From Li Lu's book:

At the beginning of the new year in 2016, I watched the movie "The Big Short". Adapted from the novel of the same name by Michael Lewis, the film tells the legendary story of the few investors who first discovered the 2007-2008 subprime mortgage crisis and the loopholes in the entire financial system of the United States, and started shorting to profit. I have personally experienced many of the events involved in the film; I have more or less intersected with the various characters in the film, so watching it gives me a more immersive sense of reality, which also triggers some thoughts.

From 2005 and 2006, I personally discovered the product of credit default swaps (CDS) due to accidental reasons. After doing some research, I was also planning to enter on a large scale and sell short through CDS. Later, after several conversations with Charlie Munger, this idea was gradually dispelled. The reason for Charlie’s objection is also very simple: if my analysis is correct, it means that in the end, either the counterparty of these products, those large financial companies may not be able to cash out due to bankruptcy; or these large financial institutions are approved by the government. The taxpayers' money has been saved. At this time, the money you earn is actually taxpayers' and government's money, so you are not at ease. Later, the results really confirmed Charlie's judgement. The money earned from the largest short position in history was actually obtained directly or indirectly from taxpayers around the world. So I have never regretted not earning taxpayer money.

Investment itself is a prediction of the future. Although the prediction is correct, it will bring some pleasure to some extent, but the results of different ways of making money are still different. Later, after the publication of this book by Michael Lewis, I had several exchanges with Charlie and talked about the decision at that time. He said that if you made a lot of money doing CDS at that time, you may still be looking for a new CDS today. A big short opportunity. Human nature is like this.

1.1. Question 28: What happened 1973 and 1974 when your investment firm lost over half?

Charlie: Oh, that’s very simple. That’s very easy. That’s a good lesson. That’s a good question. What happened is the value of my partnership where I was running, went down by 50% in one year. Now the market went down by 40% or something. It was a once in 30 year recession. I mean monopoly newspapers are selling at 3 or 4 times earnings. At the bottom tick, I was down from the peak, 50%. You’re right about that. That has happened to me 3 times in my Berkshire stock.

so I regard it as part of manhood. If you’re going to be in this game for the long pull, which is the way to do it, you better be able to handle a 50% decline without fussing too much about it. And so my lesson to all of you is conduct your life so that you can handle the 50% decline with aplomb and grace. Don’t try to avoid it. (applause) It will come. In fact I would say if it doesn’t come, you’re not being aggressive enough.

1.2.

“I regard it as a part of manhood. If you’re going to be in this game for the long haul which is the way to do it. You better be able to handle a 50% decline without fussing too much. Conduct your life so you can handle a 50% decline with aplomb and grace. Don’t try to avoid it. It will come. And if it doesn’t come I’d say your not being aggressive enough”.

Some notes about Buffett, Munger, and people they encountered:

- Over a lifetime, you'll get a reputation for either bluffing or not bluffing. I want it to be understood that I don't.

- Munger: "Phil, you have to practice the law the way my father did, by trusting a man's word."

- Miss B: Sell cheap and tell the truth, don't cheat anybody, and don't take no kickbacks.

- Kiewit: If you're not sure if something is right or wrong, consider whether you'd want it reported in the morning paper.

- On money to his children: Enough money so that they could do anything, but not so much that they could do nothing.

- A friend: Warren is the master of win/win... but he never does anything that isn't a win for him.

- It takes a lifetime to build a reputation and five minutes to ruin it.

- Rule number one, don't lose money. Rule number two, don't forget rule number one.

- Buffett on LTCM: They thought they had the time to play the hand out.

- If you keep betting long enough, sooner or later, as long as a zero was not impossible, someday a zero was 100% certain to show up.

- You absolutely never want to be in the position where tomorrow morning you have to depend on the kindness of strangers in the investment world.

-You can always tell someone to go to hell tomorrow.

Berkshire isn’t exactly just a passive shareholder. Through BHE they’re also one of the largest energy providers Google depends on to run its data centers. So they’re getting equity upside on Google’s AI growth and regulated utility returns on the power Google needs to actually do it. It’s like Berkshire is vendor financing Google’s energy demand.

The valuation pushback is fair. But this investment isn’t just a stock pick. It’s putting Berkshire’s energy assets right in the heart of the nation’s AI infrastructure build.

$SPGI … not very often do you get the chance to buy this quality business at a 5% FCF yield and 21x NTM EPS.

