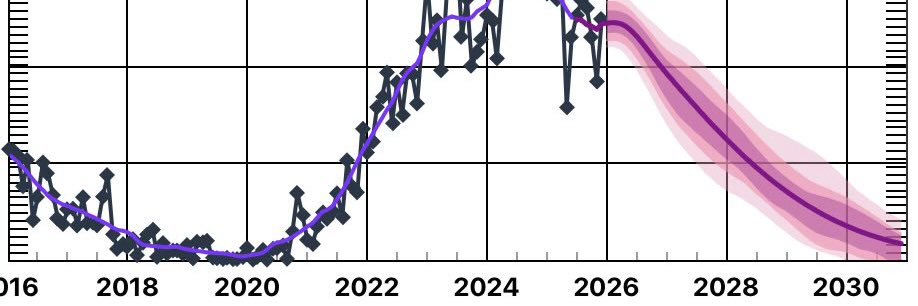

the US govt is from now until eoy 2028 in the business of explicitly buying and pumping stakes in ai / energy / defence /soon biotech ai (imo) companies with an infinite bid size and a moron that thinks number go up = he is loved. 10-13k

Donald Trump told reporters that his team might buy US stakes in artificial-intelligence companies and said he would host a meeting with AI executives as soon as next week https://t.co/PEEBpte0jN

frankly nobody does it better. everyone is shidding and farding about this being the end and I’m saying 10-13k by eoy 2028 as we get the final blowoff of the American empire

@Kurteth a big day! I will wait and see for the monthly close to see whether there’s a half hearted rally and fall or a big rise. Mike I believe thinks this is a local (not global) top, for now. I think we still need the true index blowoff. Maybe it’ll be bubble squared squared (bio x ai)

rare second post in a day: this is very true. seeing it everywhere. and tbf it’s also happening to me as well to some extent. but if it disappeared tomorrow I would recover imo. others? not so sure. not long before illusory competence leads to unforeseen consequences

the appearance of intelligence became easier to manufacture while the actual human capacity for intelligence became harder to grow. Everyone sounded more capable. Everyone became more dependent. Everyone had answers. Fewer people could still tell what an answer was.

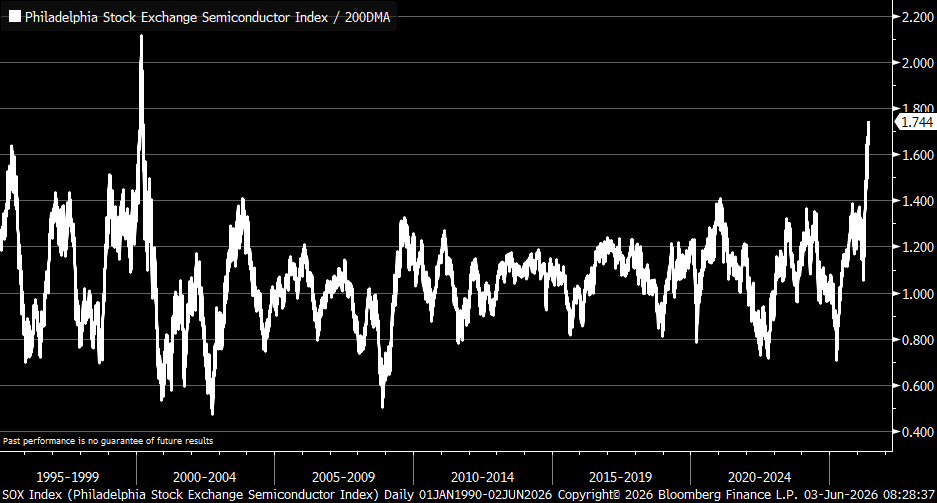

you may recall my “AI in boring shit” tweet. you also know I tend to avoid growth stuff. this time is different. it’s my opinion LLMs are now good enough to point at optimisation problems in a loop to reach a fixed goal.

