Accounts with DLL that have a consistency rule make no sense for the Prop Trader, but make total sense for the Casino Prop 🎰

Example: 50K acct with 3k target 🎯

Consistency: 20% and $1200 DLL

Pushes the trader to make no more than $600 (3k x 0.2). You could be consistent 4 days in a row but odds are you’ll grind this up 200-300 a day.

One day you hit DLL and wipe out 2-7 days of work. You might lose $1300 with slippage. Since consistency is .2 it will take over 3 days to make back 1 bad day without increasing your profit target.

It sucks that if you have a good set of trading sessions the next couple days you would be punished for trading well.

This is the very definition of capping your gains.

💥 The exact opposite of what you need to do when your system is working well!

To make matters worse, as you’ve been making progress towards the profit goal, the EOD daily loss limit has been chasing your high water mark so now you have $500 to $600 left before blowing the account. So you need to be damn near perfect to not blow for the next several weeks or the account is blown. All that time wasted.

This is Inverse Edge to the trader. Another reason most never get to payout.

🔥 HUGE list of single-stock Futures contracts are on schedule for the @CMEGroup this summer!

Should we make these tradeable at @Topstep, @MichaelPatak?

- Contract Size: 100 shares of underlying

- Quarterly Contracts

- Like all Futures, get 23-hour daily trading sessions with stops.

@NoelLeon_II@TakeProfitLLC@Tradeify@TradingLucid With TPT the 25k is the most cracked but requires patience (there’s a post earlier in my feed on it) but the 50k is a fair balance and the intraday is only till you make back buffer. 2-3 trades low size and then it’s a fully static free acc

If I was starting in prop today and actually trusted my edge, I’d stop chasing random discount codes and do this:

Buy 5 accounts at each:

• @TakeProfitLLC 50K

• @Tradeify 50K Select

• @TradingLucid 50K Flex

Why these three?

- They have volume.

- They actually pay.

- And more importantly, they all give you a real path to 5 live accounts with fewer games.

The goal isn’t “pass an eval.”

The goal is to stack live accounts.

- 5 live at TPT

- 5 live at Tradeify

- 5 live at Lucid

That’s 15 live accounts.

Now do the math:

$500/day per account

15 accounts

= $7,500/day

Most traders are still fighting over who has the cheapest account.

The real play is building a live account portfolio.

Wake up.

Expansions are the easiest trades

If you have been studying,

I have given you the blueprint I use for expansions

Use the 25% as confirmation level

Use the 50% as invalidation

If the market respects 25% and confirmed reversal on Intermediate • Lower Timeframe

expansion confirmed

The 50% as a intermediate invalidation point.

If bullish, bearish moves towards this 50% is retracements

If bearish, bullish moves to wards this 50% is retracements

The closer price gets to the 50% depending on the previous range

the lower the likelihood of large expansion

apply this to the higher timeframes

watch the outcome

>> Chinese media report: YMTC’s 1Q revenue surpasses RMB 20 billion ($3B) as it undergoes “epic-scale capacity expansion”

• China’s memory semiconductor maker YMTC is reportedly moving ahead with ultra-fast capacity expansion to respond to a surge in large-volume storage chip orders. According to supply chain sources, YMTC’s revenue in 1Q 2026 exceeded RMB 20 billion, more than doubling YoY. Its NAND flash output has reportedly surpassed 10% of the global market, putting it close to the global top three. One core industry source said, “Profits will explode even more from here.”

• To secure capacity, YMTC has already completed one new fab this year and is planning to build two additional fabs. Once all of them are fully ramped, total capacity is expected to more than double. Each fab is reportedly targeting monthly capacity of 100,000 wafers, which industry sources described as “epic-scale expansion.” The fab buildings are already completed.