In their latest 13Fs:

• Chris Hohn (TCI) added over 2 million shares (~8% allocation)

• Li Lu initiated a new position with ~121K shares (~1.6% allocation and is likely to add more)

• Pat Dorsey initiated a new position with over 220K shares (~7.5% allocation)

___

“But but … Market Intelligence will get disrupted.”

Okay, if we assume Market Intelligence goes to $0, $SPGI still trades 26x LTM Ratings + Indices Operating Income (assuming Energy segment is at $0 as well)

“But but … management has made questionable acquisitions in the past.”

Fair, and now management is spinning off Mobility (lowest margin segment) and focusing on its highest quality assets

“But but … the stock practically went nowhere since the end of 2021.”

The real story is multiple compression. At the end of 2021, $SPGI traded at 34x NTM. The flat price action since then has been almost entirely valuation-driven. Moving forward, that severe multiple contraction is unlikely to repeat as a drag on future returns. So, shareholders today are well positioned to capture the full earnings growth plus potential margin expansion as Mr. Market comes to his senses and realizes it overshot on the downside

“But but … have insiders been buying?”

Yes.

Ex-Tiger Cub at Julian Robertson's hedge fund - turned $200M into $36B in 8 years, then lost it all in 2 days

- he was the greatest trader you've never heard of, hiding $160B in positions through swaps so Goldman, Morgan Stanley, Credit Suisse never saw his real size

Bill Hwang's Archegos blew up so hard it took down Credit Suisse, cost banks $10B, and erased $100B in market cap

16min documentary about the biggest individual loss in modern financial history

bookmark - it's The Most Spectacular Implosion on Wall Street

Nvidia paid $6.01 per share for 2.9% of $NOK in October. Nokia is now at $9.55

I was at GTC and met with some of the Nokia exec team. What they described changes how you think about what a cell tower actually is.

Jensen Huang called it "Robotic AI Radio." The idea is simple: a factory robot cannot wait 200 milliseconds for a cloud server to process its next move. So instead of sending that data back to a centralized data center, you run the inference directly at the cell tower. Every tower becomes a distributed AI compute node. $NOK is deploying $NVDA RTX PRO 4500 Blackwell GPUs directly into its AI-RAN base stations to make this possible, running on $DELL PowerEdge servers. $TMUS was the first US carrier to pilot it.

There are roughly 100,000 distributed network sites worldwide with enough spare capacity to add over 100 gigawatts of new AI compute over time. Nokia is the western vendor building the software stack that runs on top of Nvidia's hardware to make those sites intelligent.

Nokia's acquisition of Infinera gave it 800G ZR coherent pluggables at exactly the moment hyperscalers started treating optical backbones as AI infrastructure, not telecom infrastructure. $CIEN is seeing the same demand and just guided $5.7 to $6.1 billion in revenue for fiscal 2026, up nearly 24%. $NOK Optical Networks grew 17% in Q4 2025, with €2.4B in hyperscaler orders for the full year. Management is targeting €3.1 to €3.7B in operating profit by 2028, up from just over €2B in 2025. The RAN market alone is projected to reach $200B by 2030.

Nvidia did not buy into Nokia because they needed the equity exposure. They bought in because they needed the distribution.

최소 2030년까지 돌고도는 AI 병목정리

L0 ㅡ Permitting + 숙련 노동

돈·자원 다 있어도 인력·허가 없으면 무의미

$PWR, $MTZ, $STRL, EME

L1a ㅡ 변압기·Switchgear

2~3년 리드타임, copper 의존

$GEV, $ETN, HUBB

L1b ㅡ 구리·전기

메탈L1a의 원재료 + 모든 인프라 공통 인풋

$FCX, $SCCO, TECK

L1c ㅡ Cooling (Liquid/Air)

전력 밀도 폭증 → 필수, 전력과 양의 피드백

$VRT, $MOD, $ETN, $FIX, $AAON, CLS

L2a ㅡ Compute / AI Accelerators & Server CPU

(GPU+CPU, 가장 근본적·순환 병목)