the next frontier is ai-generated drugs

$ARKG $GENB $ABSI

as shale peaks and rolls over, and Hormuz is not opened for years (yes, you heard it here first, could be wrong) there are massive incentives for sovereign sponsorship of offshore drilling and LNG companies

few understand this

$VAL $TDW $GLNG

consider the dot com bubble and now consider that the same companies can spaff 80 billion up the wall while still making shed loads of money and they all want to be “the” AI company. quite likely we see a blowoff unlike anything ever see before. perhaps an S&P 10-13k (top signal)

MicroStrategy's position is deteriorating rapidly. In 4 months:

— USD reserves is down 60% to $900M

— Annual div obligations DOUBLED $835M → $1.65B

— Reserve coverage shrank 30 months → 7 months

— BTC sold: 32 BTC (first since 2022)

— STRC @ 11.5%, now trading below par at $97.11

Saylor is running out of cash and options

$MSTR still trades at 1.2mNAV which should provide some short-term relief, but with ~$137M in monthly div expense, it's gonna get uncomfortable

$MSTR - STRATEGY'S BITCOIN U-TURN:WSJ

For years, Michael Saylor urged investors to never sell bitcoin—famously saying, “Sell a kidney if you must, but keep the bitcoin.” Now, his company, Strategy, is preparing to sell part of its bitcoin holdings to remain solvent. The irony is hard to miss: Saylor still appears to have both kidneys.

thought about assets that would make me feel sick to buy them because they’re complete no hopers and dead in the water useless but have good valuation stats

came up with one and ashamed to say I’m buying $PYPL

incredible value over at $GSL , you won’t believe those valuation metrics tbh. buying this one for the long-term, this price or lower is amazing imo. shipping one of the greatest beneficiaries of tight supply, globalisation, and piracy. Few understand this

@NUKE_T0WN A dramatic swing from positive net income in Q4 2023 to a substantial net loss in Q4 2024, primarily driven by digital asset impairments.

• Operating expenses increased sharply, suggesting that actual results diverged significantly from prior performance trends.

Strategy Announces Fourth Quarter 2024 Financial Results; Holds 471,107 BTC $MSTR

Key Financial Metrics:

• Revenue: Q4 2024 total revenues were approximately $120.7 million, representing a 3.0% decrease year-over-year.

• GAAP EPS: Reported basic and diluted loss per share of $3.03, compared to a profit of $0.50 (diluted) in Q4 2023.

• Adjusted (Non‐GAAP) EPS: Non‐GAAP diluted loss per share of $3.20 versus a non‐GAAP diluted EPS of $0.56 in Q4 2023.

• Net Income: A GAAP net loss of $670.8 million in Q4 2024, a stark contrast to the net income of $89.1 million in Q4 2023.

• EBITDA: Not explicitly provided; however, note that the operating loss was driven significantly by digital asset impairment losses.

• Gross Margin: Gross profit of $86.5 million on $120.7 million of revenues resulted in a 71.7% gross margin, down from 77.3% in Q4 2023.

• Operating Margin: Loss from operations reached $1.016 billion in Q4 2024 versus $42.8 million in Q4 2023, driven largely by a $1.006 billion digital asset impairment charge.

• YoY / QoQ Changes:

• Revenues declined 3.0% YoY.

• Subscription services revenues increased by 48.4% YoY, while product licenses increased by 18.3% YoY.

• Product support and other services revenues declined by 10.8% and 20.8% YoY, respectively.

• Operating expenses soared 693.2% YoY, reflecting substantial digital asset impairment losses.

• Earnings Highlights:

• The company acquired 218,887 bitcoins during Q4 2024 for $20.5 billion, marking its largest quarterly increase in bitcoin holdings.

• Launched new performance metrics—“BTC Gain” and “BTC $ Gain” KPIs—with an annual BTC $ Gain target of $10 billion for 2025.

• Revised its annual BTC Yield target for 2025 to a minimum of 15% (down from 74.3% achieved in FY 2024).

• Completed a 10-for-1 stock split in August 2024, with all prior period data adjusted accordingly.

