelment slab grids would settle the "30–40 bps better than tiny ARN" claim.

6. ⚠️ The 2016–17 RCM → FCM service-tax notification number for MFD commission. Practitioner narrative is firm; the actual notification is elusive.

7. ⚠️ FD interest in the aggregate-turnover test — included in the test even though exempt from output GST?

If you've answered any of these in your own practice, please share. The MFD community will benefit from a settled position.