$NVDA , $AMD, $INTC, $TSM, $AVGO, ARM

L2b ㅡ HBM , Memory

L2c와 결합돼야 의미, sold out 2026

$MU, $SNDK, $WDC, $LRCX, $RMBS, AMKR

L2c ㅡ CoWoS 패키징 / 반도체

backend의 진짜 좁은 파이프

$TSM, $AMKR, ASX

L2.5 ㅡ Neo Cloud/AI 인프라

$IREN, $NBIS, $CRWV, $CIFR, APLD

L3 ㅡ On-site Power 발전

그리드 우회, 즉시성 측면 강력

$BE, $CEG, $VST, GEV

L3.5 ㅡ SMR / 차세대 원전

2030년 이후 게임체인저, 지금은 기대감

$OKLO, $SMR, BWXT

L4 ㅡ Photonics / Optical Interconnect

Cluster scale-out 필수, 전력 절감 효과

$LITE, $COHR, $CRDO, $AAOI, $LWLG, $AEHR, MRVL

L5 ㅡ 희토류·영구자석

지정학 리스크 + 로보틱스 본격화 시 폭발

$MP, $USAR, $CRMA, UUUU

L6 ㅡ 로보틱스 / 우주

위 모든 것 풀려야 본격적인 스케일

$TSLA, $NVDA, $ISRG, $TER, $SERV, $RKBL, $ASTS, PL

병목이라는게 순차적으로 발생하는게 아니고

진짜 핵심은 병목들이 어떻게 상호작용하는가임

병목은 단순히 "더해지는" 게 아니라 서로 곱해지고, 일부는 음의 피드백, 일부는 양의 피드백을 만듦

1. 직선 의존성 (A가 막히면 B도 막힘)

🔸Permitting → 전력 발전소/송전선 건설

🔸숙련 노동 → 모든 건설 (DC, 변압기 공장, 발전소)

🔸변압기/Switchgear → 전력 전달 → DC 가동

🔸CoWoS → GPU 생산 (HBM, 3nm 웨이퍼 준비돼도 무용지물)

🔸구리 → 변압기, 케이블, 모터 (모든 전력 인프라의 원재료)

여기서 중요한 게 "가장 느린 노드가 전체 속도를 결정"한다는 점임.

지금은 그게 변압기(2~3년 리드타임)와 숙련 전기공임

2. 양의 피드백 루프 (서로를 악화시킴)

이게 흥미로운 부분인데

Loop 1: 전력 ⇄ 냉각

액침/액냉 도입 → 랙당 전력 밀도 ↑ (50kW → 120kW+)

그러면 → 단위면적당 더 많은 전력 필�� → 전력 병목 악화

즉, 냉각 기술 발전이 전력 문제를 풀어주는 게 아니라 더 키우게 됨

◈VRT가 강한 이유가 이 dual-bind을 둘 다 잡기 때문

Loop 2: 숙련 노동 ⇄ 발전소 건설

전력 부족 → 발전소(가스, 원자력) 더 짓자

근데 발전소 건설에도 똑같은 전기공·용접공 필요

→DC와 발전소가 같은 인력 풀을 두고 경쟁

"데이터센터가 확장되는 동시에 유틸리티, 제조, 재생에너지, 그리드 인프라, 건설이 모두 같은 숙련 인력 풀을 두고 경쟁하고 있고, AI가 이 압력을 증폭"

Loop 3: 구리 ⇄ 모든 것

DC 1개당 구리 3~5배 → 구리 가격 ↑

변압기 가격 ↑ → DC 건설비 ↑

EV·재생에너지·로보틱스도 같은 구리 두고 경쟁

구리는 "공통 인풋"이라 영향력이 가장 광범위

3. 음의 피드백 루프 (자기조정)

Loop 4: 가격 → Capex → 완화 (2~3년 시차)

HBM/CoWoS sold-out → MU·SK Hynix·TSMC 대규모 capex

전력장비 백로그 → GEV·ETN 증설

단, 시차가 길어서 2027~2028년에야 효과

그 사이에 수요가 더 커지면 따라잡지 못함

Loop 5: Photonics → 전력 절감

광 인터커넥트가 구리 대비 전력 효율 ↑

클러스터 scale-out에서 전력 부담 일부 경감

LITE·COHR가 실제로 이 효과로 수요 폭발 중

4. 우회 루트

Off-grid power = 그리드 우회 (가장 핫한 트렌드)

BE(Fuel Cell), CEG(원전 PPA), VST(가스+원전), GEV(가스터빈)