• Raised significant capital via at-the-market equity offerings, netting approximately $15.1 billion in Q4 2024 and an additional $2.4 billion between January 1 and February 2, 2025.

• Issued convertible notes and perpetual strike preferred stock to fund further strategic initiatives.

• Comparison to Estimates:

• The report does not explicitly provide analyst consensus or estimates; however, key figures indicate:

• A dramatic swing from positive net income in Q4 2023 to a substantial net loss in Q4 2024, primarily driven by digital asset impairments.

• Operating expenses increased sharply, suggesting that actual results diverged significantly from prior performance trends.

• Investors will likely compare these results to expectations on digital asset performance and capital strategy execution, though specific consensus numbers were not disclosed.

• Guidance:

• For 2025, the company is targeting an annual BTC Yield of more than 15% and an annual BTC $ Gain of $10 billion.

• The company anticipates transitioning to fair value accounting for its bitcoin holdings in Q1 2025, which is expected to enhance transparency in reporting the profitability of its treasury operations.

• Management’s commentary suggests continued momentum in executing its $42 billion capital plan, with $20 billion already completed, and a strategic focus on both bitcoin and AI.

• Business Segment Performance:

• Software Business:

• Reported total revenues of $120.7 million in Q4 2024.

• Subscription services revenues surged 48.4% YoY, and product licenses grew by 18.3% YoY, indicating strong recurring revenue components.

• However, product support and other services revenues declined 10.8% and 20.8% YoY, respectively.

• The Software Business itself posted a modest operating loss of $6.9 million, contrasting sharply with consolidated figures.

• Corporate & Other:

• This category, which includes costs related to the company’s bitcoin strategy (e.g., digital asset impairment losses), reported a loss from operations of over $1.009 billion.

• The combined consolidated performance was overwhelmingly impacted by these bitcoin-related charges, overshadowing the underlying software operations.

• Market Commentary:

• The market reaction is likely to be mixed as the impressive bitcoin acquisition activity and new KPI targets underscore a bullish long-term digital asset strategy.

• Conversely, the massive impairment losses and steep increase in operating expenses could raise short-term concerns regarding profitability and cash flow.

• The transition to fair value accounting for bitcoin holdings in Q1 2025 is expected to increase transparency but may also introduce additional volatility in future earnings reports.

• The company’s strategic focus on both bitcoin and AI innovation is positioned as a transformative approach, potentially enhancing its long-term market appeal.

• Additional Notable Items:

• Completed a 10-for-1 stock split in August 2024, significantly increasing the number of authorized shares.

• Issued $3.0 billion of 0% convertible senior notes due 2029 and 7.3 million shares of 8.00% Series A perpetual strike preferred stock to raise capital.

• Delivered a notice of redemption for the 2027 Convertible Notes, with provisions for conversion into class A common stock.

• Increased the authorized shares of class A common stock from 330 million to over 10 billion and similarly expanded authorized preferred stock.

• Adopted ASU 2023-08, which requires fair value accounting for bitcoin holdings, resulting in a cumulative-effect net increase to retained earnings of $12.745 billion.

• Traders’ Takeaway:

• While the underlying software business shows modest revenue performance and even slight operational profit, the consolidated results are heavily skewed by the bitcoin strategy—most notably, the steep digital asset impairment losses.

• Aggressive bitcoin acquisitions and the introduction of new KPIs signal a long-term bullish stance on digital assets, but traders should be cautious of the near-term volatility introduced by large, non-cash impairment charges.

• The upcoming adoption of fair value accounting for bitcoin could lead to further fluctuations in reported earnings, presenting both risks and opportunities.

• Capital raising via equity and convertible debt, along with the stock split, may improve liquidity and market accessibility, potentially creating trading opportunities based on future strategic developments.

@NUKE_T0WN They are in a locked feedback loop. The bomb has been planted. Agent Saylor has completed his mission. The Bitcoin reserve will be created - just not at the price holders want.