Light up creativity with pixels. In the bead art world of Rialo, every bead is a fragment of inspiration, piecing together unique cuteness and ingenuity~ Come and see these little Rialo worlds made of bead art, does it touch your heart? ✨

@RialoHQ@itachee_x@gametheorizing@firearrowmage@rialo_zw

Tokenizing private credit is the easy part. The hard part is verifying that borrowers are actually complying with loan covenants.

That gap is why onchain private credit has not worked yet.

In crypto lending today, to borrow $100 you must lock up $150. You need to be rich to borrow. This is the only model that works because the system doesn't know who you are.

In the real world, banks lend you more than you put down. Mortgages, credit cards, business loans. They can do this because they check your credit score, income, identity. Trust replaces collateral.

Rialo brings this to crypto. Borrowers can verify credentials (credit score, banking, identity, repayment history) to reduce their collateral requirement, potentially below 100%. The difference: unlike every other project attempting this, Rialo verifies the data without anyone seeing it. Private by default, revealed only if you default.

The global unsecured lending market is ~$4.7 trillion. On-chain lending is ~$56B, almost all over-collateralized. That gap is the opportunity.

We built a demo tool to show how the opportunity might work.

Toggle credentials, adjust loan size, watch collateral and rates update live.

The more information you provide, the less you need to put down to take a loan. It just makes sense.

Open the Pricing Engine at the bottom to see 6 different models for how this could work, including one designed for AI agent borrowers.

Link below:

The RWA section is the one to read twice.

You can't model risk from smoothed quarterly NAVs. Liquidation takes 30–90 days with 20–50% haircuts. The math breaks before it starts.

But the deeper issue is older than DeFi: garbage in, garbage out. Smart contracts enforce rules perfectly, but they can't determine whether the inputs are true. Someone still has to feed real-world borrower data on-chain. If that party has bad incentives, you've rebuilt TradFi with extra steps.

This is the oracle problem, applied to private credit.

DeFi solved it for price feeds. Nobody has solved it for bespoke financial instruments: covenant compliance, borrower performance, collateral quality. That's the verification gap, and it's why private credit on permissionless rails keeps stalling.

That's what we're building at Rialo.

Smart contract enforcement fixes the rules, but it doesn’t fix the truth. We need a determination layer that bridges the verification gap while keeping inputs private.

@soumeya from Subzero shared a writeup on the complexities of bringing private credit on chain.

The Lunar New Year vibe is building up! 🧧 Rialo is here with you waiting for the big day. May our community be as warm and lively as this art. Let’s thrive together in the Year of the Horse! 🐎✨ ✨

@RialoHQ@itachee_x@gametheorizing@firearrowmage@rialo_zw

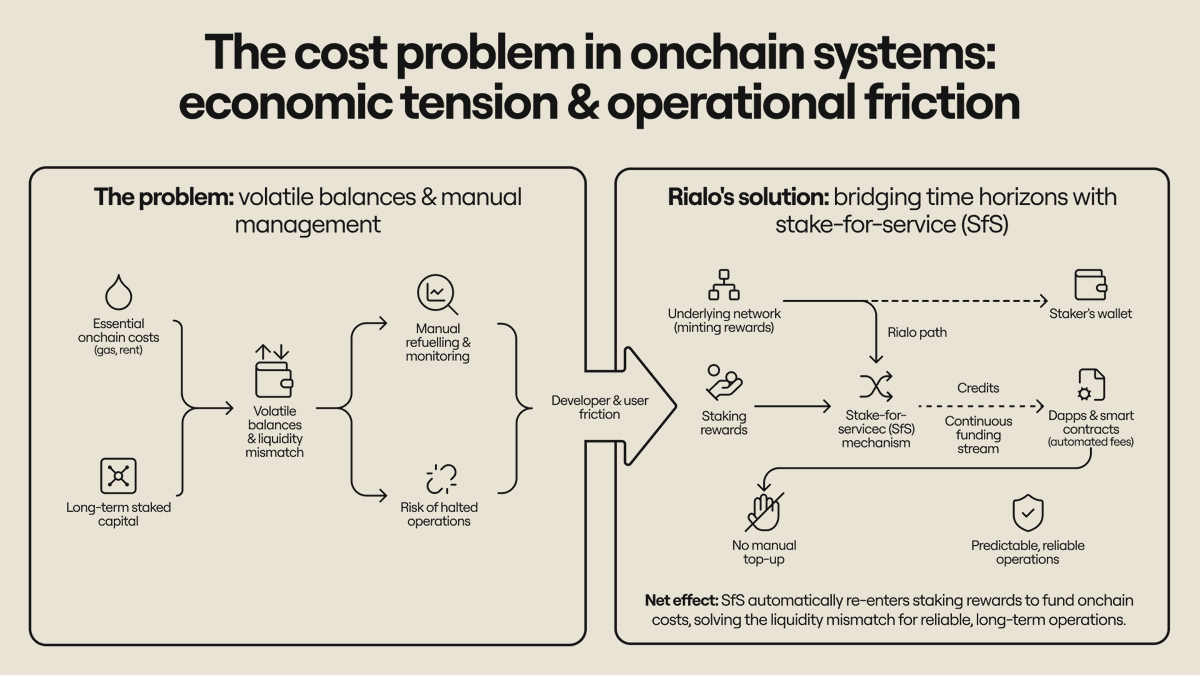

We need yield and always-on apps.

But today, they live in separate worlds: capital earns yield, while apps depend on manually funded hot wallets to run.

So, when wallets empty, apps stall, bots fail, and infra breaks.

Rialo closes the gap with Stake-for-Service. Here’s how 👇