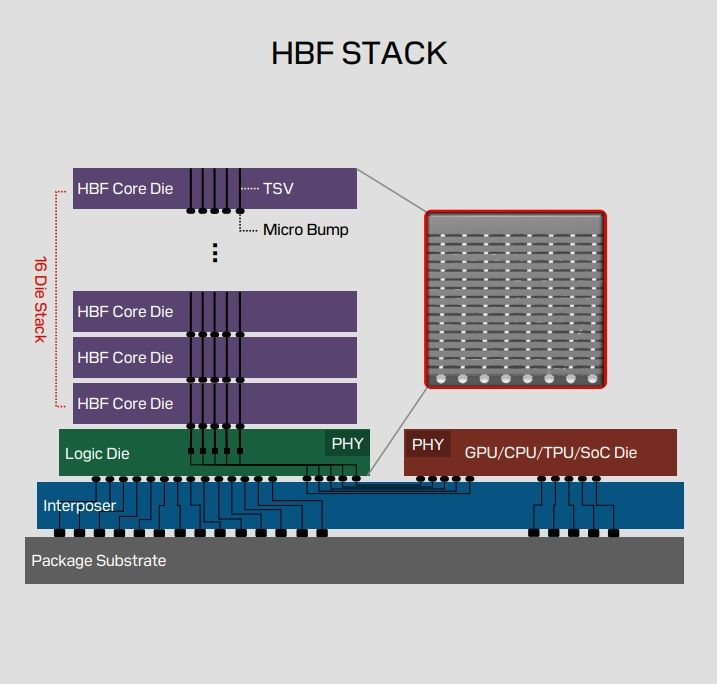

NAND Stacking 'HBF' Process Market Opens… SanDisk Begins Building Supply Chain

The market for 'High Bandwidth Flash (HBF)' — a process that dramatically boosts performance and capacity by stacking NAND flash memory in a manner similar to High Bandwidth Memory (HBM) — has officially opened. This comes as SanDisk, which first unveiled HBF technology, has begun building out its materials, components, and equipment supply chain. With major memory manufacturers successively launching HBF development efforts, attention is turning to whether it will generate manufacturing demand on par with HBM.

According to industry sources on April 13, SanDisk has begun establishing an ecosystem with related supply chain partners to set up a pilot production line for HBF prototypes. The company plans to showcase prototypes in the second half of this year, and this is understood to involve the construction of a new pilot line. Japan is emerging as the leading candidate for the production site.

A senior supply chain industry executive said, "SanDisk is in discussions with materials and equipment companies, targeting major equipment installation in H2," adding that "some companies have already begun purchase order (PO) negotiations." The industry expects the pilot line buildout to be completed in H2 with operations commencing around year-end. Commercial production is targeted for next year.

HBF is a next-generation flash memory concept unveiled by SanDisk in February of last year. Its core architecture is similar to HBM. HBM, which has seen rapid growth recently as it underpins AI computation, achieves dramatically higher speed (bandwidth) and performance by stacking DRAM. HBF instead stacks NAND flash to increase not only bandwidth but also capacity. While HBM is a memory optimized for speed — real-time computation for AI training — HBF maximizes capacity. Unlike DRAM, NAND retains data without power (non-volatile), drawing attention as a new storage solution for AI.

As HBF production infrastructure buildout accelerates, demand for process-related materials, components, and equipment is also expected to expand — signaling the emergence of an entirely new process market for manufacturing an unprecedented product. With SK Hynix and Samsung Electronics also preparing HBF alongside SanDisk, the pace of market growth could accelerate. SK Hynix is collaborating with SanDisk on HBF standardization and other initiatives, while Samsung Electronics is independently gearing up to enter the market.

Professor Kim Jung-ho of KAIST, at an HBF technology roadmap presentation in February, projected that HBF could surpass HBM in market size by 2038.

The HBF process is expected to favor the existing supply chain ecosystem that has served HBM manufacturing, given the process similarities. Through-Silicon Vias (TSVs) are used to transmit signals between stacked NAND layers. The industry consensus is that companies that have established competitiveness in bonding materials and equipment (bonders) for HBM will maintain their positions in HBF as well.

