Just pointing out that SoFi's 10-Q filed this morning contains the exact disclosure I said was required by GAAP - which SoFi never provided before. Having said that, I now agree with you that engaging extensively in Xon these topics is not the best use of my time. Figured you might appreciate the update!

@ewarren You eliminated American jobs, hurt those people's families, and raised prices for Americans.

Try to think through the consequences of your actions before thinking about your talking points.

@claraliang@claraliang thank you for sharing. Did you listen in on the SoFi earnings call this morning? I was hoping that SoFi would address some important accounting questions addressed at length here: https://t.co/x8FYDsKrsx

@ElhuronD33244@anthonynoto Let’s be honest. If every bank is as bad you claim, then banks should not be granted special privileges over non-banks for crypto. PS, not paid by anyone. My identity is as irrelevant as the empty rhetoric employed by SoFi.

You said: “In the report, he attempts to suggest that the numbers are off for interest and non- interest income.” Never said that or anything remotely like that. If I did say that, please share the copy and paste. The entire discussion is screenshotted here. You must be really misunderstanding what you are reading.

It wasn't intended to "attack character." I was just attempting to point out that third parties (Goldman partners leaking to the NY Times), Twitter investors had made independent assertions in the past that Noto was essentially too optimistic and upbeat, not transparent enough. I don't think Noto is a bad "character." In fact, I think it is obvious he is capable, bright, hard working. He is clearly a competitive, type A personality. It doesn't take much of a leap to believe he lives and breathes SoFi and has put his all into SoFi every day for the last 8 years. He surely genuinely wants to maximize shareholder value and does not have bad intentions. My simple point is this: as a CEO its very important to paint an accurate picture of the company. That is true even if it means taking a less than optimistic tone or even if it means disappointing investors or others. In my own professional life, there are times where I've been optimistic and should have been more realistic, so I do not regard that as a character issue. Our natural behavior is to spread optimism, to try to avoid disappointing others, and to keep trying again and again. The issue is that as CEO, billions of dollars are at stake: investors' life savings, college funds, institutional pension funds investors, thousands of employees. They are all counting on SoFi and SoFi makes the situation worse if SoFi is not being upfront about negative facts about company performance.

