I share with you now, one of my highest conviction bets for the next 4-5 Years or maybe for the next 20 years...it is disrupting a whole industry with no competition at all and has a monopoly position....i never see this in my whole life in the stock market...I like to hear your comments and happy to see some likes to see you appreciate my ideas =)

The 3,000-Year-Old Gold Standard is Dead—But the Real Story is "Beyond Gold." 🌍⚒️

A Deep Dive into Chrysos Corporation $C79.AX and why this tech monopoly is the ultimate pick-and-shovel play for the commodity supercycle.

The Problem vs. The Solution

The mining industry still heavily relies on "Fire Assay," a 3,000-year-old method to measure gold.

It is painstakingly slow (24-48 hours), uses tiny 50g samples (prone to massive error margins), and requires smelting with toxic lead.

Enter Chrysos Corporation. Spun out of Australia’s national science agency (CSIRO), $C79 replaces Fire Assay with high-energy X-rays: PhotonAssay™.

The advantages represent an absolute paradigm shift: ⚡ Speed: Results in 2 minutes instead of days.

⚖️ Accuracy: Uses 500g+ samples, entirely eliminating the "nugget effect."

♻️ 100% Chemical Free: Zero toxic lead waste & ~60% lower CO2 emissions per scan.

📦 Non-Destructive: Samples aren't destroyed and can be re-tested later.

The Business Model = Pure Leverage 📈

Chrysos doesn’t sell machines. They operate a pure Technology-as-a-Service (TaaS) model, collecting recurring lease fees & royalties per scan.

Once installed, clients max out machine capacity.

The operational leverage is staggering: 1H FY26 EBITDA exploded +152% YoY.

🚨 The Ultimate Catalyst: "Beyond Gold" & Concurrent Analysis

Silver and Copper analysis are now commercially live, massively expanding their Total Addressable Market (TAM).

Near-term R&D unlocks Zinc, Lead, and Uranium, with long-term potential for Rare Earths and Energy Metals.

Here is the financial magic: Concurrent Analysis. 🪄

PhotonAssay can measure multiple elements (e.g., Gold + Copper + Silver) in a SINGLE scan.

This drives up revenue per sample with virtually ZERO additional OPEX. It is pure margin expansion flowing straight to the bottom line.

Valuation Snapshot (April 2026) 📊

🔹 Market Cap: ~$900M AUD 🔹 Net Debt (excl. leases): ~$33M AUD

🔹 Enterprise Value (EV): ~$933M AUD

🔹 EBITDA (FY26 Est.): $20M - $27M AUD

🔹 1H Margin: Expanded from 20% to 33% YoY.

The market is pricing in a SaaS monopoly, and for good reason.

$C79 has NO direct peers.

Traditional mining labs trade at 10-15x EV/EBITDA but are plagued by cyclicality, high labor costs, and heavy carbon footprints.

Chrysos commands tech multiples thanks to ~90% incremental margins on extra scans and impenetrable CSIRO patents.

2030 "Blue Sky" Scenario 🚀

Capturing the broader energy metals market could easily scale 2030 Revenue to $500M-$600M AUD. With concurrent scanning pushing EBITDA margins past 55%, EBITDA could hit ~$300M. Even applying a compressed, mature 15x multiple, EV approaches $4.5B AUD.

Opportunities & Risks ⚖️

🟢 Opportunities: Global ESG mandates will eventually force a total phase-out of Fire Assay.

🔴 Risks: Heavy capital intensity to manufacture new units and reliance on major lab partners (like MSALABS) for global rollouts.

Conclusion:

Chrysos is no longer just a gold play; it is the ultimate technology-infrastructure layer for the future of all mining.

For investors wanting exposure to the commodity supercycle without the drill-bit risk, $C79 is the apex asset hiding in plain sight.

Disclaimer: Not financial advice. Mining is high risk. Always do your own DD.