An industry source stated, "Given that HBF and HBM manufacturing do not differ significantly, there is a very high probability that the process ecosystem led by Samsung Electronics and SK Hynix in the existing HBM market will carry over directly into the HBF market."

$SNDK

Why is Lucid better than most firms?

Here’s another reason 👇🏻

$25K Tradeify Select - $109

$25K Lucid Flex - $100

(No discounts applied)

Use code: PLAZA (40% OFF + BOGO)

Lucid is built for traders’ success 💚

Comment below, if you really loves Lucid!

Samsung Electronics Places Equipment Orders for Final P4 Lines… Accelerating HBM Mass Production

Samsung Electronics' capital investment for its 4th Pyeongtaek Campus (P4) is entering the final stage. It has been confirmed that the company placed manufacturing equipment orders last month for the remaining 2 phases (out of a total of 4) where investment had not yet been executed.

These lines are dedicated to mass production of Samsung Electronics' most advanced DRAM process, 1c (6th-generation 10nm-class) DRAM. 1c DRAM serves as the core die for Samsung's HBM4 (6th-generation High Bandwidth Memory) and is drawing significant attention as a critical component for business with global big tech customers including NVIDIA.

According to ZDNet Korea reporting on April 6, Samsung Electronics recently placed a blanket order for front-end process equipment for two buildings — ph2 and ph4 — within P4.

P4 is Samsung Electronics' advanced semiconductor fab. Originally designed as a comprehensive fab for DRAM, NAND, and foundry production, the majority of its production capacity has been allocated to DRAM due to market conditions and other factors. Among its output, it produces the most advanced process-based 1c (6th-generation 10nm-class) DRAM.

P4 is divided into a total of 4 phases. The construction sequence is 1-3-4-2. Ph1, which was built first, has already completed all investment. Ph3 has also been under investment since H2 last year, with most equipment setup now finalized.

This year, front-end process (the process of etching circuits onto semiconductor wafers) equipment investment is expected to proceed actively for the remaining ph4 and ph2. According to multiple equipment industry sources, Samsung Electronics issued purchase orders (POs) for front-end process equipment for ph4 and ph2 at the end of last month.

Accordingly, front-end equipment is planned to be installed in ph4 starting around May–June. Equipment installation for ph2 is scheduled for around November. Cleanroom construction work for equipment installation in ph2 already began in Q1 this year. A cleanroom is an infrastructure facility that controls contamination levels and other environmental factors essential for semiconductor manufacturing. It must be installed before front-end process equipment can be brought in.

With this PO placement, Samsung Electronics' P4 construction timeline has become clear. Samsung has been accelerating new and conversion-related capital investment recently to respond in a timely manner to the semiconductor supercycle triggered by global AI infrastructure investment.

In fact, front-end equipment for P4 ph2 had previously been expected to be ordered at year-end, with actual installation taking place next year. Considering this, the actual installation timeline has been pulled forward by approximately 2 months.

In particular, 1c DRAM plays a central role in the company's high-value-added memory business. Samsung Electronics adopted 1c DRAM — one generation ahead of competitors — for its HBM4, which entered full-scale mass production this year. As a result, Samsung is assessed to have achieved the highest performance in HBM4 for its key customer NVIDIA.

This year, Samsung's 1c DRAM production capacity is expected to reflect the P4 ph3 buildout. In numerical terms, this amounts to approximately 130,000–140,000 wafers per month. The completion of front-end equipment setup in ph2 is expected around Q1 next year. Including 1c DRAM conversion investments planned for next year at P3 and the Hwaseong Line 17, production capacity is projected to continue expanding.

A semiconductor industry source explained, "Samsung Electronics has been showing a proactive willingness toward capital investment, to the extent of placing advance equipment orders for ph2 with its partners," adding, "High-value-added DRAM is in the spotlight within the AI industry, and there is a prevailing atmosphere of preparing investments ahead of time to avoid uncertainties arising from the recent war."

