This will eventually send much higher imo, just a matter of time

$ETHFI is one of the very few things that I might actually be willing as a "longterm investment" rn

already fully vested and card metrics keep printing new aths every week

bitcoin w1

honestly the similarities in this cycle compared to the last is crazy

of course it doesn't look exactly the same, there is much more money in bitcoin now

but it's following the same script, just different actors

price action is a display of human emotion

$CLX - Defensive stock breaking out that covers consumer staples from Clorox cleaning products like wipes and bleach, ranch dressing, burt bees, brita filters, and charcoal.

USA Rare Earth $USAR: Government Giveth, Government Taketh Away

By Hataf Capital

The rare earths sector is not for the faint of heart. If you want a masterclass in volatility, just look at USA Rare Earth, Inc. $USAR, which recently doubled off its lows only to surrender a massive chunk of those gains in a matter of weeks.

It’s a classic case of the market struggling to price a company that is essentially trying to reshore an entire industry that the West effectively abandoned decades ago.

While the headlines are focused on a massive $3.1 billion government-backed capital raise, the underlying story is more complex.

We are seeing a strategic tug-of-war where the U.S. government is finally putting real capital on the table, but at a cost that is both dilutive to current shareholders and potentially exposed to the pricing whims of Beijing.

Despite the noise, my investment thesis remains bullish, as USA Rare Earth is positioning itself as the critical, vertically integrated answer to China's near-monopoly on the minerals that power everything from F-35s to the semiconductors in your pocket.

The Trump Investment: A High-Stakes Lifeline

Last week, USA Rare Earth dropped a bombshell regarding its capital structure. The company announced a massive $3.1 billion raise that, frankly, looks like a restructuring of the entire bull case. Here is how the math breaks down:

$1.3 billion in a senior secured loan via the CHIPS Act.

$277 million via 16.1 million shares priced at $17.17.

$300 million from 17.6 million warrants also at $17.17.

$1.5 billion from a private capital raise at a premium $21.50 per share.

The market’s immediate reaction was a mix of relief and "sticker shock" over the dilution. By issuing over 103 million shares, the company is diluting existing holders by more than 50%.

However, this isn't your typical desperate penny-stock dilution. This is a strategic entry by the U.S. Department of Commerce under President Trump’s push for the government to take equity stakes in exchange for critical infrastructure support.

What’s interesting here is the shift in the timeline. The company was previously looking at a 2030 start for its Round Top mine in Texas, but has now pulled that forward to late 2028.

When you’re trying to build a $4.1 billion "manufacturing fortress" that includes magnet production in Oklahoma and heavy rare earth mining in Texas, you need a "big bazooka" of capital.

With a 2025 year-end cash balance of only ~$350 million, this multi-billion-dollar infusion was the only way to turn these "science experiments" into an industrial reality.

The "China Problem" and the Lack of Pricing Guarantees

Now, let's address the elephant in the room: the January 29th selloff. The market took a hit when it became clear that the government deal did not include the pricing floors that investors were desperately hoping for.

The fear is simple: the Chinese government has a long history of weaponizing its supply chain by undercutting prices to bankrupt Western upstarts.

Many expected a deal similar to what MP Materials secured in 2025, which provided a safety net against predatory pricing.

CFO William Steele’s defense of this was telling. He argues that because Round Top produces minerals like dysprosium, terbium, and yttrium which are in "dramatic undersupply" outside of China the market itself will provide the floor.

I’ll be frank: that’s a bold bet on rational market behavior in an arena that is historically irrational.

However, there is a practical interpretation of this data that the bears are missing. Sophisticated buyers in the aerospace and defense sectors are no longer just looking for the cheapest price; they are looking for supply security.

A 15% premium for a "Made in USA" magnet is a rounding error in a multi-billion-dollar fighter jet program, but a lack of that magnet is an existential threat.

Valuation: A 2030 Vision at a 2026 Price

If we look at the projected 2030 revenue target of ~$2.6 billion and an adjusted EBITDA of $1.2 billion, the valuation starts to look like a massive anomaly.

