The Ultimate Silver Heist: Why Honey Badger #Silver is a Table-Pounding Buy Right Now $TUF.v

Mr. Eric Sprott just backed the truck up(now owns 10%)

Here’s why you should b paying attention to the most asymmetrical resource acquisition of the decade

#GOLD

https://t.co/SXpSkupdxP

🚨 $TUF.V / $HBEIF might be one of the most absurdly undervalued silver stories on the entire market right now… and the math is the part most people are missing. 🧠⚒️

Honey Badger acquired Prairie Creek through its purchase of Canadian Zinc.

This is NOT just another tiny exploration company poking holes in the ground hoping to find silver someday.

Prairie Creek is already a large, advanced mining project in Canada’s Northwest Territories with:

✅ huge historical silver-equivalent resources

✅ underground mine development already completed

✅ existing infrastructure and facilities

✅ a gravel airstrip

✅ engineering/economic studies already done

✅ important permits and approvals already in place

✅ exposure to silver, zinc, lead, and potentially germanium

That matters because most mining projects NEVER make it this far.

Mining is one of the hardest industries on Earth.

Most projects die long before becoming realistic mines because of:

⚠️ permitting problems

⚠️ infrastructure costs

⚠️ financing issues

⚠️ environmental hurdles

⚠️ inflation

⚠️ engineering failures

⚠️ metal price crashes

So Honey Badger may not have just bought metal in the ground.

It may have bought decades of work, development progress, and strategic positioning at an extremely low valuation.

And this is where the math starts getting ridiculous. 📊

Mining companies are often compared using:

➡️ EV/oz = Enterprise Value per ounce.

Very simply:

“How much is the market valuing each ounce of metal the company controls?”

Enterprise Value, or EV, is basically:

📌 company value

➖ cash

➕ debt

It is a rough way to estimate what the market thinks the actual mining assets are worth.

Honey Badger reportedly controls around:

⚡ ~550 million ounces silver-equivalent, or AgEq.

“Silver-equivalent” means all the metals in the deposit, silver, zinc, lead, etc., are converted into an estimated silver value so investors can compare projects more easily.

Right now, Honey Badger is reportedly trading around:

⚠️ ~C$0.05 EV per ounce.

That means the market is valuing each ounce at only FIVE CENTS.

Now compare that to a peer-average style valuation around:

📊 ~C$2.25/oz EV/AgEq

That is the key number.

Because:

📍 Current: C$0.05/oz

📍 Peer-style average: C$2.25/oz

C$2.25 ÷ C$0.05 = 45x.

That is where the “45x undervalued” argument comes from.

Not vibes.

Not hype.

Basic valuation math.

If Honey Badger’s ~550Moz AgEq were valued at today’s reported ~C$0.05/oz:

📊 550Moz × C$0.05 = ~C$27.5M EV

If those same ounces were valued at ~C$2.25/oz:

📊 550Moz × C$2.25 = ~C$1.24B EV

That is a difference of roughly:

🔥 ~45x enterprise value expansion.

And here’s the full valuation ladder:

📊 C$0.05/oz = ~C$27.5M EV

📊 C$0.25/oz = ~C$137.5M EV

📊 C$0.50/oz = ~C$275M EV

📊 C$1.00/oz = ~C$550M EV

📊 C$2.25/oz = ~C$1.24B EV

📊 C$5.00/oz = ~C$2.75B EV

So even a move from:

C$0.05/oz → C$0.25/oz

would imply roughly:

⚡ ~5x EV expansion.

A move to:

C$0.50/oz

would imply roughly:

⚡ ~10x EV expansion.

A move to:

C$1.00/oz

would imply roughly:

⚡ ~20x EV expansion.

A move to:

C$2.25/oz

would imply roughly:

🚨 ~45x EV expansion.

That does NOT mean the stock automatically deserves a 45x rerate today.

This is still junior mining.

And junior mining is brutally risky.

But it does mean the current valuation appears wildly compressed compared with the scale of the asset.

The market is essentially saying:

“Interesting project, but prove it actually matters economically.”

Fair enough.

