Active developer who got tired of banks, partnered with a private lender, and now sees both sides of every deal.

I used to think private money was for people who couldn't get bank financing.

Then a "cheap" bank loan took 5 months to close. The market turned before I could exit.

That "cheap" money cost me more than any hard money loan ever would have.

Now I quote hard money deals.

Still building, still learning, still wrong sometimes.

This account is everything I wish someone had told me when I started.

Real deals. Real numbers. Real talk. Anonymous for now. Honest always.

Closed a spec loan for a family company doing high-end custom builds. Larger than their usual play, liquidity timed a little tight, market conditions made underwriters nervous. But the work is impeccable and the deal math was really good. Sometimes you just lean on the fundamentals and get it done. Sitting down with them yesterday to celebrate, that part meant a lot.

@Travisjost1 I empathize. I spent my entire day trying to explain to them why an unincorporated county does not produce conventional certificates of occupancy.

People think an architect’s job is to draw lines.

The real value is getting you to understand what you actually want and need.

A good architect will talk you out of something you thought you wanted and turn it into something better. That clarity is worth more than the drawings.

Premade plans skip that process entirely.

Just got back from a build expo.

Slow show. Most booths were quiet. Easy to check out mentally.

We made 2 great connections.

These shows aren't just networking. They're the fastest way to sharpen your knowledge on the products you sell. Keep your energy up even when the floor is dead. You never know who's about to walk through that door.

A city changes when builders, founders, and operators suddenly have liquidity.

Capital formation is often a better proxy for economic prosperity than population growth.

That’s when the next generation of companies, neighborhoods, and institutions gets funded.

@mikesimonsen Agree. Didn’t think about the prop 13 angle. My family owned a property in SF for a long time and always though of it as a blessing hahaha.

In Alamo Heights in particular zoning is a big part of why. SF-A and SF-B zoning. Minimum 7,500-8,400 sqft lots. FAR capped at ~0.45. No subdivision. Lot coverage maxed at 40%. Those rules don't just shape what gets built. They compress supply and create a scarcity premium. Buyers in Alamo Heights aren't just buying land. They're buying the guarantee that nobody redevelops the lot next door into something that doesn't belong. Zoning as a moat. Underrated value driver.

Easy trap in this business:

One or two groups give you consistent volume. The pipeline feels steady. The calls slow down. The outreach stops.

Concentration in one client feels like reliability... Until it doesn't.

When that group pulls back, so does your book.

Keep calling. Keep outreaching. Even when you don't need to.

Especially when you don't need to.

Three things everyone looks at on every hard money deal:

Property value. Sponsor experience. Liquidity.

The ideal is all three.

But two strong ones closes most deals.

Strong value + liquidity: we can work with a first-timer.

Strong experience + liquidity: we can work with a tough market.

Strong experience + value: we can work with tighter reserves.

The mistake most borrowers make is assuming experience alone is enough.

The mistake most lenders make is assuming value alone is enough.

At least two out of three.

Always liked retail over SFR. A couple of years after moving to the US, LP’d into a strip mall in Houston, then two more plazas in San Antonio.

The hardest part was finding the right GP and getting in front of the right information.

That kind of access used to take years and the right handshake. Still does for most people.

@connorclift35@Jacob_Naviaux 75% LTARV is already disappearing for us. Had to fight hard to get it approved for a client we’ve done 10+ deals with over the last 2 years in a market we are very familiar with.

Experience used to unlock leverage. Now it’s barely holding it steady.

The best deal I’ve ever seen was a very ugly and depleted RV park. Utilities were provided by the owner (tenants paid a flat fee) and he made a ton of money renting divided shipping containers as storage units. The place was dirty with a caliche stone road but it was a cash flow machine.

Quiet story. Massive implications for private lending specifically.

Some of the largest capital partners behind non-balance sheet RTL lenders source institutional money from Japan. Churchill Real Estate is a prime example.

The chain matters:

Japan rates rise → capital repatriates → warehouse lines to hard money lenders get more expensive → RTL rates reprice → borrowers feel it 60-90 days later.

The 2Y already crossed 4% this week. The hard money market is downstream of all of this.

Most borrowers aren’t watching this yet.