At a fully diluted share count of ~280 million, we’re looking at a market cap of roughly $6.2 billion.

Trading at just 5x 2030 adjusted EBITDA, the stock is being priced as if these competitive disadvantages are permanent, while its strategic advantages are temporary.

Under any rational valuation framework, a company with this kind of manufacturing leverage and operational lock-in should command a premium, not a discount.

Of course, there are hurdles. The U.S. lacks the "tribal knowledge" of rare earth processing, and the path to 2030 will likely be littered with operational "yield bottlenecks" and higher-than-expected costs.

Your Takeaway

USA Rare Earth is a classic asymmetric risk/reward play. The market is handing us a gift wrapped in fear because it can't handle the "lumpiness" of government deal-making and the lack of a pricing safety net.

The reality is that the "Stargate" of Al and defense infrastructure requires these minerals. As the scarcity of these products becomes more apparent, the 50% dilution we’re seeing today will look like a small price to pay for the "Manufacturing Fortress" being built in Texas and Oklahoma.

I would look to buy the stock on this current weakness. We are in the earliest stages of a decade-long reshoring cycle, and sometimes the smartest move is to let the hype burn out before the fundamentals bring everyone back to reality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]

For those who aren’t aware yet, @IncomeSharks is on Slice.

If you had been subscribed, here’s the performance you would have had last night on $FLNC.