MS and Google Pursuing LTA with SK Hynix

SK Hynix is entering into long-term supply agreements (LTAs) for DRAM with major global AI companies including Microsoft (MS) and Google. Big Tech is moving to lock in DRAM—a product known for high price volatility—over extended periods. As concerns over DRAM supply shortages intensify amid the global AI infrastructure investment boom, Big Tech is strategizing to secure stable access to memory, a critical component for data centers. Samsung Electronics and SK Hynix, the world's No. 1 and No. 2 DRAM makers, are ramping up capital expenditure in response to the growing supply-demand imbalance.

◇ MS and Google Arrive with Long-Term DRAM Contracts

According to industry sources on the 5th, SK Hynix is in final-stage negotiations with MS on a long-term supply agreement for DDR5. The deal, valued in the tens of trillions of won, would cover a three-year period starting this year. Discussions are reportedly centered on provisions such as a price floor to hedge against significant DRAM ASP declines during the contract period, and terms under which 10–30% of the total contract value would be paid upfront.

SK Hynix is also in discussions with Google on a long-term supply agreement. The negotiations reportedly cover not only its flagship High Bandwidth Memory (HBM) but also commodity DRAM used in servers. MS and Google are also pursuing long-term memory supply agreements with Samsung Electronics. Micron Technology, the U.S.-based No. 3 DRAM maker behind Samsung and SK Hynix, reportedly signed a similar contract last month.

◇ "Securing Volume Matters More Than Price"

A long-term supply agreement is a contract in which volume and pricing are predetermined over an extended period. This type of agreement is typically employed when prices for a specific product surge or supply becomes scarce. Until now, large companies like MS and Google had not entered into annual or multi-year memory supply contracts with memory manufacturers, given that memory is a highly cyclical product subject to significant price volatility.

Nevertheless, Big Tech has recently been approaching Samsung Electronics and SK Hynix with LTA proposals one after another due to an increasingly acute memory shortage. Memory supply has tightened significantly as AI infrastructure investment expands worldwide, and prices have surged accordingly. According to DRAMeXchange, the DDR4 contract price, which stood at just $1.35 in March of last year, skyrocketed to $13.00 by the end of last month.

Moreover, as the AI infrastructure hegemony race appears set to become protracted, analysts note that AI companies have shifted to a strategy of securing volume first. A senior semiconductor industry executive explained, "Right now, the fact that prices have risen so much is secondary—the real issue is that DRAM volume itself is extremely difficult to procure."

◇ Samsung and SK Hynix to Significantly Expand DRAM CAPEX

Samsung Electronics and SK Hynix have decided to aggressively invest in DRAM capacity this year in light of these conditions. Samsung Electronics is focusing on ramping up volume of 10nm-class 6th-generation (1c) DRAM—used in HBM4—at its main DRAM production base, the Pyeongtaek campus in Gyeonggi Province. At its Hwaseong campus, the company is accelerating process migration to 10nm-class 5th-generation (1b) DRAM, which serves as the base die for SOCAMM and commodity DRAM modules.

SK Hynix is addressing new HBM volume demand centered on M15X, its new production base in Cheongju, North Chungcheong Province. Its headquarters campus in Icheon, Gyeonggi Province, is also aggressively pursuing process migration to its most advanced 1c DRAM node.

Driven by the DRAM supply crunch, both companies' Q1 earnings are estimated to reach all-time highs. In a report on the 3rd, Meritz Securities projected Samsung Electronics' Q1 estimated revenue at KRW 122 trillion and operating profit at KRW 54 trillion. The estimated operating profit is more than triple the previous Q1 record of KRW 14.12 trillion set in 2022. FnGuide estimates SK Hynix's Q1 revenue at KRW 46.6252 trillion and operating profit at KRW 31.5627 trillion—4.2x the KRW 7.4405 trillion reported in the year-ago quarter.