📢 You can now rent cars with 100+ cryptocurrencies on Travala 🚗🔥

✅ 1,700+ top-tier suppliers

✅ 50,000+ locations worldwide

Your one-stop shop for crypto travel 🧳

BOOK NOW: https://t.co/bUoqkZYCil

📢 You can now book car rentals with @Binance Pay on Travala 🚗

Rent cars seamlessly with Binance Pay around the world!

🔹 1,700+ top-tier suppliers

🔹 50,000+ locations worldwide

BOOK NOW: https://t.co/bUoqkZYCil

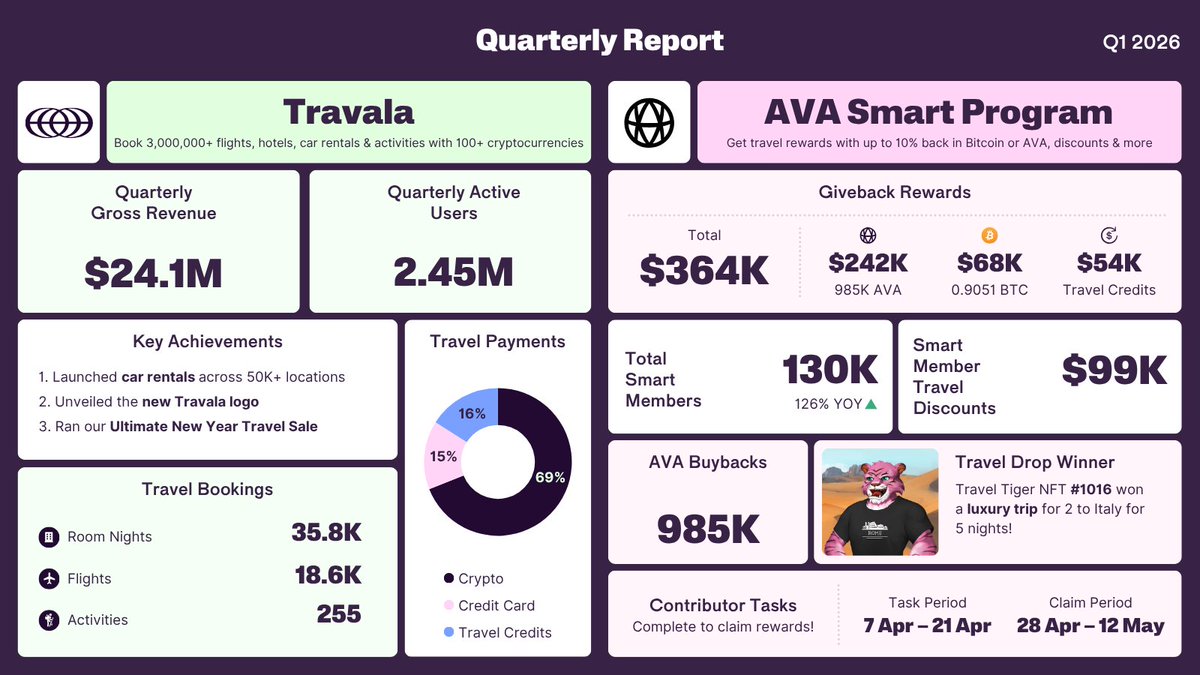

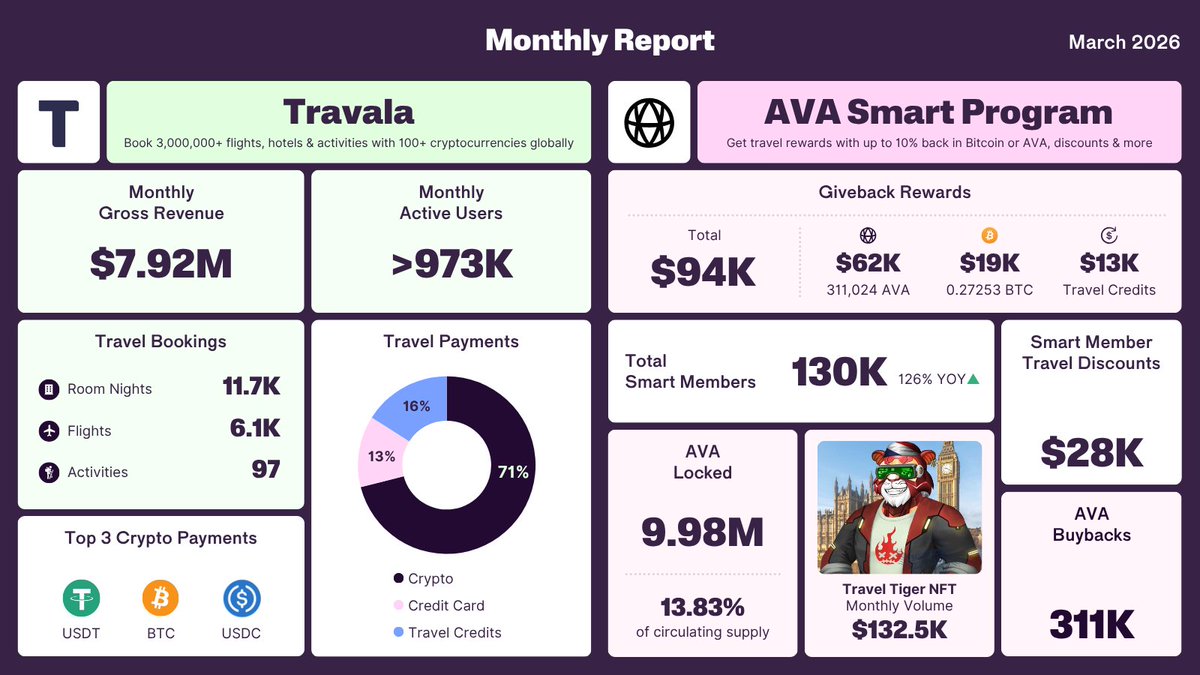

Travala Monthly Report: March 2026

View the March stats across Travala & the @AVAFoundation Smart Program.

Key Stats:

🔹 Monthly gross revenue: $7.92M

🔹 Monthly active users: >973K

🔹 Total giveback rewards: $94K

Full report below 👇

https://t.co/3vmKaISx9X

Travala aims to be a one-stop shop where users can manage their entire journey—flights, hotels, activities, and car rentals—on a single platform. The goal is to eliminate the fragmented nature of modern travel planning.

https://t.co/HKqGivk9EJ

📢 Travala is the Official Travel Partner of Istanbul Blockchain Week 2026