👉 https://t.co/rhpYqxge5k

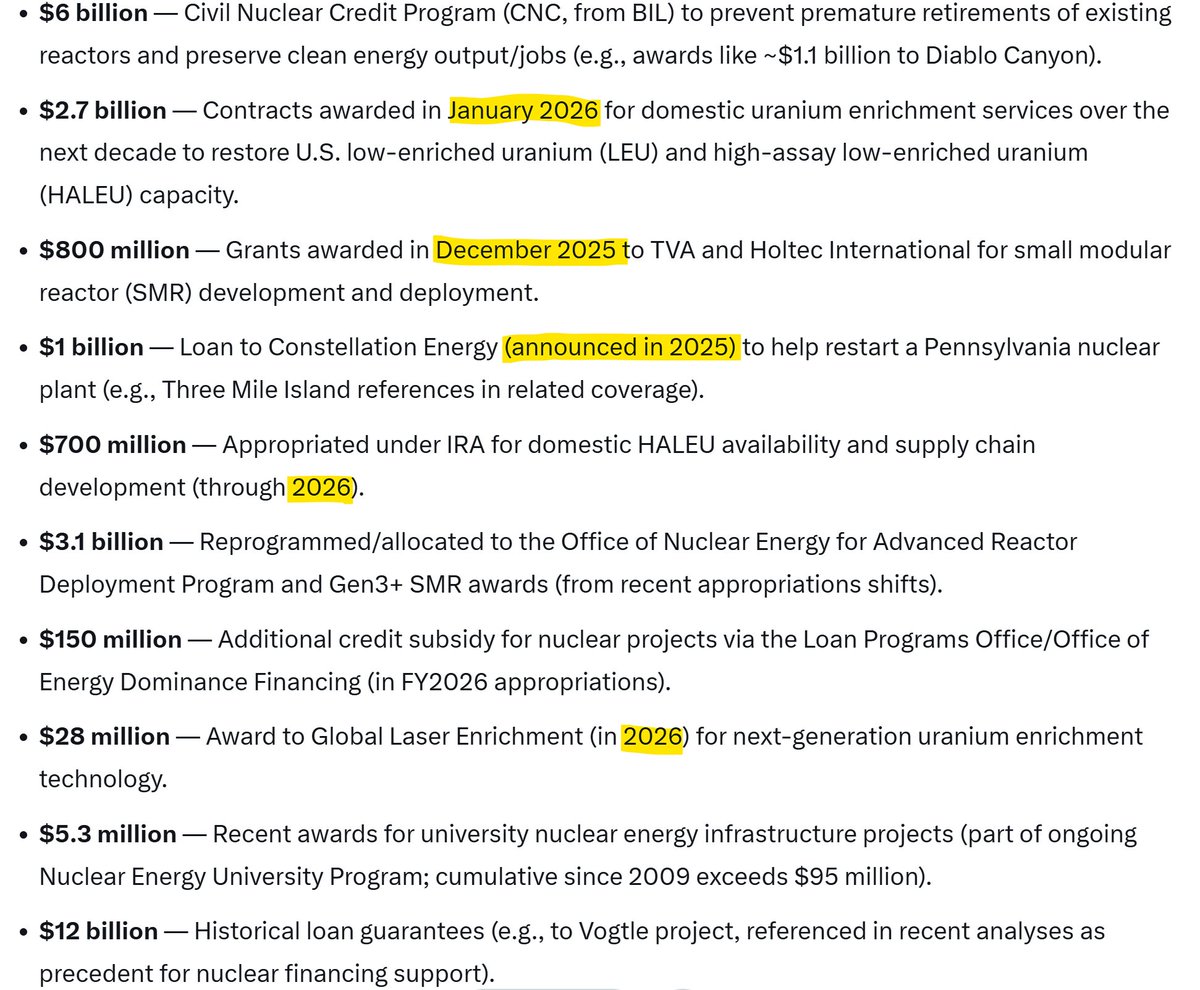

The Department of Energy has been ramping up Nuclear investments faster than ever before. Worth having exposure for the next 5 years as the battle for energy will only get bigger.

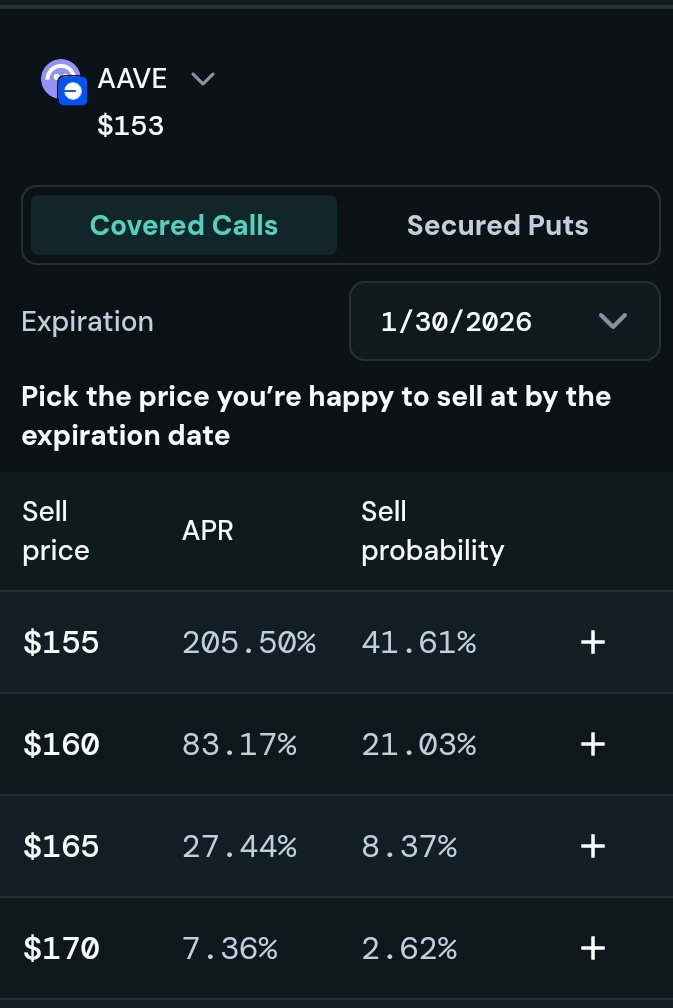

Honestly, seeing 205% APR on $AAVE made me pause for a second.

I’m just setting a price I’m already happy to buy at, getting paid upfront in USDT and still earning triple digit yield while I wait.