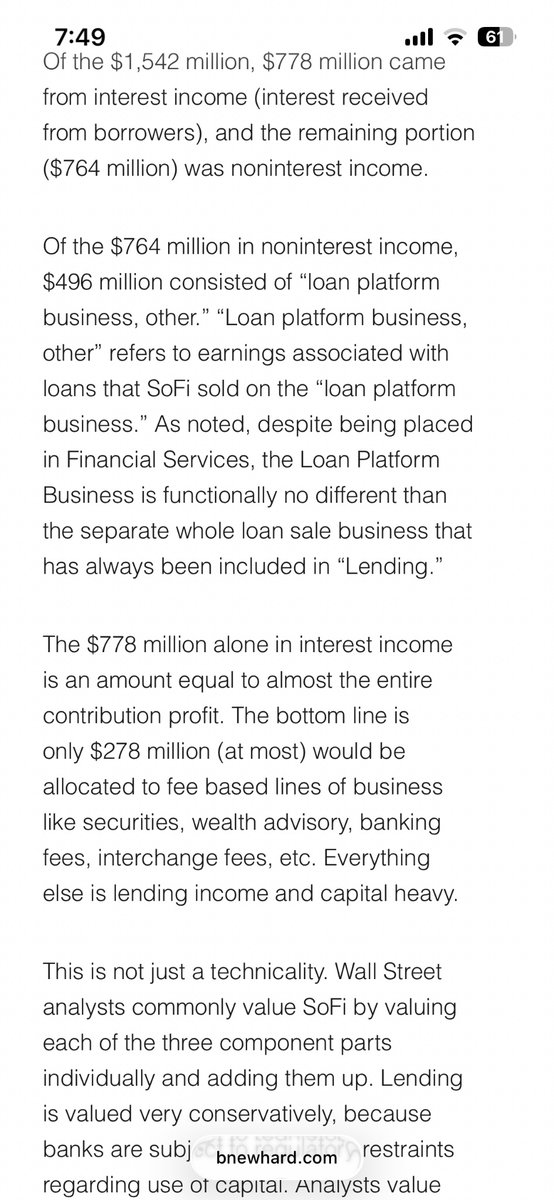

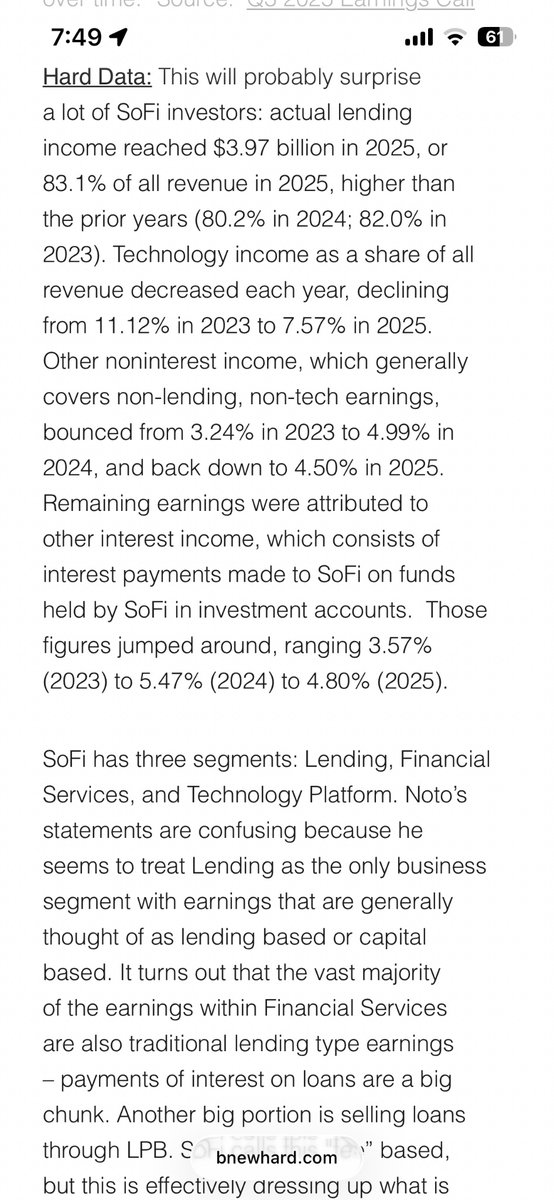

You are confusing me with someone else. I am not Muddy Waters. I wasn't involved in his report. I never went on TV. I haven't really brought up securitizations. What I attempted to do in my report was contrast narratives spun by SoFi with basic, contradictory facts from their own filings or basic data from resources like the Federal Reserve. I think investors ought to know that even though SoFi says its members are high earning young professionals, federal banking data shows that the average account size at SoFi is miniscule, far smaller than other digital banks. Investors should know that even though SoFi says it is diversifying into non-lending and non-capital intensive earnings, that assertion is based based on twisting some creative accounting. SoFi's own income statement reflects that in 2025, lending based income was about 83% of all revenue, higher than both 2024 and 2023. Investors are told that SoFi has a flywheel, efficient, one stop shop infrastructure and has an advantage over legacy banks due to non physical locations, but Federal Reserve Data shows SoFi is at the very bottom of banks with more than $10 billion in assets on a range of efficiency and profitability (on asset basis) metrics. Even SoFi's occupancy expenses are the very worst (worse than 95% of other banks), which is hard to fathom as a digital bank with branches (How could this be? SoFi has 14 offices spread around the globe). These are all black and white facts straight from SoFi's own submissions, and they contradict the image of a nimble, diverse tech-bank hybrid that everyone has when they think of SoFi.

Fine by me. You keep initiating comments at me and not vice versa. I’m comfortable in my position since I did the functional equivalent of reaching out to many people who understand the topic better than me: Big 4 guides, multiple AI programs, etc and there was a clear consensus. We shall see what happens in the future.

Those were all screenshots from the NY Times article. The font was slightly smaller on some of the quotes because of how I was screenshotting the article. Full article is linked below (unlocked). Ultimately it’s your money invested in SoFi, not mine. If you’re comfortable that you have all the relevant info, and don’t want to look at any other material, that is your choice. On the flip side, if things go south and shareholder lawsuits are filed against SoFi based on issues I’ve raised, would be an honorable act of integrity if you opted out and refused to partake in a settlement. Because someone who makes the deliberate choice not to research something shouldn’t later claim to have been a fraud victim. Those settlement pots never cover the full amount of damages, and commonly the less participation in the class action results in the participants obtaining a greater pro rata share of settlement funds. A lot of SoFi investors are not making a deliberate decision to not research certain issues about the company, and they ought to be compensated if turns out that SoFi engaged in securities misconduct. NY Times link: https://t.co/Oepyo9USI6

It’s my basic human ability to read the English language, perform research, and interpret documents. In my professional life I’ve occasionally dealt with accounting issues, certainly nothing like this though. Generally, if I had performed zero research on a GAAP issue, I would default to deferring to an actual accountant with experience over my layman understanding. On this precise issue, I’ve looked up all the big 4 guidance, ran it by 3 or 4 AI programs, looked up how the big banks do it, looked up sec comment letters. The consensus across the board is that disclosing unrealized gains is an absolute standalone disclosure requirement. I noticed a couple (maybe 1 or 2 that I spot checked) fintech companies do not disclose unrealized gains/losses, consistent with the SoFi approach. I suspect the unrealized gain/realized gain disclosure would result in bad optics and these companies are using a strained interpretation of GAAP to support their omission of this disclosure. This is such a niche issue, and the roll forward table is otherwise complete, that I can see how it could get past auditors or particularly the SEC, which lacks the resources to do a full cavity search on each filing that comes in.

