$DGXX

OpenAI’s Texas Data Center Ambitions and the Case for a Digi Power X Partnership

With OpenAI’s Stargate initiative already advancing in Abilene the question arises: Could DGXX (and its US Data Centers affiliate) play a meaningful role?

The Core Opportunity

OpenAI faces one of the industry’s biggest constraints in Texas: reliable, fast-to-deploy power. Grid interconnection delays have already forced adjustments at major sites. Texas, however, offers a structural advantage through its abundant Permian natural gas, extensive pipelines, and ERCOT rules that support behind-the-meter (BTM) generation via Private Use Networks.

Most Plausible Scenarios

Here’s how involvement could realistically unfold:

1. DGXX Power Supply (Highest Probability) DGXX develops and owns a dedicated natural gas power plant adjacent to OpenAI’s Texas campus. OpenAI would purchase the power under a long-term Power Purchase Agreement (PPA). DGXX would handle development, permitting, fuel supply contracts (from third-party Permian producers), and operations. Why it fits: Power is the bottleneck. DGXX already has power generation experience and has pursued large AI-focused power deals. Texas BTM gas projects are scaling rapidly for exactly this reason.

2. USDC / DGXX Modular Data Center Capacity (Medium Probability) DGXX’s US Data Centers arm (or the parent) provides supplemental high-density modular halls or colocation space on or near the main campus. This could support overflow workloads or faster incremental capacity. Why it’s plausible but secondary: DGXX has proven this model with deals like the 40 MW Cerebras campus. However, OpenAI’s flagship Texas sites are primarily developed by much larger partners.

3. Integrated DGXX + USDC Package (Medium-High Probability) A combined offering where DGXX supplies both dedicated power and modular compute infrastructure. This vertical approach reduces coordination friction and leverages DGXX’s full-stack capabilities. Why attractive: Speed and simplicity in a market that rewards rapid deployment.

Cost and Execution Realities

Developing a dedicated BTM gas plant is capital-intensive. Industry estimates for 2026 place costs in the $1.0M–$2.5M+ per MW range (higher for efficient combined-cycle, lower for faster simple-cycle setups). A 100 MW plant could total roughly $100M–$220M all-in, including balance-of-plant, substations, and development.

DGXX would not fund this entirely from its balance sheet. Long-term PPAs with creditworthy off-takers like OpenAI make these projects highly financeable through debt and equity partners. DGXX’s existing power expertise gives it a meaningful edge in execution.

DGXX offers a nimble, Texas-capable player with rare vertical integration of power and modular data centers. For supplemental power or fast-add capacity, this is a natural fit. A full flagship replacement is less likely given scale differences, but meaningful participation in power and modular expansion is realistic.

Peter Lynch taught us to look for asymmetric value in real, asset-heavy businesses.

$DGXX is textbook Lynch meets frontier AI:

• Real owned land & 400MW secured power

• $150M cash / $0 long-term debt

• $1.1B locked Cerebras contract

An unfair risk-to-reward ratio.

$nvda #AI

This is a consolidation of my thoughts on $dgxx/$usdc/Yutanix/Zutacore.

There is alpha in this. Enjoy the read:

Nobody is talking about the real reason $DGXX is about to take over the AI infrastructure market. Let me explain.

Everything $dgxx is doing right now is positioning them to completely take over the ai infrastructure market.

$DGXX owns 55% of US Data Centers Inc. (USDC). USDC is currently private. USDC's entire business is manufacturing and selling the ARMS 200 — a modular, Tier 3-certified AI data center system that can turn any powered site into a fully operational AI compute facility in a fraction of the time traditional construction takes.

Companies like $IREN have spent years and enormous capital securing gigawatts of powered land. That's the hard part, or so everyone thought. But raw power means nothing if your cooling and compute density can't keep up with modern AI workloads. Air cooling and glycol loops are hitting their limits fast. These companies are sitting on some of the most valuable land in infrastructure and underutilizing it because they chose the wrong stack.

USDC's ARMS 200 is the answer they didn't build themselves. Drop modular units onto existing powered land, skip years of conventional construction, and immediately unlock high-density AI compute. The host site doesn't have to rebuild from scratch. They just have to let USDC in. Their stranded gigawatts become productive. USDC gets a customer. Everyone wins, but USDC wins most, because they own the system that makes it all work.

The ones who dont make this switch either through USDC or on their own will be left with way bigger electic bills, higher maintenance costs, and difficulty expanding.