이게 왜 지금 폭등하냐면

그리드 인터커넥션 5~7년 대기를 90일~2년으로 단축시킴

하지만 가스터빈 자체도 sold-out, 리드타임 3~5년으로 늘고 있음. 결국 또 다른 병목으로 이동

이런식으로 병목은 순차적으로 하나에만 영향을 미치는게 아니고

동시다발적이며 여러군데로 영향을 미침

이 흐름을 잘 숙지하고 있으면 앞으로 2030년까지는 계속 울궈���을수 있음

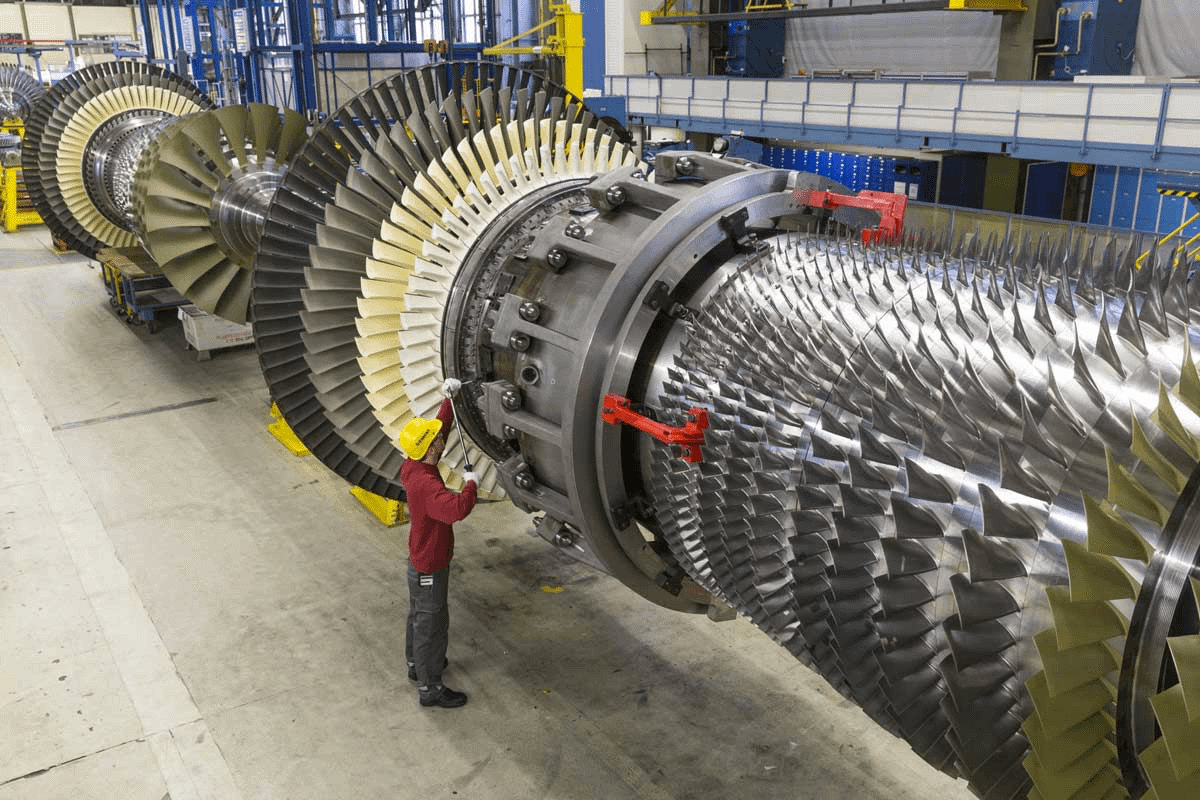

You cannot buy a new gas turbine until 2030. Order books at GE, Siemens, and Mitsubishi stretch to 2029. Turbine prices have nearly tripled since 2019. Every AI data center needs power and every gas plant needs a turbine. And every turbine has one part that bottlenecks the entire industry: The blade. It has to survive in gas 500°C above the melting point of the metal it's made from and spin at up to 20,000 RPM under 10,000 g of centrifugal force. Each blade is grown as a single crystal of nickel superalloy, pulled through a vacuum furnace at 3 mm per minute. A set of blades costs $600,000 and takes 90 weeks to grow. The same metallurgy powers modern jet engines. Only 3 companies on Earth can build one. China spent $42 billion trying to catch up. They bought a Russian fighter engine, took it apart, and copied every part. Their copy ran 30 hours between overhauls versus 400 for the original. Modern Western engines run 4,000. You can reverse engineer the shape of a turbine blade. You cannot reverse engineer 60 years of metallurgy.