@IstanbulBlockWk is Türkiye's flagship Web3 conference 🇹🇷

📍 Istanbul, Turkey

📅 June 2–3

Get $100 OFF your flights, hotels & activities ✈️

Sign up or log in via this link 👉 https://t.co/KFXDwdvNdL

🔥 NEW Travala Sprint is LIVE on @zealy_io

Thinking about signing up on Travala?

Now you get rewarded for it!

✅ $500 prize pool

✅ 50 leaderboard winners

✅ 5 × $100 USDC raffle

Book flights, hotels & cars with crypto✈️

🗓 Ends April 30

👉 https://t.co/UYgROFiayk

$AVA Travala smart membership is a great chance to get up to 10 % Cash back on your bookings, good idea is to use it on company bookings 😅😊

@AVAFoundation@Travalacom

📢 RENT CARS WITH CRYPTO 🚗💨

You can now book car rentals from 1,700+ top-tier suppliers like @Avis, @Europcar, @Sixt, @Enterprise, and @Hertz

📍 50,000+ locations worldwide

BOOK NOW: https://t.co/GAOBV0ce8q

For more details, check out our blog: https://t.co/hr1i7rQsrr

📢 Introducing the New Travala Logo

Since 2017, Travala has been connecting the worlds of travel and Web3.