Quiet story. Massive implications for private lending specifically.

Some of the largest capital partners behind non-balance sheet RTL lenders source institutional money from Japan. Churchill Real Estate is a prime example.

The chain matters:

Japan rates rise → capital repatriates → warehouse lines to hard money lenders get more expensive → RTL rates reprice → borrowers feel it 60-90 days later.

The 2Y already crossed 4% this week. The hard money market is downstream of all of this.

Most borrowers aren’t watching this yet.

@jonbrooks This tracks from our office.

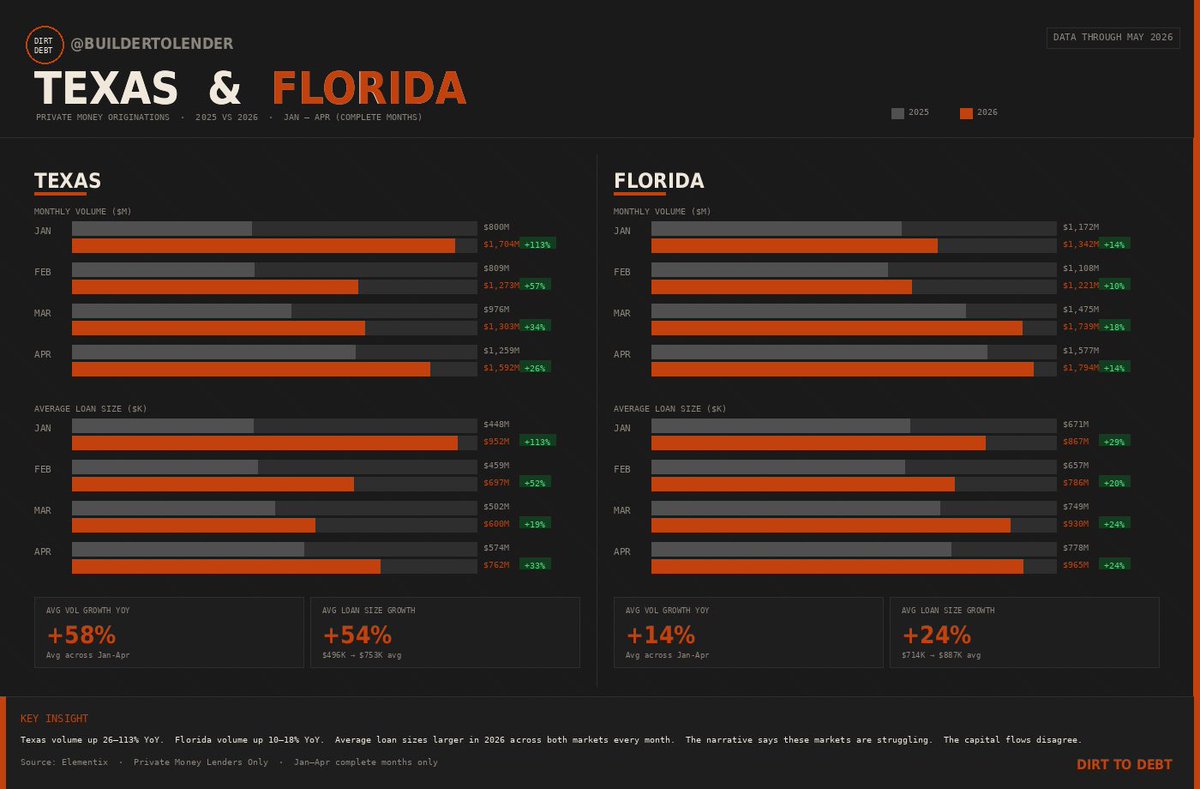

Our two main markets are Texas and Florida. Private money volume is up 58% and 14% YoY respectively. Average loan sizes up 54% and 24%.

The clients cycling fastest on our book? The luxury ones.

The deals getting approved easiest? The bigger ticket.

Capital partners are agreeing.

Townhome product in DFW is moving well. Easier to approve right now than most other Texas markets/products.

The two easiest deals we’ve approved in Texas this year? Highland Park adjacent new builds in Oak Lawn.

The numbers pencil. The exits are cleaner. The demand is real.