Berkshire Hathaway director Chris Davis: "People matter a lot more than is generally realized. We have a society that believes in equality and is very quick to figure that the people who did well got lucky."

"They don't have the same feeling about basketball. Nobody looks at LeBron and thinks, 'I could do that.'"

"It is amazing what a difference one person can make at a business."

"There is a risk of hero worship, but I hate the opposite more. I hate this proclivity we have to tear down people who have built incredible businesses that employ tens or hundreds of thousands of people that provide services that delight their customers — and then we want to vilify their success. It's crazy."

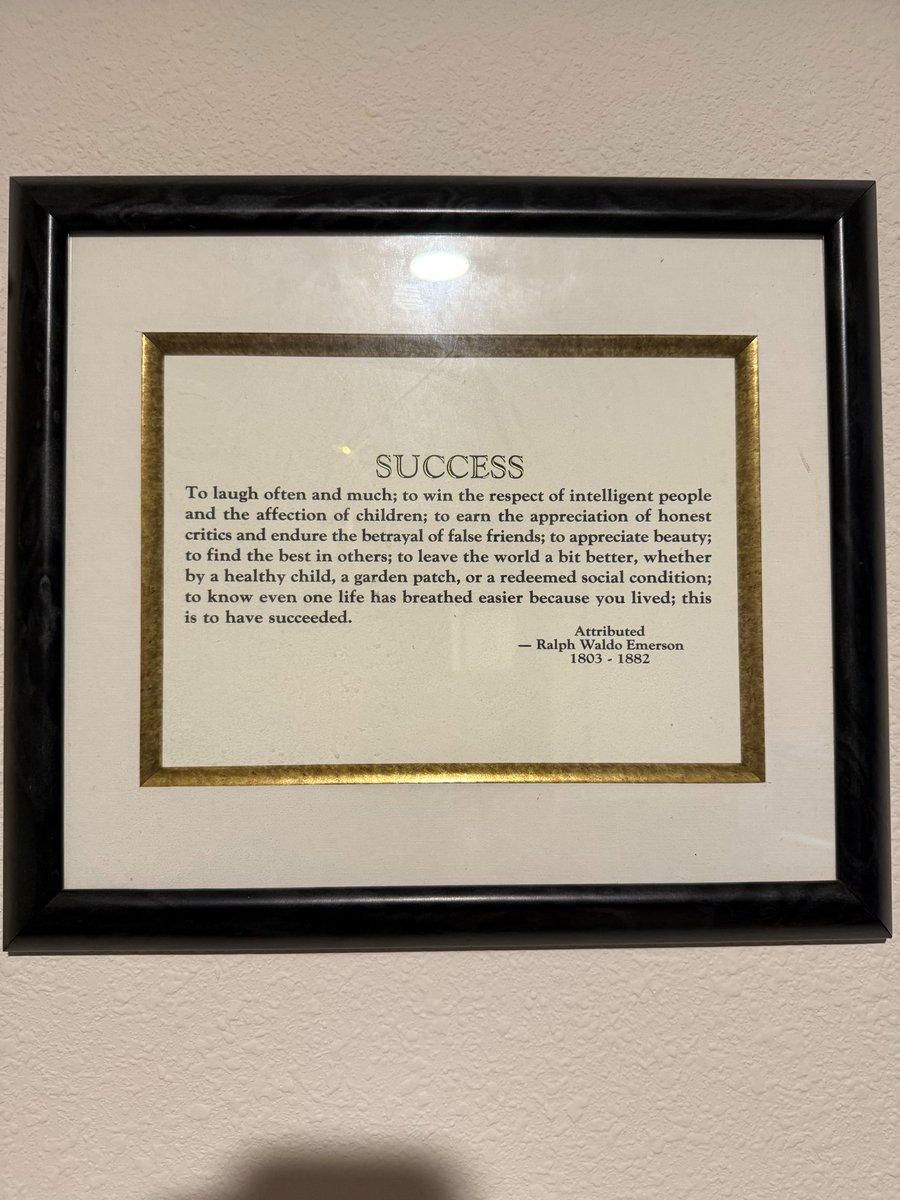

My father handed me a framed poem the day I graduated college. No watch. No check. A poem.

I didn't understand it yet. But I hung it in my cubicle at @HSBC, my first job out of my MBA program.