Today, we proudly unveil our new logo and brand identity. A future-focused design built for travellers without borders.

Learn more in our blog: https://t.co/aWLNZrSvnw

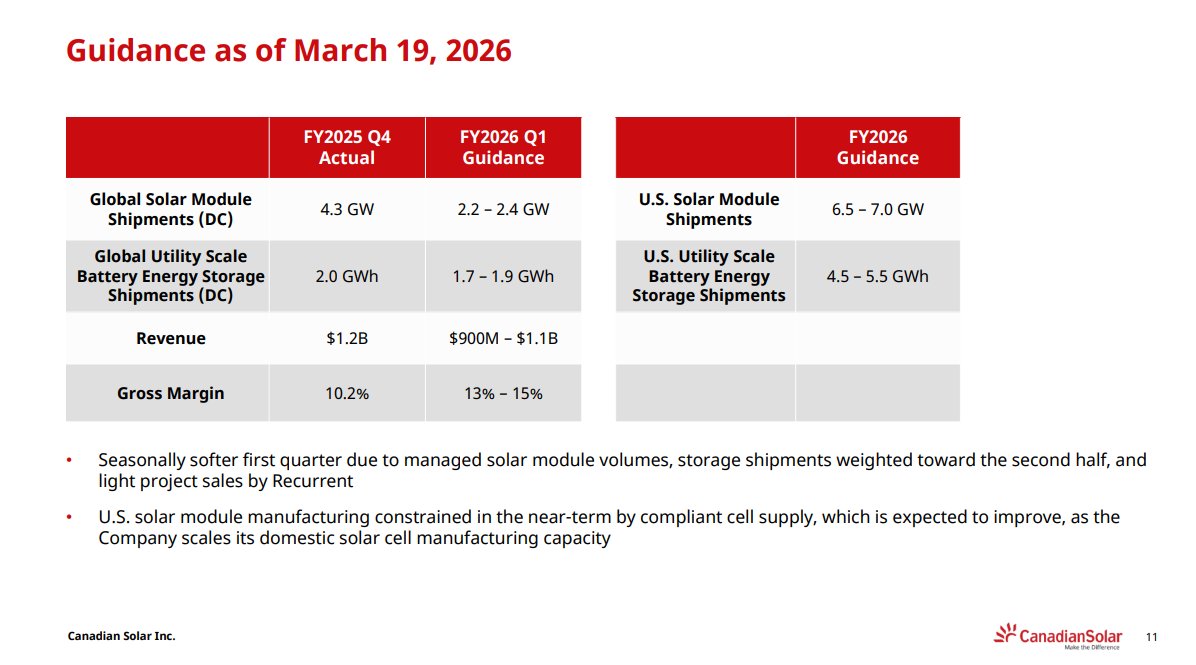

THE SLEEPING GIANT OF THE ENERGY TRANSITION: Why $CSIQ is no longer just a "Solar Play" 🧵

1/ The Company & DNA 🇨🇦🇨🇳

Founded in 2001 by Dr. Shawn Qu, Canadian Solar has evolved from a simple module manufacturer into a global renewable energy powerhouse.

Structure: A unique hybrid. Headquartered in Canada, listed on NASDAQ ($CSIQ), with its massive operational arm, CSI Solar, carved out and listed in Shanghai (https://t.co/73DbH4fL8f).

Ownership: Dr. Shawn Qu remains a visionary anchor shareholder, aligning management with long-term value creation.

2/ The Great Pivot: From Panels to Power Solutions 🔋

The "Old" Canadian Solar was a cyclical hardware play. The "New" Canadian Solar is a high-margin Energy Solution provider.

Segment A: CSI Solar (Modules & e-STORAGE).

Segment B: Recurrent Energy.

Transitioning from "Develop-to-Sell" to an IPP (Independent Power Producer) model. They aren't just building plants; they are owning the cash flow.

