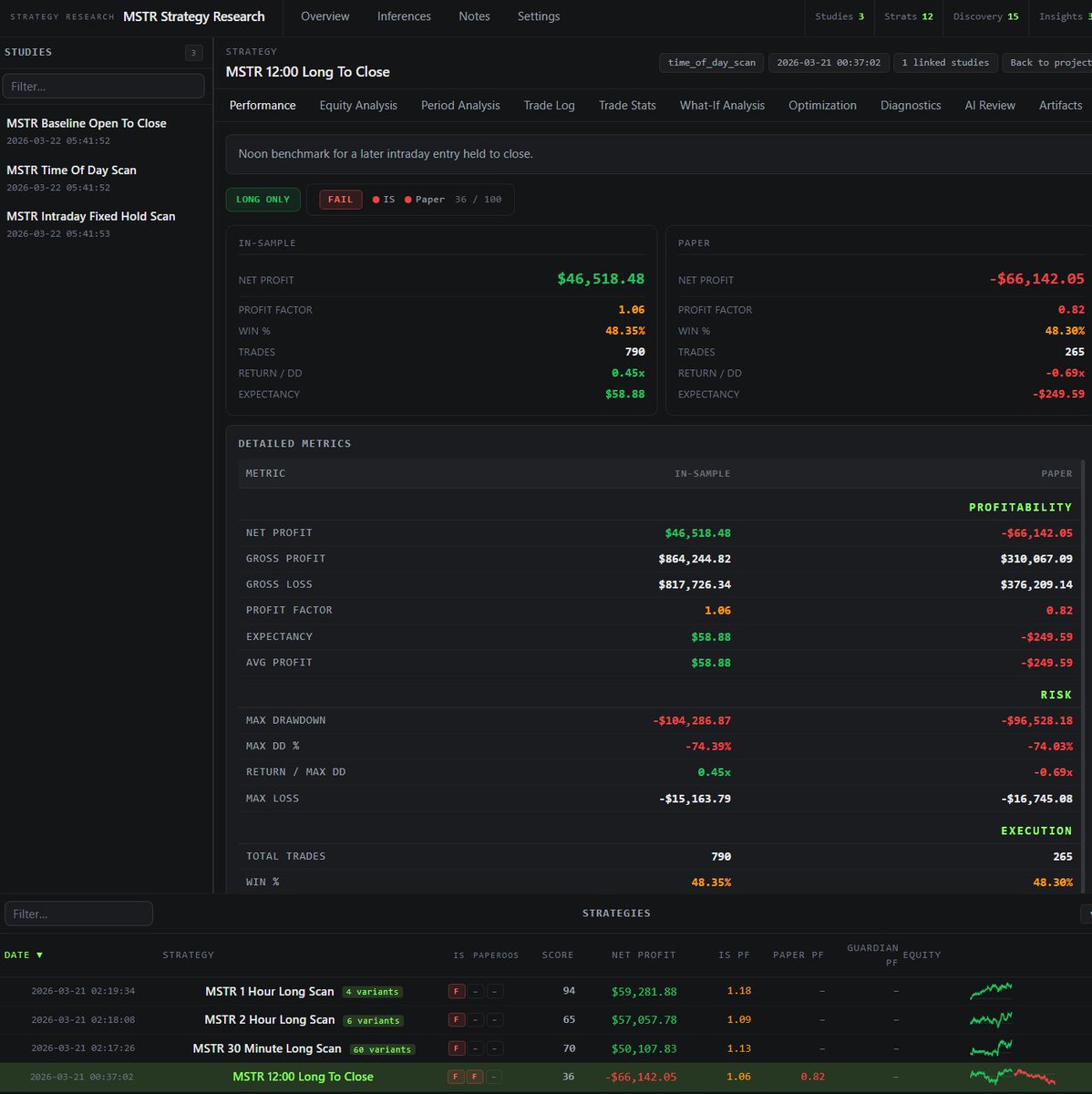

Introducing the Agentic Strategy Lab (ASL).

It looks like a trading app. But it is not a traditional backtesting engine.

It is an agentic strategy engine. You bring the ideas. AI agents write the code, run the analysis, and validate the edge automatically. Zero manual coding.

The most gangsta thing Michael Saylor could announce Monday would be that they sold huge quantity of Bitcoin at the highs raising cash warchest for STRC, got a tax credit, and then rebought the lows pulling his average price down significantly...