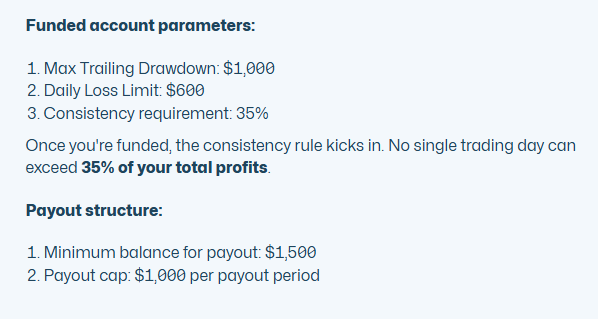

I love 25k accounts.

Tradiefy is cooking. $59 one time payment for a 25k account that rivals the 25k pro from Lucid.

Pass it in one day, activate it same day, 35% consistency to the payout.

$1,000 max payout, or $5,000 with a $295 spend.

@BrettSimba you answered my wish.

DDR5 prices have seen a significant drop recently after we've seen several key trend changes:

1) OpenAI pulling back meaningfully on spend. Going from $1.4T in planned data center build-outs and buying 40% of the world's raw wafer supply to now renting compute.

2) More efficient AI hardware, inference and models reducing baseline hardware requirements for building out data center-scale capacity. The progress that's been made over the last year changes the entire game.

3) Debt markets souring on AI CapEx spend, with stress showing up in credit default swaps and diminishing investor appetite for AI-related debt.

I suspect this could be the beginning of a broader trend of reconsidering the scale of commitment to building out compute.

Particularly because as technology becomes more efficient, it also evolves and becomes cheaper. Rewarding some for deferring spend to future generations of hardware outside of core capacity build-outs.

All-in-all it's worth watching to see if prices continue to drop. The long memory trade became very, very crowded before the big sell-off recently. It's still a cyclical industry and one where demand trends often change violently.

Meaning any complacency about NTM PEs and where things may go even more than 3-6 months forward is often misplaced.

Be nimble, my friends. Remember that everything is moving very fast right now.

TrendForce Raises Q1/Q2 2026 DRAM & NAND Price Forecasts

Q1 2026

- PC DRAM Blended ASP: revised up from +50~55% to +110~115%

- Server DRAM Blended ASP: revised up from +60~65% to +93~98%

- Mobile DRAM Blended ASP: revised up from +45~50% to +58~63%

- Overall DRAM Blended ASP: revised up from +55~60% to +93~98%

- eSSD prices: revised up from +33~38% to +75~80%

TLC/QLC NAND prices: revised up from +30~35% to +75~80%

- Overall NAND Blended ASP: revised up from +33~38% to +85~90%

Q2 2026

- PC DRAM prices: revised up from +10~15% to +40~45%

- Server DRAM prices: revised up from +10~15% to +43~48%

- Mobile DRAM (LP5X) prices: revised up from +13~18% to +58~63%

- eSSD prices: revised up from +15~20% to +68~73%

- TLC/QLC NAND prices: revised up from +15~20% to +60~65%

- Overall NAND Blended ASP: revised up from +18~23% to +70~75%

Insane if correct, DRAM & NAND continue to rise, remember how $MU beat the estimate last quarter?

Nomura now sees Q2 memory pricing exploding far above prior forecasts

-Commodity DRAM is now forecast to rise 51% QoQ, versus the prior +6% estimate.

- NAND is now forecast to rise 50% QoQ, versus the prior +20% estimate.

SK hynix estimate revisions:

- 2026F operating profit raised to KRW 256T, about US$175.3B, up 36% from prior KRW 189T.

- 2027F operating profit raised to KRW 365T, about US$253.1B, up 37% from prior KRW 267T.

Operating margin forecast is 74% for both 2026F and 2027F.

Net profit forecast:

- 2026F: KRW 205.5T

- 2027F: KRW 293.5T

Source below.

Why is #HBM placed right next to the GPU? 🤔

It's an architectural necessity. @SKhynix is closing the physical gap to deliver massive bandwidth, ultra-low latency, and better power efficiency.

Swipe through to see the logic behind #HBM4.👇

#SKhynix#HBMWHY#AIMemory