#btc is the ONLY way

Stay away from defi

Promised quick riches will only leave you rekt by the very people influencing you to buy shitcoins

Just because your Twitter feed shows you a handful of influencers who have gotten rich, doesn’t make it legit

MANY more are left rekt

@RetirementRight Dude they’ll drain your bank account long before they drain my #bitcoin wallet

If you have any money left with your track r rod with $iren and now #btc

Hey will you inverse Cramer my newest $GNS bags?

#bitcoin treasury company

@CK_Cryptoklepto@DanCote303 That’s the dumbest thing I’ve ever heard

Yes, we need miners to exist to secure the network

No, it’s not a liability for saylor to not have a capital intensive business that operates at the margins to “secure his bitcoin”

But you need to mix narratives to feel somewhat correct

Overvalued

mNAV higher than $MSTR

And they’ve just recently added all that value per share

Until 6 months ago they didn’t have half the bitcoin they have now

It’s not about price per share, it’s about market cap

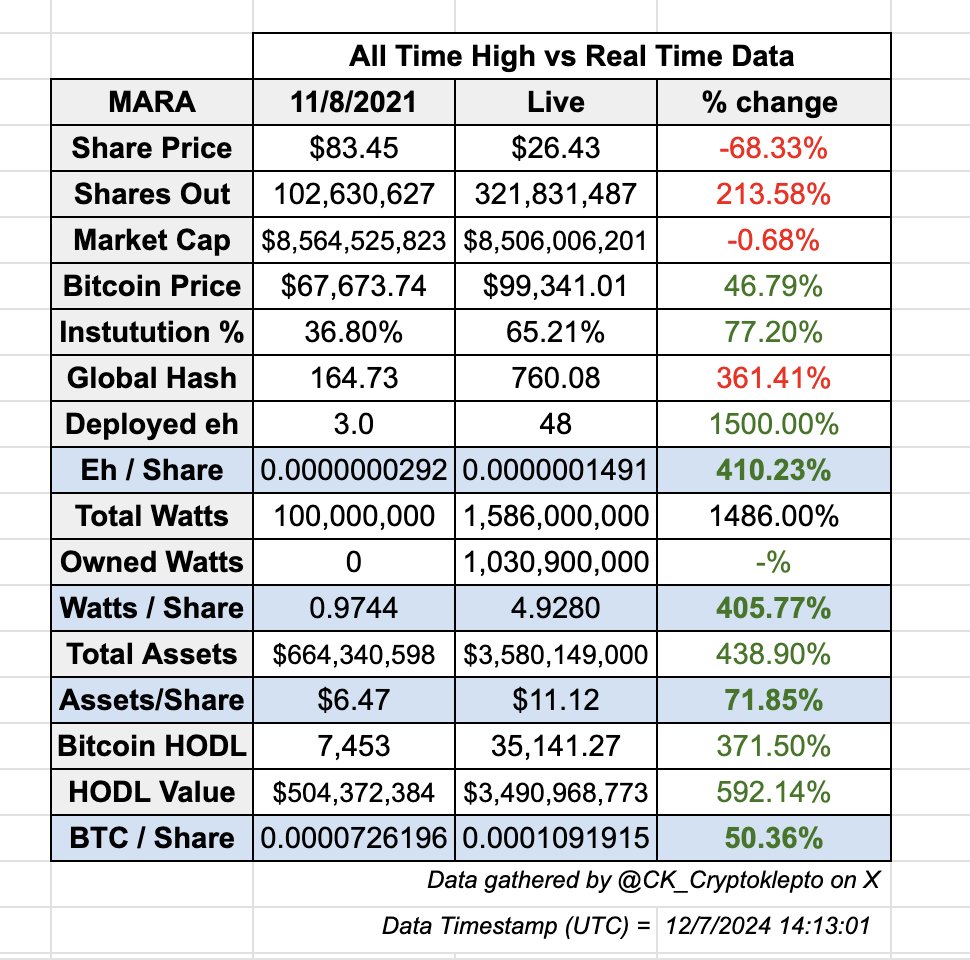

$MARA has grown Assets on the Balance Sheet by orders of magnitude greater than Share Count over the last 3 years yet the Market Cap is still lower and Share Price is 68.33% below that previous high water mark

Note: this data does NOT include what will likely be an announcement of another 6K or more Bitcoin purchased this past week via 0% interest convertible notes so the orders of magnitude related to Bitcoin Per Share will be even more parabolic once that is added

What does this #MARA data mean to you?

$BTC #BTC #Bitcoin $MSTR #MSTR #MARAPIG

@onewordtrader @CK_Cryptoklepto That’s way oversimplified, and then you leave out context. One main point is, it will go up in price, but how much relative to others (incl MSTR)

All in costs are higher than $50k

Thousands a year, cut in 1/2 every 4, difficulty goes up, mining done at margins

@MARA_investor @CK_Cryptoklepto Yeah okay

🤡

Drop your argument and start focusing on a minor detail so you can be right. Mara business sucks

They’re only relevant b/c of saylor strategy

@DanCote303@CK_Cryptoklepto Here’s something to add

What if a solar flare happens?