This feels way calmer than staring at charts all day hoping not to get wicked out.

Slow, paid and stress free is starting to look like my kind of trading.

@hypersurfaceX really changed how I think about earning in this market.

$MNT still one of my fav alts

> Neobanking platform launching

> Bybit integration

> Mantle Vault on Bybit: $100M+ TVL in under a month

> RWA focus

@Mantle_Official x @Bybit_Official taking over 2026 🚀

You'll have more wins with smaller positions. Big positions just mean you'll over manage, over stress, sell too early and see bigger drawdowns (and often close before it comes back). The only way to fight greed and impatience is to focus on downside and go smaller than you think.

$IREN - Closed above the blue line, broke out of the OBV, and the last boss standing in the way is SuperTrend resistance. Flip that to green then you have 3/3 bullish confirmations.

![hataf_capital's tweet photo. USA Rare Earth $USAR: Government Giveth, Government Taketh Away

By Hataf Capital

The rare earths sector is not for the faint of heart. If you want a masterclass in volatility, just look at USA Rare Earth, Inc. $USAR, which recently doubled off its lows only to surrender a massive chunk of those gains in a matter of weeks.

It’s a classic case of the market struggling to price a company that is essentially trying to reshore an entire industry that the West effectively abandoned decades ago.

While the headlines are focused on a massive $3.1 billion government-backed capital raise, the underlying story is more complex.

We are seeing a strategic tug-of-war where the U.S. government is finally putting real capital on the table, but at a cost that is both dilutive to current shareholders and potentially exposed to the pricing whims of Beijing.

Despite the noise, my investment thesis remains bullish, as USA Rare Earth is positioning itself as the critical, vertically integrated answer to China's near-monopoly on the minerals that power everything from F-35s to the semiconductors in your pocket.

The Trump Investment: A High-Stakes Lifeline

Last week, USA Rare Earth dropped a bombshell regarding its capital structure. The company announced a massive $3.1 billion raise that, frankly, looks like a restructuring of the entire bull case. Here is how the math breaks down:

$1.3 billion in a senior secured loan via the CHIPS Act.

$277 million via 16.1 million shares priced at $17.17.

$300 million from 17.6 million warrants also at $17.17.

$1.5 billion from a private capital raise at a premium $21.50 per share.

The market’s immediate reaction was a mix of relief and "sticker shock" over the dilution. By issuing over 103 million shares, the company is diluting existing holders by more than 50%.

However, this isn't your typical desperate penny-stock dilution. This is a strategic entry by the U.S. Department of Commerce under President Trump’s push for the government to take equity stakes in exchange for critical infrastructure support.

What’s interesting here is the shift in the timeline. The company was previously looking at a 2030 start for its Round Top mine in Texas, but has now pulled that forward to late 2028.

When you’re trying to build a $4.1 billion "manufacturing fortress" that includes magnet production in Oklahoma and heavy rare earth mining in Texas, you need a "big bazooka" of capital.

With a 2025 year-end cash balance of only ~$350 million, this multi-billion-dollar infusion was the only way to turn these "science experiments" into an industrial reality.

The "China Problem" and the Lack of Pricing Guarantees

Now, let's address the elephant in the room: the January 29th selloff. The market took a hit when it became clear that the government deal did not include the pricing floors that investors were desperately hoping for.

The fear is simple: the Chinese government has a long history of weaponizing its supply chain by undercutting prices to bankrupt Western upstarts.

Many expected a deal similar to what MP Materials secured in 2025, which provided a safety net against predatory pricing.

CFO William Steele’s defense of this was telling. He argues that because Round Top produces minerals like dysprosium, terbium, and yttrium which are in "dramatic undersupply" outside of China the market itself will provide the floor.

I’ll be frank: that’s a bold bet on rational market behavior in an arena that is historically irrational.

However, there is a practical interpretation of this data that the bears are missing. Sophisticated buyers in the aerospace and defense sectors are no longer just looking for the cheapest price; they are looking for supply security.