The ARMS 200 uses a dielectric liquid cooling (I will talk further about the liquid a couple paragraphs down, this is signalled and not publicly confirmed. This is alpha.) built around Supermicro hardware and NVIDIA Blackwell-class GPUs, not to mention the $35 million $dgxx just spent on Vera Rubins. Wonder where thats going!

Each pod delivers 1 MW of compute and supports up to 256 B200/B300 GPUs. DGXX plans to scale to 40 MW at its Alabama site alone, roughly 10,240 GPUs. The modularity allows for easy scaling.

Now here's where Yutanix fits. Yutanix is an AI infrastructure marketplace that connects AI teams with GPU capacity, deployment planning, and data center sourcing. As USDC starts selling ARMS units to powered sites at scale, Yutanix is positioned to be the demand-side engine that feeds it, matching teams who need compute with the exact kind of rapid-deployment, cluster-ready infrastructure ARMS provides. USDC supplies the modules. Yutanix supplies the customers. That's a clean loop.

Now here's the piece worth watching VERY closely. ZutaCore dielectric HyperCool technology is waterless, direct-to-chip dielectric cooling.

Zero water, handles extreme power densities that glycol and air cooling can't touch, closed loop, ZERO leak risk

The main publicity backlash against AI data centers right now is noise, power, and water usage. Communities where USDC decides to set up modules will eat this up.

ZERO water usage if utilizing Zutacore Hypercool.

The heat can be REUSED for other purposes easily.

The Zutacore system requires a flow rate of just 0.3L/min for every 1000W. For example, cooling Nvidia’s B200 (1200W) would need a flow rate of 0.36L/min with HyperCool, compared to 1.8L/min for single-phase direct-to-chip water/glycol cooling.

Thats 5 to 6x lower flow rate. 50%+ less energy usage on cooling.

No official DGXX/ZutaCore partnership has been announced, but Jagan Jeyapal, CTO of DigiPowerX, was photographed at ZutaCore's booth at GTC and tagged #digipowerx #dgxx #zutacore and #yutanix all in the same LinkedIn post, mentioning plans to work on "large projects together." That's not nothing.

If a formal partnership follows, it becomes very hard for any competitor to replicate without tearing their building apart and starting over.

This is what I come up with on valuations for $dgxx from the help of Chat-

2027

Management target:

90 MW colocation

10-12 MW GPU

~$300M revenue run rate

Market Cap Range

Bear: $800M

Base: $1.5B

Bull: $2.5B

At ~90-100M diluted shares:

Bear: ~$8-9/share

Base: ~$15-17/share

Bull: ~$25/share

2028

Management target:

140 MW colocation

30+ MW GPU

~$450-500M revenue run rate

Market Cap Range

Bear: $1.5B

Base: $3.0B

Bull: $5.0B

Share price:

Bear: ~$15

Base: ~$30

Bull: ~$50

I strongly believe that investing in fundamentally solid, undervalued micro-caps will outperform the market over the long term.

I’ve successfully proven this strategy by investing early in $NBIS, $CPSH, and $ONDS before they gained mainstream popularity.

Currently, I am long on three heavily undervalued companies:

$DGXX : $540M market cap. Trading at a huge discount compared to its peers; projected to hit $300M ARR next year.

$AMPG : $200M market cap. An Open RAN pioneer guiding $50M for FY26 with 48% margins. Boasts a powerhouse customer list ($NVDA, $IBM, $AMZN) spanning ORAN, Quantum, 5G/6G, and SATCOM.

$SCW.WA : $160M market cap. Scanway is a A Polish NewSpace frontier company specializing in high-resolution Earth-observation telescopes, satellite optical instruments, and industrial machine vision for high-speed manufacturing/QC. Just announced two new contracts yesterday.

This is not financial advice. Please do your research and due dilligence and NEVER blindly follow anyone into investnent.

There are moments when a company emerges from becoming something into undeniably being something. DigiPowerX has emerged. I serve as a Director of $DGXX and these are my personal views, not the Company's. Everything here comes from public filings and press releases. This is not investment advice. What follows is my perspective as a Board Member, grounded entirely in publicly disclosed information.

I've been in the rooms. I've sat across from Michel Amar in strategy sessions, attended investor meetings, reviewed the financial models, and watched this executive team: Alec, Jag, Paul, and others, supported by expert legal counsel and senior leaders of the world's largest financial institutions, make decisions under real pressure with real capital on the line. What I'm about to share is my personal view, grounded in publicly disclosed information, because I think the magnitude of what is being built here deserves to be said clearly.

