Bitcoin gave me an epiphany.

Money isn't just money.

It's stored time.

Every time you go to work, you're exchanging a piece of your life for money.

An hour. A day. A year.

Your salary is simply your time converted into a monetary form.

When you don't spend that money, you're doing something remarkable.

You're storing your time.

You're choosing to use a piece of your life's work in the future instead of today.

Savings are stored time.

That completely changed how I think about inflation.

Inflation isn't just prices going up.

It's your stored time buying less than it used to.

If it took you 100 hours of work to build your savings...

...and years later those savings buy significantly less...

Then those 100 hours of your life no longer command the same value.

That's a sobering thought.

This isn't about greed.

It's about respect for your time.

Your time is the one asset you'll never get back.

Good money should preserve the value of that sacrifice as well as possible.

Whether you choose Bitcoin, property, equities, or something else...

The question I now ask is simple:

"Does this help preserve the value of my stored time?"

Bitcoin didn't just change how I invest.

It changed how I define wealth.

Not as pounds or dollars...

But as the ability to preserve the value of my life's work into the future.

What do you think?

Is money just money?

Or is it really stored time?

@LanternBitcoin Very interesting Scott. I’ve recently purged the list of people I’ve been following on X & found it liberating. Peace restored 🙏🧘♂️

Sovereign Sessions launches in August. This will be the new home for ALL my tutorial content.

If you want practical step by step instructions on Bitcoin, self hosted AI, privacy and sovereign computing, follow @SOVsessions and subscribe on YouTube here👇

https://t.co/k4Ajw12qNd

Starting in 2026, the "exit" from Bitcoin isn't Dollars.

It's Digital Credit.

Wealthy holders rotate BTC → digital credit → spend the yield → issuers buy more BTC.

Selling pressure becomes buying pressure. This may be the most bullish setup in Bitcoin's history.

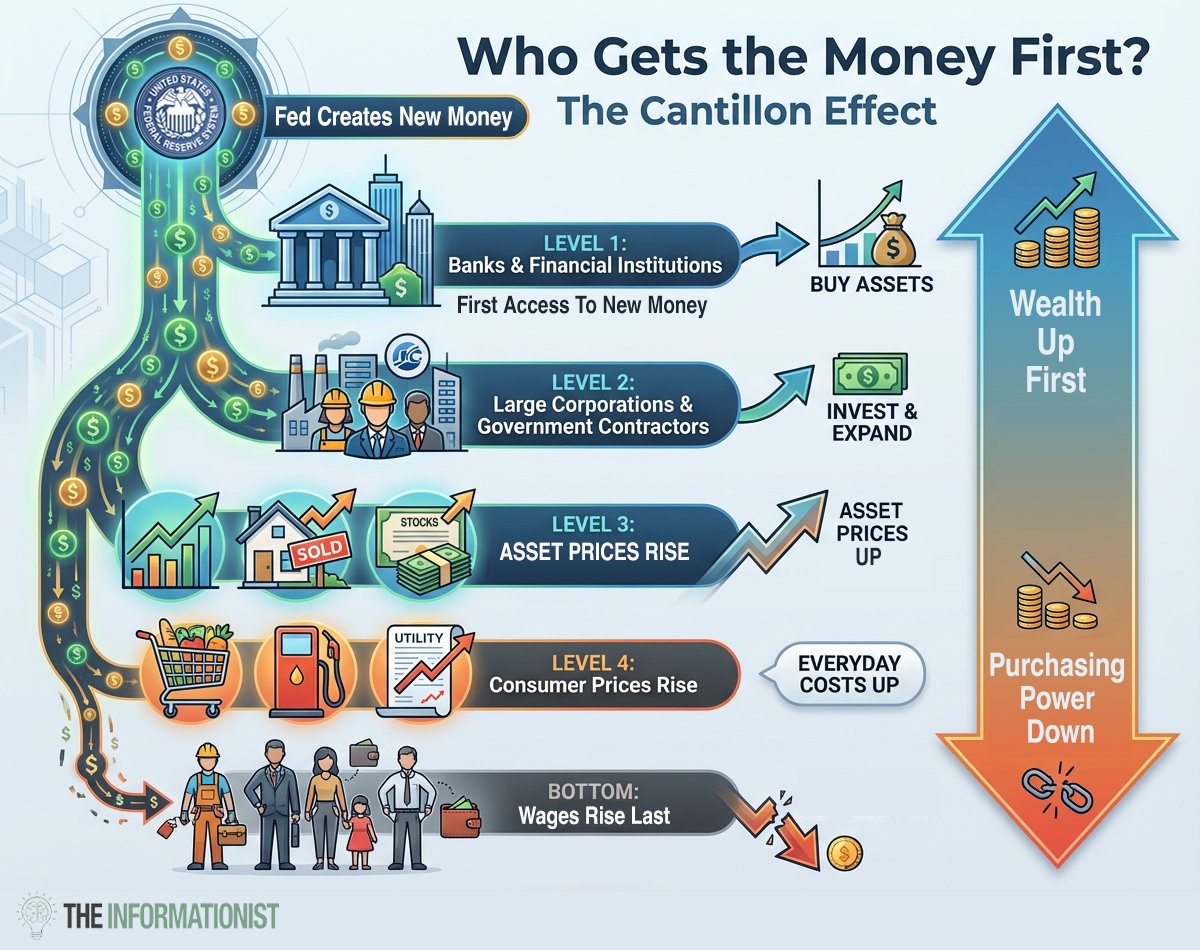

Most people have never heard of the Cantillon Effect.

But once you understand it, you’ll see the world of investing differently.

What is it?

In the early 1700s, Richard Cantillon noticed a simple pattern:

When new money enters an economy, it doesn’t reach everyone at once.

And whoever gets it first benefits the most.

Here’s how it works today:

New liquidity enters through the Fed and through bank lending.

Both follow a similar pattern:

→ Markets and large balance sheets get first access

→ Large corporations and well-connected borrowers tap cheap credit next, they invest and expand at today’s prices

→ Asset prices tend to rise as new liquidity chases finite assets

→ Consumer prices often follow

→ Wages rise last, usually after purchasing power has already declined

Fed data shows how lopsided the playing field is:

- The top 10% hold nearly 90% of equities.

- The bottom 50% holds about 1%.

It’s a simple but powerful monetary transmission.

Understanding this won’t change the system.

But it might change how you think about where to store your savings.

For those of you who don't know, I write all about topics like this every week in The Informationist. Last week, we dove deep on this one.

Link in bio if you want to read the full explanation.