@pwallacep7 @DazzDaBozz @Futurenvesting That’s instrument specific credit risk. Not unrealized gains. Instrument specific credit risk is a separate disclosure requirement under 520.

No, different company, 2 years ago. But same exact accounting issue and rule. No reason to expect the SEC to enforce this straightforward GAAP disclosure rule inconsistently among public companies. All the major banks show unrealized/realized breakdown. I don’t think SoFi will have any legitimate argument that its presentation complies and SoFi will be forced to modify it.

Maybe I will become a slightly more active investor. I was heavily influenced by the book "A Random Walk Down Wall Street" when I read it in college. Ever since then, I have been convinced that individual investors, in the long run, cannot beat market returns. And I still think that is mostly true, but going through this research and subsequent dialogue, I have modified my beliefs a little bit. As far as giving my report credibility, I've repeatedly said I am not a finance or stock guy. And I am not giving financial advice. But people can judge the full report for what it is. It is heavily footnoted and very detailed, with lots of supporting evidence excerpted or screenshoted. I don't think I've had one person point out a single fact I simply got wrong. I've heard critiques of MW's short report directed at me, but I didn't draft that report. Someone criticized that I compared SoFi's discount rate with other lenders like Upstart, which is more of an analytical point than a factual error, but certainly a good faith criticism. But I also compared SoFi's discount to federal note yields, investment grade corporate bond yields, and mainstream bank discount rates. So even if comparing SoFi to Upstart is an error, it doesn't really detract from the basic analysis (and personally I think it is fair to compare SoFi to Upstart or other fintech lenders, because discount rate is not an "all in one" risk rating - other lenders may have higher default rates, but they command higher interest rates - discount rate isn't a proxy for default risk, especially since default rate is a completely separate input on the valuation model). I've had back and forth with you and Tim S. on the unrealized/realized gain issue, and I've seen no reason to back off my position that SoFi violates GAAP. Tim has taken the position that tax liens against a bank are a "lol," which is hard to take seriously. You're probably the only one to really engage on any details with any seriousness (the ASC 820-10-50-2.d issue) - and just today I found multiple recent SEC comment letters where companies were told to provide the realized/unrealized breakdown, exactly like I said is required. So it seems unlikely that the SEC will change course. I think it is highly likely that SoFi will have to restate their financials at least on this point and I suspect this bit of information will be disastrous because it will expose the extent to which SoFi's fair value model has generated inflated earnings. Link: https://t.co/PWG7GeQNZx excerpt below.

I never suggested he got kicked out of Goldman. In fact, I noted that he became known as the best analyst and turned around his reputation. You are successfully attacking a position I never took. The simple point is, he was criticized for being too enthusiastic about many internet companies (eToys, Webvan, Homestore, Asford) that ended up bankrupt, to the point that he was known as "Anthony Don't Know." That's irrefutable. Excerpts from NY Times article below:

He wasn’t “right” at Goldman- he notoriously overhyped internet companies that went bust- not future parts of Amazon. To his credit, he turned it around and became known as the very best analyst, but I see the same overly positive and upbeat attitude at SoFi that he was criticized over by his own Goldman colleagues . I don’t think there is one thing on that report (which is a drop in the ocean of what I found) this has anything to do with a screwed up basket of loans. I welcome you demonstrating that I am not qualified to understand what I wrote. -> https://t.co/Gp1RySYrRs

That report literally quotes the NY Times verbatim; then recites the allegations of a lawsuit filed against Noto/Twitter which resulted in a 800 million settlement; and finally exactly quotes managements statements and then provides seemingly inconsistent or contradictory information. Last time I checked it wasn’t slander to report or recite on the allegations of others - or to quote verbatim statements or informations. I find the NY Times and Twitter lawsuit allegations both compelling personally. They show long track record of excessively upbeat/optimistic analysis, and a prior lack of transparency with investors.

@marketswithmay You obviously didn’t go to the link. I’m not referring to MW’s report. I’m not MW. The link compiled various statements made by SoFi management that have credibility concerns on key issues. No one has refuted or adequately explained those away.