THE FUTURE OF AI IS PHYSICAL

Many talk about AI as if it lives in the cloud. It doesn't. It lives in buildings. Buildings that require hundreds of megawatts of power, purpose-built cooling systems, owned land, Tier III infrastructure, and teams who know how to operate it at scale without blinking.

We are at the beginning of what will be the largest infrastructure buildout in human history. Not the largest tech buildout. The largest infrastructure buildout - period. The demand for AI compute is doubling and doubling again. The models are getting larger. The inference requirements are exploding. OpenAI, Google, Meta, Amazon, and every major enterprise on earth is racing to deploy AI at scale and every single one of them needs power and physical compute infrastructure to do it.

The companies that secured that infrastructure early, before the utilities ran out of capacity, before the land was gone, before the power agreements became impossible to sign - are sitting on assets that cannot be replicated at any price today.

DigiPowerX is one of those companies.

THE PICTURE I'M POSTING

That photo is a Cerebras data center, 10 MW of operational AI compute. Take a look at it. Quiet on the outside. Inside: wafer-scale AI chips, liquid cooling running nonstop, redundant power, and some of the most powerful AI inference hardware ever deployed.

This is what the physical layer of the AI revolution looks like.

DigiPowerX is building four times this, 40 MW. On land we own in Columbiana, Alabama. Powered by a substation we built. Backed by 393 MW of secured power across our portfolio. And anchored by a $1.1 billion, 10-year Master Services Agreement with Cerebras, the company that operates that exact facility in the photo.

Phase 1 - 15 MW - comes online December 15, 2026.

Full 40 MW delivered by Q1 2027.

Substation: complete. Grid interconnection: finalized. All long-lead equipment: secured.

MICHEL AMAR AND WHAT I'VE SEEN FROM THE INSIDE

I've reviewed the financial models. I've been in the investor meetings. I've walked, almost running to keep up, with Michel through back-to-back meetings, building to building across midtown Manhattan. It actually was a very productive and exciting day. I've watched Michel Amar operate, and I want to say publicly what I believe privately: he and Alec saw this coming before many in this space did. We have meetings 24/7, including Saturday's and Sunday's. Many mornings I wake up and there is already a new text or email from Michel on something to be discussed after I grab a large cup of coffee.

They made the call to walk away from Bitcoin mining before it was obvious. They secured the power before it became scarce. We signed Cerebras - one of the most consequential AI compute companies in the world - before breaking ground on the data center. They built NeoCloudz and launched GPU-as-a-Service while the flagship campus was still under construction. And he did all of this with a balance sheet that today carries approximately $150 million in cash and zero long-term debt.

That is not luck. That is vision, executed with discipline.

Cerebras, for context, just completed the largest IPO of 2026 on Nasdaq (CBRS) - opening 68% above offering price, raising $5.55 billion, holding a $20B+ relationship with OpenAI. They looked at every option available to them and chose DigiPowerX to be included. A billion-dollar bet on our team and the assets we've assembled.

I've seen the plan from the inside. What's being communicated publicly reflects exactly what I've seen in execution. There is no gap.

WHERE THIS IS GOING

The AI data center of the future isn't a retrofitted warehouse. It's purpose-built from the ground up - for liquid-cooled, 150kW+ rack density, Tier III uptime, and the kind of power reliability that frontier AI demands. It sits on owned land, connected to grid power that was secured years ago, and operated by people who've never run anything less.

That is exactly what DigiPowerX is building.

And we're not stopping at 40 MW. The pipeline includes a 1.3 GW Letter of Intent in West Virginia - targeted for 2028 through 2030. As AI scales from tens of megawatts to gigawatts, DigiPowerX is already positioned for that next phase.

NeoCloudz, our GPU-as-a-Service platform, is live right now on NVIDIA B200 and B300 bare metal - the fastest, most powerful AI compute available today. First revenues recognized in May 2026. And we've already committed $35 million to NVIDIA's Vera Rubin platform - the successor to Blackwell - for Q1 2027 deployment. We try to be one generation ahead.

Project financing is advancing with one of the world's largest private credit institutions - managing $220B+ in credit assets - structured as non-dilutive 70/30 debt. Firms at this level don't commit to a process without exhaustive underwriting. The fact that this financing is moving forward is itself a validation: of the asset quality, the contracted cash flows, and the professionalism of the DigiPowerX team in every aspect of how this company conducts its business affairs.