A 15% premium for a "Made in USA" magnet is a rounding error in a multi-billion-dollar fighter jet program, but a lack of that magnet is an existential threat.

Valuation: A 2030 Vision at a 2026 Price

If we look at the projected 2030 revenue target of ~$2.6 billion and an adjusted EBITDA of $1.2 billion, the valuation starts to look like a massive anomaly.

At a fully diluted share count of ~280 million, we’re looking at a market cap of roughly $6.2 billion.

Trading at just 5x 2030 adjusted EBITDA, the stock is being priced as if these competitive disadvantages are permanent, while its strategic advantages are temporary.

Under any rational valuation framework, a company with this kind of manufacturing leverage and operational lock-in should command a premium, not a discount.

Of course, there are hurdles. The U.S. lacks the "tribal knowledge" of rare earth processing, and the path to 2030 will likely be littered with operational "yield bottlenecks" and higher-than-expected costs.

Your Takeaway

USA Rare Earth is a classic asymmetric risk/reward play. The market is handing us a gift wrapped in fear because it can't handle the "lumpiness" of government deal-making and the lack of a pricing safety net.

The reality is that the "Stargate" of Al and defense infrastructure requires these minerals. As the scarcity of these products becomes more apparent, the 50% dilution we’re seeing today will look like a small price to pay for the "Manufacturing Fortress" being built in Texas and Oklahoma.

I would look to buy the stock on this current weakness. We are in the earliest stages of a decade-long reshoring cycle, and sometimes the smartest move is to let the hype burn out before the fundamentals bring everyone back to reality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/HAKm5ZDaEAA90Pz.jpg)

![hataf_capital's tweet photo. USA Rare Earth $USAR: Government Giveth, Government Taketh Away

By Hataf Capital

The rare earths sector is not for the faint of heart. If you want a masterclass in volatility, just look at USA Rare Earth, Inc. $USAR, which recently doubled off its lows only to surrender a massive chunk of those gains in a matter of weeks.

It’s a classic case of the market struggling to price a company that is essentially trying to reshore an entire industry that the West effectively abandoned decades ago.

While the headlines are focused on a massive $3.1 billion government-backed capital raise, the underlying story is more complex.

We are seeing a strategic tug-of-war where the U.S. government is finally putting real capital on the table, but at a cost that is both dilutive to current shareholders and potentially exposed to the pricing whims of Beijing.

Despite the noise, my investment thesis remains bullish, as USA Rare Earth is positioning itself as the critical, vertically integrated answer to China's near-monopoly on the minerals that power everything from F-35s to the semiconductors in your pocket.

The Trump Investment: A High-Stakes Lifeline

Last week, USA Rare Earth dropped a bombshell regarding its capital structure. The company announced a massive $3.1 billion raise that, frankly, looks like a restructuring of the entire bull case. Here is how the math breaks down:

$1.3 billion in a senior secured loan via the CHIPS Act.

$277 million via 16.1 million shares priced at $17.17.

$300 million from 17.6 million warrants also at $17.17.

$1.5 billion from a private capital raise at a premium $21.50 per share.

The market’s immediate reaction was a mix of relief and "sticker shock" over the dilution. By issuing over 103 million shares, the company is diluting existing holders by more than 50%.

However, this isn't your typical desperate penny-stock dilution. This is a strategic entry by the U.S. Department of Commerce under President Trump’s push for the government to take equity stakes in exchange for critical infrastructure support.

What’s interesting here is the shift in the timeline. The company was previously looking at a 2030 start for its Round Top mine in Texas, but has now pulled that forward to late 2028.

When you’re trying to build a $4.1 billion "manufacturing fortress" that includes magnet production in Oklahoma and heavy rare earth mining in Texas, you need a "big bazooka" of capital.

With a 2025 year-end cash balance of only ~$350 million, this multi-billion-dollar infusion was the only way to turn these "science experiments" into an industrial reality.

The "China Problem" and the Lack of Pricing Guarantees

Now, let's address the elephant in the room: the January 29th selloff. The market took a hit when it became clear that the government deal did not include the pricing floors that investors were desperately hoping for.