But let's be honest... Saylor and company more likely got super bullish at the peak and didn't take any major actions.

Overtrading or under-trading?

Many traders concern themselves with overtrading while others claim there is no such thing as over trading. There is even argument to be made that most day traders who fail are more likely those that take fewer trades. In fact, I think the latter is more directionally true. Yet, we also hear about traders who are very selective and that makes all the difference.

All these claims feel like a giant paradox but resolve once you understand certain fundamental truths of trading.

The first fundamental truth of trading is that if you become loose in one area or aspect you must become tighter in another: it is a conservation constraint.

If you want to place more trades, you need lower costs but you must tighten up your pricing constraint or fill quality.

If you place fewer trades, each trade bears more weight thus the quality of trade needs to be higher. If you place fewer trades, the cost of missing good trades is higher and the fill quality becomes less relevant.

If you take more trades, necessarily the quality per trade will decrease which mandates the risk per trade should be less. If you demand less evidence per trade then you must tighten up the risk management.

Once you understand the constraint nature driving everything then you understand why would want to take more trades or fewer trades and more importantly how to do it.

The paradoxes resolve.

Arguments for trading more frequently:

- It is generally easier to figure out what is good pricing then to profitably predict direction.

- By taking more trades you can reduce the risk per trade.

- You prioritize flexibility and adaptation.

- Your cost structure is lower.

- You value trading experience and real-time feedback.

- You have ability to size smaller.

- Typically taking more trades you will be providing liquidity which serves a useful function in the market place.

It is also easier to understand why one may want to take fewer trades:

- Typically taking fewer trades means you will be demanding liquidity.

- You want to maximize the edge per trade.

- You want to scale up size.

- You prioritize evidence when entering trade.

- Your cost structure is higher.

- You will be helping price discovery which serves a useful function in the market place.

That said, as retail traders we generally don't have a structural edge in liquidity provision which means some things are still true regardless:

- Stop losses and/or daily loss limits are required.

- Selectivity is required.

- Patience is required.

- Scaling plan is needed.

- Focus on process and improvement is key.

- Ability to step away from the action and stop is important.

- The biggest account destroyers often come from a few large losing days. When taking liquidity, it can look like getting chopped up in flat markets with large size whereas when providing liquidity those days are often trend days that keep running past all expectations.

- Size should only be scaled up with evidence. Trying to trade bigger size is one of the fastest way to destroy an account.

Tradestation Tip: Average Price

The average price tab in Tradestation serves the equivalent function of floor trader cards in the old days. It tells you what your average on the day is.

This is invaluable if you hold shares to compute your actual day trading profits and ignore FIFO pricing-- also very useful if you average into or work positions to know your basis cost.

Below are my click trades.... Think I over trade? I like to click a lot but even I have learned the necessity of patience.

Be Dario Amodei

- Get a job at OpenAI, quit, and take half-the-company with you to start Anthropic.

- Build the most opinionated, condescending, annoying, gaslighting, censored, and throttled AI model of all time: Claude. Make it good at one thing: writing. But when that's not enough shift to focus on being the best at coding.

- Go on a tour claiming that open source AI is dangerous and needs to be regulated.

- When that fails, go on tour claiming that AI will replace all software engineers within 6 months every 6 months. Even though even their latest Opus model gets tripped up with basic mathematics.

- When that fails, go on tour claiming that AI is entering the self-improving era and needs to be slowed down.

Contrast with Google-- just building and shipping.

Despite all their benefits, LLMS are still notoriously unreliable.

I catch at least 5 to 10 false, inaccurate, or confabulated claims in every response they produce. In past, I have found Google's fast Gemini/search model multiple times giving dangerously inaccurate medical advice.

That said, I have also used LLMs like Gemini and GPT Pro on real-world medical topics that far surpassed what the average doctor would know and that would require a team of medical experts -- on multiple medical topics.

I have also used them to solve hard problems.

However, Yann Lecun was right: these are knowledge models masquerading as intelligence models.

One reason LLMS aren't very smart: they talk too much. They have to emit, yap, talk. Smart people say very little because there's very little that one can say confidently.

The architecture necessarily means you get lots of inaccuracies, mistakes, confabulations, distortions, etc.

A true ASI would say very little but would do a lot. Exact opposite of LLMs. And when it did speak, it would be something to pay attention too.