Because risks ARE real:

⚠️ financing risk

⚠️ construction costs

⚠️ dilution risk

⚠️ remote logistics

⚠️ metallurgy/recovery risk

⚠️ delays

⚠️ commodity volatility

⚠️ historical resource validation

⚠️ germanium recoverability

But the bullish argument is that the market may currently be valuing Prairie Creek almost like stranded geology…

while the world is increasingly desperate for secure metal supply chains.

And here’s the deeper macro story most people miss:

Silver is NOT just a “precious metal.”

Silver is the most electrically conductive metal on Earth. ⚡

Modern civilization quietly depends on silver for:

🔋 solar panels

🚗 electric vehicles

🖥️ AI datacenters

📡 telecom systems

🏥 medical equipment

⚙️ industrial electronics

🛰️ military technology

🔌 power grids

And here’s the really important part:

Most silver is NOT mined primarily for silver.

It is usually produced as a byproduct of:

➡️ zinc mines

➡️ lead mines

➡️ copper mines

That means silver supply cannot easily increase even if demand surges.

Why?

Because silver production depends heavily on whether OTHER metals are profitable to mine.

That creates what’s called:

⚡ structural supply constraints.

Meaning:

the system physically struggles to grow supply fast enough.

So the world is rapidly electrifying itself while relying on a metal whose production is partly controlled by unrelated mining economics.

That’s a huge hidden bottleneck. 🧠⚡

Now add Prairie Creek into that situation.

Prairie Creek is polymetallic, meaning it contains multiple metals:

🥈 silver

⚙️ zinc

🧱 lead

🛰️ potentially germanium

That matters because the zinc and lead can potentially help offset mining costs.

So this is not just “silver exposure.”

It’s silver exposure supported by other valuable metals.

Now let’s talk about the germanium angle because this may become extremely important.

Honey Badger recently highlighted assays reportedly up to:

⚡ 316 ppm germanium.

An “assay” is basically a lab test showing how much metal exists inside the rock.

Germanium is a strategic metal used in:

📡 fiber optics

🌌 infrared optics

🖥️ semiconductors

🛰️ aerospace and military systems

This is where the story potentially changes categories.

Silver investors may notice the silver.

Critical-mineral investors may notice the germanium.

Defense and semiconductor investors may notice the secure Western supply-chain exposure.

That means Prairie Creek could eventually attract multiple DIFFERENT types of investors simultaneously.

That matters a lot.

Because valuation depends partly on WHO is paying attention.

Old market label:

🪦 “small silver explorer”

Possible future label:

⚡ “strategic Canadian silver-critical-minerals platform”

Those are completely different categories.

And category changes are where mining stocks can rerate violently.

Now add another important layer:

🛣️ Infrastructure and permitting scarcity.

In modern mining, geology is often NOT the hardest part anymore.

The hardest part is usually:

⚠️ permits

⚠️ roads

⚠️ infrastructure

⚠️ environmental approvals

⚠️ financing

⚠️ social license

⚠️ Indigenous agreements

A giant metal deposit without infrastructure or permits can sit trapped for decades.

That’s why Prairie Creek’s historical development work matters so much.

Honey Badger may have bought:

➡️ time

➡️ infrastructure

➡️ permitting progress

➡️ engineering progress

…at a valuation the market still barely respects.

Now ask the replacement-cost question:

What would it cost today to recreate Prairie Creek from scratch?

Not just discover it.

But:

📌 drill it

📌 engineer it

📌 permit it

📌 develop underground workings

📌 build infrastructure

📌 negotiate agreements

📌 survive years of inflation

📌 secure financing

Probably vastly more than Honey Badger paid.

That’s another reason the valuation disconnect looks extreme.

And there’s another macro layer.

Mining has been massively underinvested in for years.

Investors got burned during previous cycles from:

📉 dilution

📉 bad management

📉 cost overruns

📉 failed projects

So capital left the sector.

Projects stalled.

New discoveries slowed down.

Now suddenly governments want:

⚡ electrification

🖥️ AI infrastructure

🛡️ defense reshoring

📡 semiconductor independence

🔋 critical minerals

But mining projects take YEARS or DECADES to build.

You cannot magically create advanced Western mining projects overnight.

That scarcity may eventually matter a lot more than markets currently realize.