3/ Product Edge: e-STORAGE & TopCon ⚡

While others fight a price war in modules, $CSIQ is winning in Energy Storage.

SolBank: Their proprietary LFP battery system is seeing 100%+ YoY growth.

US Manufacturing: Massive CAPEX in Texas (10GW) and Indiana to capture $IRA 45X tax credits. This is "Made in America" with global expertise.

4/ Valuation Snapshot (2026 Metrics) 📊

The disconnect between fundamental value and stock price is staggering:

Market Cap: ~$1.24B

Enterprise Value (EV): ~$5.74B

Net Debt (ex-Leasing): ~$4.5B (Strategic leverage for US expansion)

2026e EBITDA: ~$720M

SOTP Valuation:

Based on their 62% stake in the Shanghai-listed subsidiary alone, the equity value should be ~4x higher than the current NASDAQ price.

5/ Earnings Reality Check 📉

Q4 2025 was a "kitchen sink" quarter. Negative margins at Recurrent Energy due to project delays and impairments masked the core strength.

The Rebound:

2026 is the "Transformation Year." As US factories hit full scale, we expect a massive margin expansion from 10% toward 15%+.

6/ Peer Group: The Value Gap 🥊

First Solar $FSLR: Trades at a premium (~9x EV/EBITDA) due to US-only focus.

JinkoSolar $JKS: Pure-play China risk.

$CSIQ: The "Deep Value" hybrid. Trading at ~6x Forward EBITDA despite having a superior battery storage pipeline.

7/ The 2030 Vision: A $2B+ EBITDA Powerhouse 🚀

By 2030, $CSIQ is projected to be a diversified utility-scale giant:

IPP Strategy: Currently operating ~1.1 GWp of own assets. The roadmap targets a massive scale-up to 10 GWp+ by 2030.

Est. Revenue: $16B | Est. EBITDA: $2.24B

Drivers: Recurring revenue from the IPP portfolio and dominance in the US stationary storage market.

8/ The "Musk Factor": A Sector-Wide Validation 🦾

The industry is buzzing after reports (March 2026) that Elon Musk's Tesla is in talks to buy $2.9B worth of solar manufacturing equipment from Chinese firms to scale US capacity.

Strategic Alignment: Musk is doubling down on "Amazing Abundance," aiming for 100 GW of US solar capacity.

Validation: $CSIQ is already ahead of this curve, executing exactly what Tesla is now scaling: sourcing the best tech to build massive US-based energy infrastructure.

9/ Opportunities vs. Risks ⚖️

✅ Upside: Massive $IRA tax credits, global storage boom, and "SOTP" re-rating.

⚠️ Downside: Geopolitical tensions (US/China), high interest rates affecting project finance, and module oversupply.

10/ The Bottom Line 🏁

$CSIQ is currently priced for a "worst-case" scenario, ignoring the exponential growth of its e-STORAGE division and US-based manufacturing alpha.

If they execute their 2027/2030 targets, the current valuation will look like a historical anomaly.

Disclaimer: Not financial advice. Always do your own DD.

https://t.co/jtjJEawzyb

#Solar #Renewables #Investing #CleanTech #CSIQ #EnergyStorage #StockMarket

THE SLEEPING GIANT OF EMERGING MARKETS? 🌍💳 Deep Dive into dLocal $DLO

After yesterday’s blockbuster Q4 2025 earnings, it’s time to look under the hood of the Uruguayan payment powerhouse. Is the "Emerging Markets" discount justified, or are we looking at a generational entry point?

1. The Company: Bridging the Gap

a) Company: dLocal isn’t just a payment processor; it’s the operating system for the "Global South."