THE NUMBERS - PUBLICLY STATED MANAGEMENT TARGETS

2026 → First AI revenues. NeoCloudz live. SubQ AI 24-month bare metal contract (~$19.6M). Revenue engine started.

2027 → ~$300M revenue run rate. Full 40 MW Cerebras campus online. NeoCloudz scaling.

2028 → $450��$500M run rate.

2029 → $800M–$1B run rate.

These are Michel's publicly stated targets. Subject to all the risks in our public filings. But they are grounded in assets that already exist, contracts that are already signed, and a team that is already executing.

I'm proud to serve on this board. I'm proud of Michel Amar, Alec Amar, Paul Ciullo, Jagan Jeyapaul, and every person building this platform. And I'm proud of what this company represents for the future of AI infrastructure in America.

The AI revolution needs a physical layer. DigiPowerX is building it.

That photo shows 10 MW.

- We're delivering 40 MW.

- And we're just getting started.

Full press release (June 3, 2026): https://t.co/toDvZBsnDa

Gerard Rotonda | Director, DigiPowerX Inc.

$DGXX $DGX

#DigiPowerX #AIInfrastructure #DataCenter #GPUaaS #NeoCloudz #NVIDIA #Cerebras #AICompute #FutureOfAI #PowerInfrastructure #NasdaqStocks

For fiscal 2027, Digi Power X expects total revenue of $250M–$300M.

If that revenue guidance holds and you spread it evenly across quarters, Q1 2027 alone would be roughly $60–75M — a massive jump from the $6.8M they did in Q1 2026.

Q1 earnings call will be the next major step

The market is sleeping on $DGXX and the numbers prove it. 🧵

---

Forward P/S ratios across NeoCloud providers:

$CIFR - 22.32x

$NBIS - 10.82x

$IREN - 8.44x

$WYFI - 6.78x

$CRWV - 3.73x

$DGXX - 2.89x ← cheapest in the group

The median is 7-8x. $DGXX is trading at less than half that.

---

Let that sink in.

$DGXX is cheaper than $CRWV on a forward P/S basis.

CoreWeave, the AI hyperscaler with Meta, OpenAI, and Anthropic as customers, trades at a HIGHER multiple than Digi Power X.

The market is pricing $DGXX as if they simply cannot execute on FY2027 guidance.

---

So what IS the FY2027 guidance?

→ $250 to 300M in total revenue

→ 90MW AI colocation + 10-12MW GPU-as-a-Service

→ Anchored by a signed $1.1B, 10-year MSA with Cerebras (expandable to $2.5B)

→ Phase 1 (15MW) RFS: December 2026

→ Full 40MW: Q1 2027

The contract is signed. The term sheet for debt financing is signed. The GPUs are in the ground.

---

The re-rate math is simple.

At the peer group median (~7.5x fwd P/S) on $275M 2027E revenue:

→ Implied market cap: ~$2.1B

→ vs. today's $722M

→ That's a ~3x from current levels

At IREN's multiple (8.44x):

→ Implied market cap: ~$2.3B

→ ~3.2x upside

At CRWV's multiple (3.73x), the LOWEST reasonable re-rate:

→ Implied market cap: ~$1.0B

→ Still ~40% upside just to match the proven hyperscaler

---

Why is it this cheap?

Execution risk. The gap between today's ~$27M annualized revenue and $275M in 18 months is enormous. The market wants proof before it pays up.

That proof arrives December 2026.

Phase 1 RFS is the line in the sand. If they hit it, this re-rates hard.

---

Balance sheet to back it up:

→ ~$125M cash, zero long-term debt

→ $45M YTD capex already deployed at Columbiana

→ 210MW grid-connected today — no interconnection wait

→ 393MW total secured. 1.3GW WV LOI for 2028-2030

$DGXX is the cheapest NeoCloud name in the peer group. December 2026 is the catalyst.

$DGXX is executing its pivot to AI data centers hard.

Any single one of below catalysts happening = massive re-rating for $DGXX

1. Full revenue ramp from the $19.6M 24-month SubQ AI bare-metal GPU deal (already live May 15 via NeoCloudz)

2. Execution on the $1.1B 10-year $CBRS 40 MW AI colocation campus in Columbiana, AL and/or expansion to $2.5 billion

3. Deployment & scaling of ARMS 200 Tier III modular pods (first units already in motion, targeting 50 MW AI IT load online in 2026)

4. Landing additional multi-year AI colocation + GPU-as-a-Service contracts (multiple advanced discussions already underway)

5. Hitting the revenue inflection that sets up $250–300M guidance for 2027 (AI colocation + GPU cloud + energy sales)

6. Securing non-dilutive debt financing to accelerate capex while keeping ~$125M cash + $15M digital assets war chest intact

7. Further NeoCloudz GPU cloud expansion with more NVIDIA Blackwell workloads and enterprise wins

8. Strategic clean-energy tie-ups unlocking cheaper power & ESG premium

Balance sheet is rock-solid (zero long-term debt, positive Adj. EBITDA already in Q1), legacy mining is winding down cleanly, and the modular AI factory is live.