The fear is simple: the Chinese government has a long history of weaponizing its supply chain by undercutting prices to bankrupt Western upstarts.

Many expected a deal similar to what MP Materials secured in 2025, which provided a safety net against predatory pricing.

CFO William Steele’s defense of this was telling. He argues that because Round Top produces minerals like dysprosium, terbium, and yttrium which are in "dramatic undersupply" outside of China the market itself will provide the floor.

I’ll be frank: that’s a bold bet on rational market behavior in an arena that is historically irrational.

However, there is a practical interpretation of this data that the bears are missing. Sophisticated buyers in the aerospace and defense sectors are no longer just looking for the cheapest price; they are looking for supply security.

A 15% premium for a "Made in USA" magnet is a rounding error in a multi-billion-dollar fighter jet program, but a lack of that magnet is an existential threat.

Valuation: A 2030 Vision at a 2026 Price

If we look at the projected 2030 revenue target of ~$2.6 billion and an adjusted EBITDA of $1.2 billion, the valuation starts to look like a massive anomaly.

At a fully diluted share count of ~280 million, we’re looking at a market cap of roughly $6.2 billion.

Trading at just 5x 2030 adjusted EBITDA, the stock is being priced as if these competitive disadvantages are permanent, while its strategic advantages are temporary.

Under any rational valuation framework, a company with this kind of manufacturing leverage and operational lock-in should command a premium, not a discount.

Of course, there are hurdles. The U.S. lacks the "tribal knowledge" of rare earth processing, and the path to 2030 will likely be littered with operational "yield bottlenecks" and higher-than-expected costs.

Your Takeaway

USA Rare Earth is a classic asymmetric risk/reward play. The market is handing us a gift wrapped in fear because it can't handle the "lumpiness" of government deal-making and the lack of a pricing safety net.

The reality is that the "Stargate" of Al and defense infrastructure requires these minerals. As the scarcity of these products becomes more apparent, the 50% dilution we’re seeing today will look like a small price to pay for the "Manufacturing Fortress" being built in Texas and Oklahoma.

I would look to buy the stock on this current weakness. We are in the earliest stages of a decade-long reshoring cycle, and sometimes the smartest move is to let the hype burn out before the fundamentals bring everyone back to reality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/HAKmxtEaIAAo5dS.jpg)

![hataf_capital's tweet photo. USA Rare Earth $USAR: Government Giveth, Government Taketh Away

By Hataf Capital

The rare earths sector is not for the faint of heart. If you want a masterclass in volatility, just look at USA Rare Earth, Inc. $USAR, which recently doubled off its lows only to surrender a massive chunk of those gains in a matter of weeks.

It’s a classic case of the market struggling to price a company that is essentially trying to reshore an entire industry that the West effectively abandoned decades ago.

While the headlines are focused on a massive $3.1 billion government-backed capital raise, the underlying story is more complex.

We are seeing a strategic tug-of-war where the U.S. government is finally putting real capital on the table, but at a cost that is both dilutive to current shareholders and potentially exposed to the pricing whims of Beijing.

Despite the noise, my investment thesis remains bullish, as USA Rare Earth is positioning itself as the critical, vertically integrated answer to China's near-monopoly on the minerals that power everything from F-35s to the semiconductors in your pocket.

The Trump Investment: A High-Stakes Lifeline

Last week, USA Rare Earth dropped a bombshell regarding its capital structure. The company announced a massive $3.1 billion raise that, frankly, looks like a restructuring of the entire bull case. Here is how the math breaks down:

$1.3 billion in a senior secured loan via the CHIPS Act.

$277 million via 16.1 million shares priced at $17.17.

$300 million from 17.6 million warrants also at $17.17.

$1.5 billion from a private capital raise at a premium $21.50 per share.

The market’s immediate reaction was a mix of relief and "sticker shock" over the dilution. By issuing over 103 million shares, the company is diluting existing holders by more than 50%.

