The U.S. homeowners insurance market is under unprecedented stress from severe climate risks. @blcollier2, Benjamin Keys, and @Philipcheesy1 propose the creation of a federal property reinsurer, US Re, to stabilize financing for catastrophic losses: https://t.co/OlNbLqy2Y4

Takeaway: Frictional costs of managing tail risks help explain the rapid rise of homeowners insurance premiums in Florida.

To improve affordability, policy could focus on reducing these costs, e.g., expanding reinsurance supply.

Preliminary paper here: https://t.co/LUFIzpvCVh

Home insurance premiums are skyrocketing. How much is due to growing climate risk? 🌪️🏠

In our new paper, we use unique data from Florida—which has some of the highest premiums in the US—to open the "black box" of hurricane insurance pricing. 🧵

w/ @JuddBoomhower@Tobias_Huber8

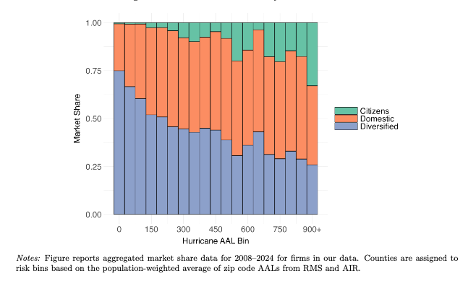

This cost is compounded by the market structure. National insurers ration coverage in high risk areas and are replaced by "Florida-only" domestic firms.

These smaller firms rely heavily on reinsurance, spending $0.58 on it for every $1 in premiums they collect.

Climate change is upending insurance markets, which threatens mortgage markets, which risks triggering a property values crash.

@SenWhitehouse leads a hearing to highlight new data and which markets may be next to fall. WATCH ⤵️ https://t.co/EnnI94Xuha

Hey #econtwitter! Dropping back over to tell you about a great Wharton job candidate! Xian Ng studies whether households are able to optimize over financial products with different up-front versus sustained payments. This area often has a tradeoff b/t identification and stakes 🧵

Around an approval discontinuity, Federal Disaster Loans causally reduces severe financial distress, decreasing bankruptcy filings by 61 percent in the 3 years after the disaster, from @blcollier2, Daniel A. Hartley, @Key_Z_E, and Jing Xian Ng https://t.co/sGKpW9nCIO

The 16th Conference on Urban & Regional Economics is back in Philly Nov 8-9. If you’ve participated before, you know that the conference strives to provide a forum for extensive discussion of the newest and most innovative research in the field. Apply to participate by Aug 23!

🚨New paper on the effects of emergency credit!🧵

We find that timely liquidity provision after a severe climate event has large effects on consumer financial health. Federal disaster loans causally reduce bankruptcy filing by 61% in the three years after a natural disaster.

We find large, persistent benefits of liquidity provision precisely when it is most needed. Denied HHs can’t find credit in private markets, exacerbating the cost of the shock. The lack of private credit suggests an important role for public credit markets in times of need.