Especially in a fractured geopolitical world where:

🌎 secure Western supply chains

may become more valuable than simply “cheap ounces.”

And this creates another bullish possibility:

🏛️ Government support.

Western governments are increasingly offering:

✅ critical-mineral funding

✅ grants

✅ tax incentives

✅ infrastructure support

✅ strategic investment programs

A Canadian silver-zinc-lead-germanium project may increasingly fit into that strategic narrative.

Then there’s the reflexive effect.

At tiny valuations, relatively small inflows of money can move mining stocks dramatically:

📈 rising price

→ attracts attention

→ attracts traders

→ attracts institutions

→ improves financing access

→ improves survival odds

→ attracts even more attention

That’s how junior mining stocks often move.

Slowly at first…

then suddenly all at once. ⚡

So the thesis is NOT:

“cheap stock guaranteed moon.”

That’s simplistic thinking.

The thesis is:

🧠 The market may currently be using OLD assumptions to value Prairie Creek.

The market may still see:

🪦 “remote silver explorer”

…while the world increasingly values:

⚡ secure conductive metals

🛰️ strategic minerals

🛡️ Western supply chains

📡 semiconductor inputs

🔋 electrification infrastructure

If Honey Badger can validate resources, advance engineering, improve financing visibility, confirm germanium economics/recovery, and attract institutional or strategic attention…

then the market may eventually stop valuing Prairie Creek like forgotten geology…

and start valuing it like strategically important mineral infrastructure.

At ~C$0.05/oz EV/AgEq, the market is essentially saying:

“Prove these ounces matter.”

Fair enough.

But the reason the setup is so explosive is simple:

If the market ever values those ounces closer to a peer-style ~C$2.25/oz…

the math says the EV gap is roughly 45x.

That is not a small discount.

That is a valuation canyon.

And if Prairie Creek proves financeable and strategically important in a world increasingly desperate for secure conductive and critical metals…

today’s valuation may eventually look less like caution…

and more like the market accidentally throwing away a winning lottery ticket during a metal shortage. 📈🔥

🚨In the past 30 years, I've NEVER seen a better risk/reward stock as $TUF.v

This is an 8-10 bagger if everything goes horribly wrong!

*Don't take my word for it, just DYOR on this one!🧐

The 3 Godfathers are all holders(DD, Eric & Rule

$TUV $AG #Silver#GOLD#TSX#TSXV#Silver

Honey Badger acquired the Prairie Creek mine. After the deal, my target price is $15. Seems crazy, but that's what I get at $200 silver.

With that much upside potential, you also get very high risk. This is not an easy project. Only invest what you can afford to lose. That's how I invest. Don't let a single stock hurt your portfolio. 😉

https://t.co/e4IRXvWg6Z

@CP24 So now every cop in #Canada will simply let car thieves drive off? Why risk job/pension?

Just like that cop last year who told everyone to leave your keys in the mail box for thieves!

What has happened to this country?! @onpoli

If you're a smart #Uranium investor you want to listen to the U GOATs

$DMX 's CEO found Arrow &

Doug.B built MacArthur River!

🧐DYOR on $DMX.v 📈 It's 5-10 bags!

#Uranium $CCJ $DML.to $URA #GOLD $ISO.to $UUUU $URC.to $SASK $EFR.to #TSX#TSXV $GLO.to #StocksToBuy#MiningStocks

💥So...

DOUG BEATTIE

-Ex CHIEF mining engineer at Cameco & $NXE.to , who built MacArthur River with his bare hands says.

@District_metals is what #Uranium investors need to own!📈 2B+ MC soon

$DMX

$CCJ $DML.to $URA #GOLD $ISO.to $UUUU $URC.to $SASK #TSX#TSXV $GLO.to #Silver

🤔I get it. High-grd Athabasca #Uranium is the only way to go..

But shouldn't the amount & cost/ease to get that U out be more important?

This is where $DMX blows everyone away.

Please spend 10 mins of DYOR

$DMX.v

$CCJ $NXE.to $DML.to $URA #GOLD $ISO.to $URC.to $SASK #TSX#TSXV

@district_metals showed this table in the linked presentation to Chinese investors. The uranium mining ban will be voted in the next 45 days:

https://t.co/VyBFqwC6dP

Then you have a x2-x30 times undervalued asset... and that's only counting U.