However, this isn't your typical desperate penny-stock dilution. This is a strategic entry by the U.S. Department of Commerce under President Trump’s push for the government to take equity stakes in exchange for critical infrastructure support.

What’s interesting here is the shift in the timeline. The company was previously looking at a 2030 start for its Round Top mine in Texas, but has now pulled that forward to late 2028.

When you’re trying to build a $4.1 billion "manufacturing fortress" that includes magnet production in Oklahoma and heavy rare earth mining in Texas, you need a "big bazooka" of capital.

With a 2025 year-end cash balance of only ~$350 million, this multi-billion-dollar infusion was the only way to turn these "science experiments" into an industrial reality.

The "China Problem" and the Lack of Pricing Guarantees

Now, let's address the elephant in the room: the January 29th selloff. The market took a hit when it became clear that the government deal did not include the pricing floors that investors were desperately hoping for.

The fear is simple: the Chinese government has a long history of weaponizing its supply chain by undercutting prices to bankrupt Western upstarts.

Many expected a deal similar to what MP Materials secured in 2025, which provided a safety net against predatory pricing.

CFO William Steele’s defense of this was telling. He argues that because Round Top produces minerals like dysprosium, terbium, and yttrium which are in "dramatic undersupply" outside of China the market itself will provide the floor.

I’ll be frank: that’s a bold bet on rational market behavior in an arena that is historically irrational.

However, there is a practical interpretation of this data that the bears are missing. Sophisticated buyers in the aerospace and defense sectors are no longer just looking for the cheapest price; they are looking for supply security.

A 15% premium for a "Made in USA" magnet is a rounding error in a multi-billion-dollar fighter jet program, but a lack of that magnet is an existential threat.

Valuation: A 2030 Vision at a 2026 Price

If we look at the projected 2030 revenue target of ~$2.6 billion and an adjusted EBITDA of $1.2 billion, the valuation starts to look like a massive anomaly.

At a fully diluted share count of ~280 million, we’re looking at a market cap of roughly $6.2 billion.

Trading at just 5x 2030 adjusted EBITDA, the stock is being priced as if these competitive disadvantages are permanent, while its strategic advantages are temporary.

Under any rational valuation framework, a company with this kind of manufacturing leverage and operational lock-in should command a premium, not a discount.

Of course, there are hurdles. The U.S. lacks the "tribal knowledge" of rare earth processing, and the path to 2030 will likely be littered with operational "yield bottlenecks" and higher-than-expected costs.

Your Takeaway

USA Rare Earth is a classic asymmetric risk/reward play. The market is handing us a gift wrapped in fear because it can't handle the "lumpiness" of government deal-making and the lack of a pricing safety net.

The reality is that the "Stargate" of Al and defense infrastructure requires these minerals. As the scarcity of these products becomes more apparent, the 50% dilution we’re seeing today will look like a small price to pay for the "Manufacturing Fortress" being built in Texas and Oklahoma.

I would look to buy the stock on this current weakness. We are in the earliest stages of a decade-long reshoring cycle, and sometimes the smartest move is to let the hype burn out before the fundamentals bring everyone back to reality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/HAKmqgXa4AAmzPa.jpg)

![hataf_capital's tweet photo. USA Rare Earth $USAR: Government Giveth, Government Taketh Away

By Hataf Capital

The rare earths sector is not for the faint of heart. If you want a masterclass in volatility, just look at USA Rare Earth, Inc. $USAR, which recently doubled off its lows only to surrender a massive chunk of those gains in a matter of weeks.

It’s a classic case of the market struggling to price a company that is essentially trying to reshore an entire industry that the West effectively abandoned decades ago.

While the headlines are focused on a massive $3.1 billion government-backed capital raise, the underlying story is more complex.

We are seeing a strategic tug-of-war where the U.S. government is finally putting real capital on the table, but at a cost that is both dilutive to current shareholders and potentially exposed to the pricing whims of Beijing.