Which one do you think hits first? Drop it below 👇

$DGXX 🚨🚨🚨

Huge if true!!!!!

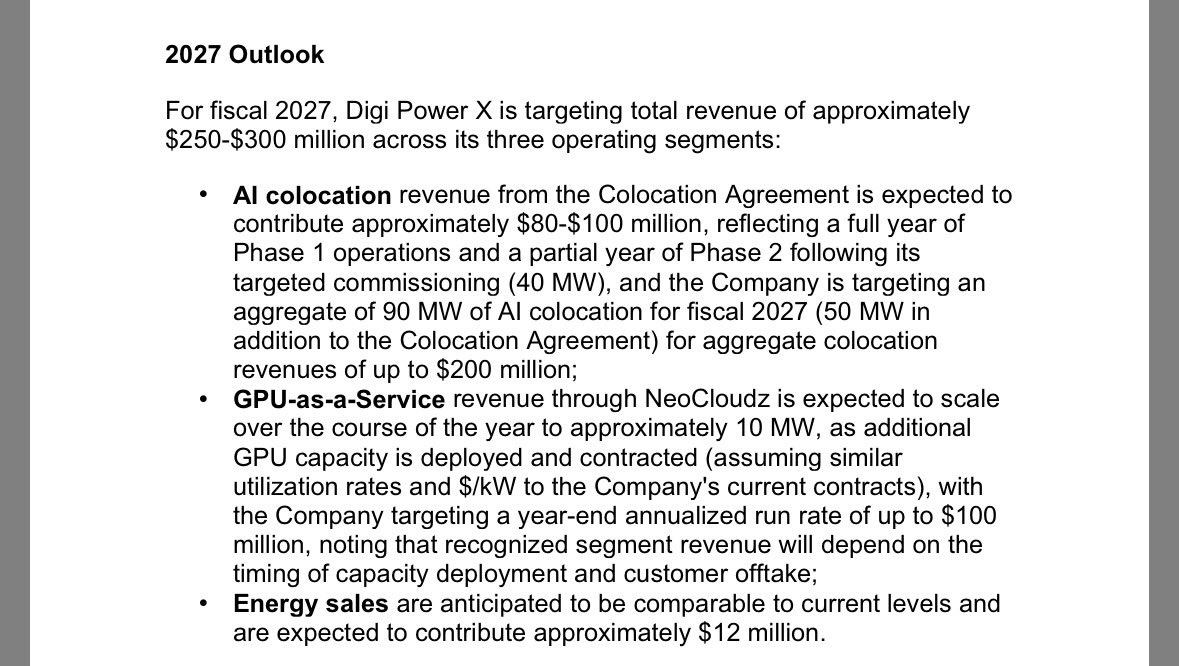

𝐅𝐘 𝟐𝟎𝟐𝟕 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $250 - $300 million

Accelerating exponentially. This represents a monumental leap from the $6.8M generated in Q1 2026. The guidance assumes seamless execution of 90 MW in colocation and massive GPU-aaS uptake.

$DGXX just dropped its 2027 outlook and the market is still sleeping on it.

Management is guiding $250–$300M in total 2027 revenue across three segments. Note that this is not the ARR - which should be a much higher number.

• AI colocation (Cerebras + Phase 2): up to $200M

• GPUaaS via NeoCloudz: $100M ARR run-rate by year-end

• Energy: ~$12M

I am applying 10x forward P/S - the discount rate I would give a micro-cap with execution risk and a single anchor tenant (at the moment).

I’m using the mid revenue number of $275 million. At 10x multiple, the current fair value should relate to a market cap of $2.75 billion.

Assuming diluted number of shares of 90 million, my end of 2026 target price is $30, very close to my initial estimate of $32.

The bull case of course is higher than the above. Any new deals will rerate my price higher.

Thesis is intact. Wake me up in September. :)

Not an advice. Do your own DD. $DGXX $CBRS