#DMX.V

https://t.co/nz72G168YK

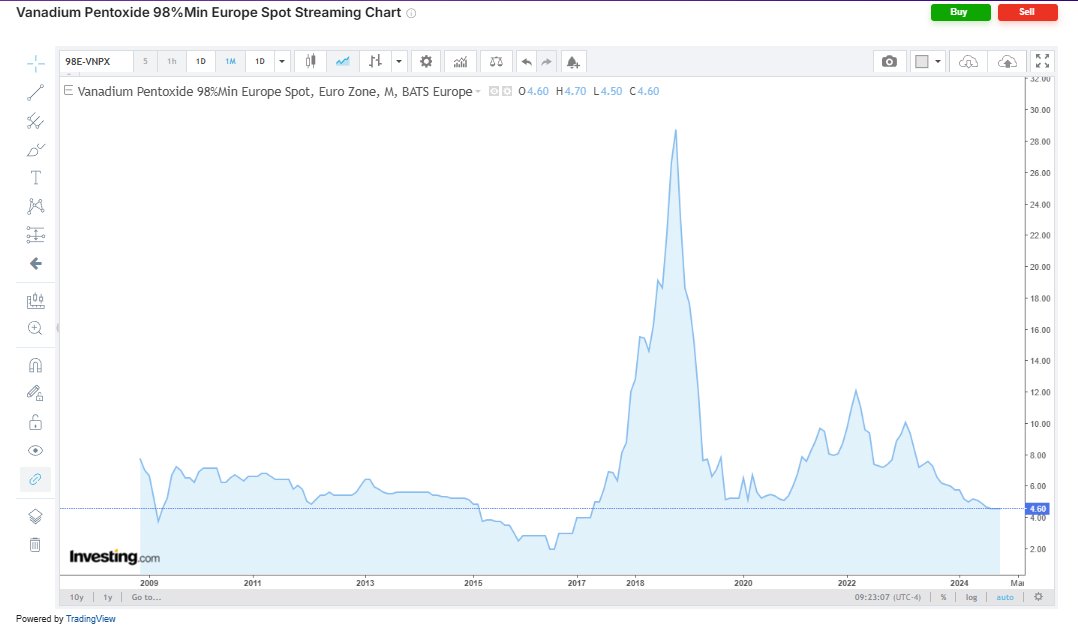

Vanadium is the next commodity to squeeze

• 80% of global supply comes from Russia and China

• The U.S. produces almost nothing domestically

• Demand is exploding - for clean energy and national defense

@Swedish_uranium@district_metals If you DYOR on DM, and you are in Sweden, you know that DMX isn't trying to build a mine. They are just proving the resource. If you're 100% sure it won't happen, then all you need to do is simply not invest. You don't know it won't happen either. Maybe change your handle too?

💥So...

DOUG BEATTIE

-Ex CHIEF mining engineer at Cameco & $NXE.to , who built MacArthur River with his bare hands says.

@District_metals is what #Uranium investors need to own!📈 2B+ MC soon

$DMX

$CCJ $DML.to $URA #GOLD $ISO.to $UUUU $URC.to $SASK #TSX#TSXV $GLO.to #Silver

@FreiburgCoffeeC You somehow forgot to mention @District_metals

DMX

The largest undevolped Uranuim resource in the world that's likely 3 times bigger. All in Sweden, which is easy to mine and sell to E.U.

24 posts but you don't mention DMX?

where do you think they are going to get the U from?

#uranium I am getting more optimistic on uranium as timelines of new production get pushed out, amounts of new production expectations are unrealistic, the tired old mines of Cameco are aging out and hopefully that pool of uranium inventory on the sidelines is getting smaller. My main uranium holding has been District Uranium the past few years and Garrett has done a great job moving one of the World's largest undeveloped uranium resources forward in Sweden. @district_metals

@BrianHafer3@RealRickRule@district_metals You don't even have the right exchange. It's an explorer, it's not supposed to have revenue. FFS, lol. Do some bloody research. Best to start collecting stamps.