Gotta look at all aspects of the business…

Haha

Come on guy

MARA core business is a liability

Mining is done at the margins

MSTR loads with scale way more, with way less operational liability and expenses

@MARA_investor @CK_Cryptoklepto I never said MARA was garbage

Nor that it would go down in price

Implementing the saylor playbook saved their asses

So keep trying to keyboard warrior over your own made up narratives to try and catch me with a fake gotcha moment…

Your emotions blind you

@MARA_investor @CK_Cryptoklepto Yeah last cycle

Keep investing based on previous cycles

Don’t pay any attention to the capital mstr has at their fingertips, the pending bitcoin reserve for US, etc

🤡

$MARA - Now the Chuck E Cheese of $MSTR. Copying the $MSTR playbook is an act of desperation; an admission that buying BTC is a better ROI than their core business, and an attempt to remain relevant.

I'm guessing $MARA's next move will be to lean into the fact they have less of a NAV premium on BTC than $MSTR. $MSTR is at around 3x, $MARA is around 2x.

But unfortunately with $MARA you have exposure to their core business, and there's no telling how much of your investment will get plowed into that vs BTC.

$MARA's core business can mine around 2,000 BTC/quarter (decreasing with network difficulty) at an industry-worst cash hashcost of ~$49.75 ($78,300/BTC at present, increasing with network difficulty).

They spent around a $1.2b dollars on ASICs for this privilege. This is not factored into the above costs, but if you want an approximation then include the 3-year depreciation of those ASICs. This brings it to $85.00 hashcost ($135,000/BTC at present, increasing with network difficulty).

In Q3, they burnt around $6m mining BTC. Effectively, they paid $6m over spot price for 2,070 BTC, funded by dilution.

They have the highest $/KWH costs and, crucially, will not outrun other miners from the bear. When BTC price doesn't outpace network hashrate growth -- which has historically happened 100% of the time -- everything gets worse.

The CEO of $MARA himself has recently gone on a world tour talking all about how mining will only be viable at near-zero power costs.. and here they are, with the highest of their peers. Shareholders have paid $101m YTD in stock-based comp for these ivory tower speeches.

So, what's that business worth? Best not to think about it -- hence the further pivot to $MSTR playbook. They're buying more BTC! They have a big HODL! Big market cap!

Seeing as every $1 invested into $MARA eventually gets burnt as SBC, profitless EH/s growth, or just goes straight to buying BTC to prop up book value (for which you'll be paying up to 2x premium for them to HODL it)... why bother? You can buy BTC yourself, or put money where 100% of it goes to buy BTC.

Contrast $MARA with $MSTR: Basically a vigilante ETF; instead of a creation/redemption mechanism, you take it on faith that every $1 raised will go into BTC. A core business without leveraged exposure to BTC. Less SBC (~$58m YTD) vs $MARA ($101m YTD), despite a 13x difference in market cap.

If you want exposure to mining, far better choices exist. Namely: any. If you want exposure to BTC, then you can buy it, or an ETF, or $MSTR, or (soon) options.

There's basically zero point to owning $MARA. The only realistic upside I see (relative to peers) is that they can achieve the same multiple on NAV as $MSTR (unjustified given the reasons above), or they announce a foray into HPC.

@CK_Cryptoklepto It’s a matter of scale

If they can buy billions worth right now for damn near free (especially if you consider dilution was always happening, now it’s just accretive), but only mine hundreds or thousands even at your “50%” profit margin (bullshit)

They went saylor 4 a reason

@CK_Cryptoklepto It’s a liability

Bro they can issue converts right now and scoop up more coin than they can mine in years, maybe decades

And if you extrapolate price and difficulty adjustments, way cheaper

Also their all in costs suck ass

So MSTR is better value mNAV and liability wise

Here's another major issue with Bitcoin:

If you read the original 2008 white paper, the intention was to create a digital currency.

Nothing was remotely said about it being a store of value.

That idea came once people saw how much its price was rising.

$MARA @MARAHoldings has been (rightfully) getting a lot of attention on their convertible note offerings & running the $MSTR playbook re: Bitcoin treasury strategy.

But they can do smthg @saylor cannot - they can mine it at prices less than spot.

Unlike $MSTR whose core business is software and services, $MARA is a Bitcoin miner, and the highest volume BTC producer in the sector at that. MARA mined 717 BTC in October alone. Even better that vertical is growing.

Monday $MARA added multiple sites in Ohio to their pipeline and now has nearly 1.5 GW (1488 MW) of capacity - 1268 MW current and 200 MW in development

Even better for investors, they continue to move steadily away from the hosting model, now up to 65% self-owned and operated. Better margins, more control over ops.

So they can buy, and they can mine at a price that undercuts spot markets by a solid %, giving them an edge $MSTR cannot match. This gives MARA an interesting twist to their version of the Bitcoin treasury strategy.

Who in the mining sector is going to copy first?

@rogerhamilton@rogerhamilton

I’m sure you’ve already thought of this, but it’s a perfect time to double the sack to $20m to match the MC

Then when bitcoin runs, market cap matches

Obviously the best thing would be $120m

Get the corn while it’s under $100k