They enable giants like Amazon, Meta, and Google to accept 900+ local payment methods across 44 countries in LATAM, Asia, and Africa.

b) Shareholders: Strong "Skin in the Game." Founders Andrés Bzurovski & Sergio Fogel hold significant stakes. Tier-1 backers like General Atlantic, D1 Capital, and Tiger Global remain on board, despite recent repositioning.

c) Evolution: From a niche Latin player to a global fintech contender. They’ve moved from just "handling payments" to a full-stack ecosystem (Stablecoins, BNPL, Treasury).

2. Product Excellenced

Local’s "One dLocal" API is their moat. It solves the complexity of fragmented regulations and local currencies.

• Stablecoins: New fiat-to-stablecoin on/off-ramps for faster treasury movements.

• Fuse (BNPL): Live in 6 countries, driving higher conversion for merchants.

• AI-Driven: Using proprietary models for fraud detection and smart routing, resulting in +7% productivity gains.

3. Valuation Snapshot (as of March 19, 2026)

The numbers tell a story of a massive valuation disconnect:

• Market Cap: ~$3.46B

• Enterprise Value (EV): ~$2.67B (reflecting a massive cash pile)

• Net Debt: Negative (Cash-rich balance sheet; Net Debt/EBITDA < 0)

• 2025 Adj. EBITDA: $278M

• EV/EBITDA (2025): ~9.6x (extremely low for >40% growth)

4. Earnings Snapshot (FY 2025)Record-breaking across the board:

• TPV: $40.8B (+60% YoY)

• Revenue: $1.1B (+47% YoY) – The first time crossing the $1B mark!

• Net Income: $197M (+63% YoY)

• Shareholder Returns: $300M Buyback authorized + $57.2M Dividend declared.

5. Peer Group Comparison

While $DLO trades at ~10x EV/EBITDA, peers like Adyen $ADYEY or Stripe $Stri (private) often command 25x-40x. Even StoneCo or PagSeguro trade at higher multiples despite more localized focus.

dLocal offers the growth of a high-tech processor at the price of a value stock.

6. Forecast 2030: The 4.2 Trillion Opportunity

The management is thinking long-term.

• TAM: Expected to grow from $2.1T (2025) to $4.2T by 2030.

• Market Share: Currently <2%. If they hit 5% by 2030, we are looking at a $200B+ TPV company.

• 2026 Guidance: TPV target of $58B - $62B with an Operating Profit of $280M - $320M.

7. Risks & Opportunities

🔴 Risks:

• Currency volatility in markets like Nigeria/Argentina.

• "Take Rate" compression as they onboard larger Tier-0 merchants.

• Past short-seller noise still affecting sentiment.

🟢 Opportunities:

• AI-integration driving "invisible" infrastructure efficiency.

• Massive expansion in Africa & Asia (APAC is the next frontier).

• Valuation re-rating once the "Emerging Markets" stigma fades.

8. Conclusion

dLocal is a high-growth machine trading at a value multiple. With a $300M buyback and a $57M dividend, the management is screaming that the stock is undervalued.

If they execute on the 2026 Operating Profit guidance, the current price will look like a steal in retrospect.

Disclaimer: Not financial advice. Mining is high risk. Always do your own DD.

#dLocal #Fintech #Earnings #EmergingMarkets #Investing $DLO #Payments

The $TBLD Thesis is Playing Out: FY 2025 Audited Results Confirm the Inflection Point 📈

1/ The "Survival" Phase is Officially Over.

The FY 2025 results are out, and they didn't just meet expectations—they beat them.

Revenue hit $35.5M (+17% YoY) and, most importantly, Adjusted EBITDA swung from a $6.1M loss to a $5.6M profit. The "Turnaround" isn't a forecast anymore; it’s an audited fact.

2/ Margin Expansion via IP Sovereignty.

The strategy shift I mentioned is visible in the data: 86% of Gaming Revenue now comes from Own-IP (up from 77%). By owning the underlying rights to hits like Deadside (which crushed it on console) and The King is Watching, tinyBuild is keeping the lion's share of every dollar earned.