Despite the noise, my investment thesis remains bullish, as USA Rare Earth is positioning itself as the critical, vertically integrated answer to China's near-monopoly on the minerals that power everything from F-35s to the semiconductors in your pocket.

The Trump Investment: A High-Stakes Lifeline

Last week, USA Rare Earth dropped a bombshell regarding its capital structure. The company announced a massive $3.1 billion raise that, frankly, looks like a restructuring of the entire bull case. Here is how the math breaks down:

$1.3 billion in a senior secured loan via the CHIPS Act.

$277 million via 16.1 million shares priced at $17.17.

$300 million from 17.6 million warrants also at $17.17.

$1.5 billion from a private capital raise at a premium $21.50 per share.

The market’s immediate reaction was a mix of relief and "sticker shock" over the dilution. By issuing over 103 million shares, the company is diluting existing holders by more than 50%.

However, this isn't your typical desperate penny-stock dilution. This is a strategic entry by the U.S. Department of Commerce under President Trump’s push for the government to take equity stakes in exchange for critical infrastructure support.

What’s interesting here is the shift in the timeline. The company was previously looking at a 2030 start for its Round Top mine in Texas, but has now pulled that forward to late 2028.

When you’re trying to build a $4.1 billion "manufacturing fortress" that includes magnet production in Oklahoma and heavy rare earth mining in Texas, you need a "big bazooka" of capital.

With a 2025 year-end cash balance of only ~$350 million, this multi-billion-dollar infusion was the only way to turn these "science experiments" into an industrial reality.

The "China Problem" and the Lack of Pricing Guarantees

Now, let's address the elephant in the room: the January 29th selloff. The market took a hit when it became clear that the government deal did not include the pricing floors that investors were desperately hoping for.

The fear is simple: the Chinese government has a long history of weaponizing its supply chain by undercutting prices to bankrupt Western upstarts.

Many expected a deal similar to what MP Materials secured in 2025, which provided a safety net against predatory pricing.

CFO William Steele’s defense of this was telling. He argues that because Round Top produces minerals like dysprosium, terbium, and yttrium which are in "dramatic undersupply" outside of China the market itself will provide the floor.

I’ll be frank: that’s a bold bet on rational market behavior in an arena that is historically irrational.

However, there is a practical interpretation of this data that the bears are missing. Sophisticated buyers in the aerospace and defense sectors are no longer just looking for the cheapest price; they are looking for supply security.

A 15% premium for a "Made in USA" magnet is a rounding error in a multi-billion-dollar fighter jet program, but a lack of that magnet is an existential threat.

Valuation: A 2030 Vision at a 2026 Price

If we look at the projected 2030 revenue target of ~$2.6 billion and an adjusted EBITDA of $1.2 billion, the valuation starts to look like a massive anomaly.

At a fully diluted share count of ~280 million, we’re looking at a market cap of roughly $6.2 billion.

Trading at just 5x 2030 adjusted EBITDA, the stock is being priced as if these competitive disadvantages are permanent, while its strategic advantages are temporary.

Under any rational valuation framework, a company with this kind of manufacturing leverage and operational lock-in should command a premium, not a discount.

Of course, there are hurdles. The U.S. lacks the "tribal knowledge" of rare earth processing, and the path to 2030 will likely be littered with operational "yield bottlenecks" and higher-than-expected costs.

Your Takeaway

USA Rare Earth is a classic asymmetric risk/reward play. The market is handing us a gift wrapped in fear because it can't handle the "lumpiness" of government deal-making and the lack of a pricing safety net.

The reality is that the "Stargate" of Al and defense infrastructure requires these minerals. As the scarcity of these products becomes more apparent, the 50% dilution we’re seeing today will look like a small price to pay for the "Manufacturing Fortress" being built in Texas and Oklahoma.

I would look to buy the stock on this current weakness. We are in the earliest stages of a decade-long reshoring cycle, and sometimes the smartest move is to let the hype burn out before the fundamentals bring everyone back to reality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/HAKnAPEaYAAnhjG.jpg)