3/ The Back-Catalogue is an "Evergreen" ATM.

88% of gaming revenue came from the back-catalogue. While the market chases "hits," $TBLD is printing cash from a portfolio of 100+ titles.

Hello Neighbor remains a powerhouse, and the expansion into a Season 3 Animated Series + Movie is turning a game studio into a multi-media franchise machine.

4/ Efficiency & Clean Sheets.

Management has been ruthless with cost discipline. G&A expenses are down, and the disposal of Red Cerberus (QA business) has successfully streamlined the group to focus on high-margin publishing.

Net Cash sits at $4.6M with zero debt. The balance sheet is "lean and mean" heading into the 2026 super-cycle.

5/ The "Steam Top 200" Dominance.

This is the "Alpha" signal: tinyBuild now has a record 7 titles on the Steam Top 200 Wishlist.

Kingmakers (The medieval-with-guns viral sensation)

Streets of Rogue 2

RESTORY (200k+ wishlists in 1 month)

The Lift (300k+ wishlists)

The pipeline isn't just "large"—it is statistically high-probability.

6/ Valuation:

The Market is still Sleeping.

Despite beating expectations and proving profitability, the valuation remains disconnected from the fundamental "Option Value" of the 2026 pipeline.

You are essentially paying for a stable, profitable back-catalogue and getting Kingmakers and Hello Neighbor 3 for a symbolic price.

7/ The Verdict.

2025 was about stabilizing the ship and proving the unit economics. 2026 is about the payload. With a record wishlist count and a proven profitable base, the risk/reward skew here remains one of the most asymmetric in the entire Small-Cap Gaming sector.

Disclaimer: Not financial advice. Always do your own DD. $TBLD #Gaming #Stocks #SmallCap #ValueInvesting #Kingmakers

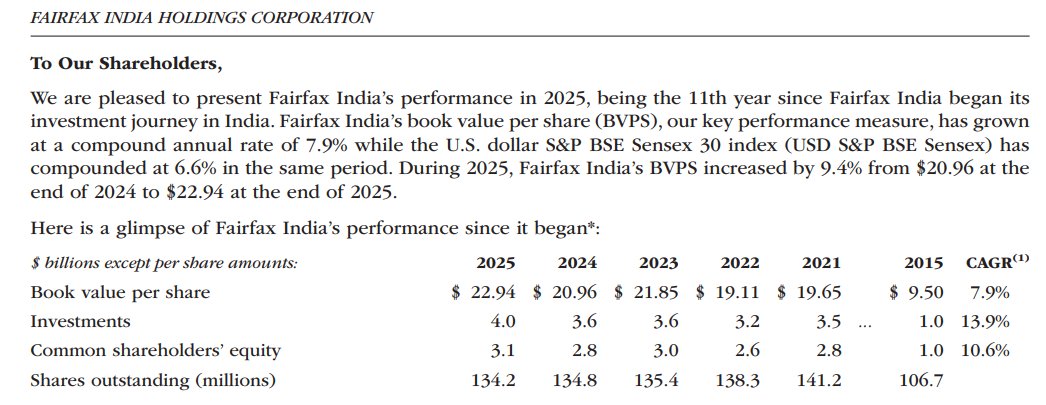

DEEP DIVE: Why Fairfax India Holdings $FIH-U.TO / $F5X is the Ultimate Gateway to India’s Economic Engine 🇮🇳

If you want exposure to the world’s fastest-growing major economy, you can buy a Nifty 50 ETF—or you can invest alongside Prem Watsa (the "Canadian Buffett") in a vehicle that owns the literal "toll booths" of Indian growth.

Here is my full breakdown of Fairfax India Holdings Corp. 🧵👇

1️⃣ The Company: A Permanent Capital Vehicle

Founded in 2015, Fairfax India is a Toronto-listed investment holding company $FIH.U / $FFXDF.

Unlike private equity funds with 10-year lifespans, Fairfax uses permanent capital. This allows them to hold high-moat, "generational" assets without the pressure to sell, compounding value at an 8-10% BVPS CAGR since inception.

2️⃣ The Portfolio: A Who's Who of Indian Infrastructure

The portfolio is a surgical strike on the Indian middle class and infrastructure:

Financials: Deep stakes in IIFL Finance, CSB Bank, and IIFL Securities.

They are riding the "financialization of savings" wave in India.

Industrial/Logistics: Seven Islands Shipping (crude/product tankers) and Maxop (precision engineering).

Agri: NCML, India’s leading private sector agriculture player.

3️⃣ The Crown Jewel: Bangalore International Airport (BIAL) ✈️

BIAL is not just an airport; it’s a high-growth monopoly. Fairfax owns 74% of Kempegowda International Airport (BLR).

The Moat: A concession agreement until 2068.

The Potential:

Bengaluru is the "Silicon Valley of India."

BIAL recently opened Terminal 2, increasing capacity to 50M+ passengers.

Real Estate Play:

They own ~460 acres of unutilized land around the airport. Think "Airport City"—hotels, tech parks, and retail.

IPO Catalyst:

The IPO for the airport holding vehicle (Anchorage) is slated for September 2026. This will be a massive "re-rating" event, likely valuing the airport far above its current book value.

4️⃣ Valuation Snapshot (As of March 10, 2026)

Despite the quality, the stock trades at a persistent discount to its intrinsic value.

Market Cap: ~$2.32 Billion

Book Value Per Share (BVPS): ~$22.94 (End of 2025)

Current Share Price: ~$17.30 (Trading at a ~25% discount to Book!)

Net Debt (ex-Leasing): ~$448 Million

EV / EBITDA: ~5.3x (Extremely low for a high-growth infrastructure play)

5️⃣ Earnings Snapshot (FY 2025 Highlights)

Net Earnings: $410.5 Million (A massive swing from the 2024 loss).

EPS: $3.05 (Diluted).

Performance: BVPS grew 9.4% in 2025, outperforming the USD S&P BSE Sensex (6.6%).

6️⃣ Peer Group Comparison

When compared to other India-focused vehicles or global infrastructure holdcos:

P/E Ratio: FIH.U (5.8x) vs. Peer Average (13.8x).

Price/Book: FIH.U (0.75x) vs. Indian Financial Peers (2.5x+).

The market is pricing Fairfax India like a stagnant holding company, while its underlying assets are growing at 15-20% YoY.

7️⃣ The 2030 Forecast 🔮

By 2030, India is projected to be the world's 3rd largest economy.

BIAL Valuation: Could easily double as passenger traffic hits 80M.

Exit Strategy: Expect Fairfax to start monetizing mature assets (like IIFL) to buy back shares or pivot into green energy/tech.

BVPS Target: If they maintain their 8% CAGR, BVPS will exceed $33.00 by 2030.

If the discount to book closes, we are looking at a $30-$35 share price.

8️⃣ Opportunities vs. Risks

✅ Opportunities:

-Closing the "Holding Company Discount."

-The 2026 Airport IPO.

-Share buybacks (they have been aggressive at these levels).

⚠️ Risks:

-Currency: Rupee (INR) depreciation against the USD.

-Regulatory: Changes in Indian tax laws or airport tariff structures.

-Concentration: Over 50% of value is tied to one airport.

9️⃣ Conclusion

Fairfax India is a "Buy and Forget" stock for the next decade. You are buying a world-class airport and a basket of India's best private companies at 75 cents on the dollar.

The 2026 IPO of BIAL will be the "Big Reveal." Don't wait for the market to realize what Prem Watsa already knows.

Disclaimer: Not financial advice. Always do your own DD. Mining (of data/value) is high risk.

#Investing #India #FairfaxIndia #ValueInvesting #Stocks #BIAL #Growth #EmergingMarkets #PremWatsa