It was called "Success"—attributed to Emerson—and it said nothing about corner offices, stock options, or your name on a building.

It talked about laughing often. Earning the respect of honest critics. Leaving the world slightly less broken than you found it.

I read it every morning at my desk. The same desk where I watched a global bank choose profit over national security and expected me to stay quiet about it.

That poem became the most dangerous thing in my cubicle.

Because when you internalize a definition of success that has nothing to do with money or titles, you become very hard to control. You can't threaten someone's career when they've already decided their career isn't the point.

After I blew the whistle, I lost my job. I lost relationships. The bank paid $1.9 billion in fines.

At the time, I thought I had lost everything.

I actually gained everything.

Resilience. Courage. Integrity that no one can take from me. It made me a stronger person. And every company I've built since—every decision I've made—is rooted in that poem my father gave me.

My message to anyone starting their career: the focus is not making money. Make a significant positive difference. Try to leave the world a bit better. The money will follow.

There is a lot of evil out there. But I choose to focus on the positive. I see so many people—CEOs, leaders, everyday professionals—trying to do the right thing. And it is encouraging.

The right thing doesn't mean you have to blow the whistle on an international bank and stand up to terrorists and drug cartels.

It's the little moments.

Just focus on doing the next right thing. Baby steps.

My father gave me the answer key before I even knew the test was coming. He showed me what success actually looks like—and I hope this reminds someone out there that the things worth building are always worth the cost.

Success is knowing that even one life has breathed easier because you refused to look away.

That poem still hangs on my wall. Different office now. Same standard.

Want to understand why Brazil is the way it is?

You have to start at the beginning. And the beginning explains everything.

Portugal didn't colonize Brazil the way Britain colonized America.

There was no Puritan work ethic. No town hall democracy. No independent yeoman farmer building institutions from the ground up.

Portugal sent extractors. They came for sugar, gold, and wood. They built plantations, not communities.

The first economic model was extraction, not creation.

That DNA still runs through parts of the system 500 years later.

The country was named after a tree (pau-brasil), not a person. The land defined the nation before the nation defined itself.

From the beginning, Brazil's identity was shaped by what could be pulled from its soil. Sugar in the Northeast. Gold in Minas Gerais. Coffee in São Paulo. Rubber in the Amazon. Soybeans in the Cerrado.

The resource changed every century. The pattern stayed the same.

And the labor system that powered that extraction shaped everything that followed.

Over 4 million enslaved Africans were brought to Brazil across three and a half centuries. More than to any other country in the Americas.

Brazil was the last country in the Western Hemisphere to abolish slavery. 1888.

The social consequences of that system (inequality, informal labor, racial stratification, distrust of institutions) did not end with abolition.

They were baked into the economic structure and remain visible in every major city today.

That history also explains why Brazil's political transitions have always come from the top, not the bottom.

Brazil has never had a revolution that stuck.

Independence came through negotiation (the Portuguese prince declared independence from his own father).

The Republic came through a military coup that most citizens didn't know about until days later.

Every major political transition was brokered by elites, not won by the people.

Change in Brazil is gradual, negotiated, and incomplete. Institutions bend. They rarely break.

The same pattern played out with BCB independence, the tax reform, and the EU-Mercosul deal. The pace frustrates outsiders. But the direction holds.

Even the geography reflects this pattern of reinvention from the top.

The capital moved twice, and each move followed the money.

Salvador was built on sugar. Rio rose with gold and coffee. Brasília was constructed from nothing in 41 months in the middle of the Cerrado to force development inland.

The country keeps reinventing its own geography. MATOPIBA is the latest chapter in that same 500-year story of pushing economic frontiers deeper into the interior.

So where does corruption fit? It didn't arrive with modern politicians. It was the operating system from the beginning.

The Portuguese crown distributed land, titles, and trade monopolies based on loyalty, not merit.

The informal system (the "jeitinho") exists because the formal systems were built to serve elites, not citizens. When the law doesn't work for you, you find a way around it.

That impulse is Brazil's greatest friction for outsiders trying to navigate the system. It's also the greatest source of resilience for the people who live inside it.

Lava Jato didn't invent the corruption problem. It exposed a system that had been running for 500 years.

The fact that Brazil prosecuted sitting presidents, senators, and CEOs on live television (something most democracies have never attempted at that scale) was the break from history, not the continuation of it.

Which brings us to the skepticism.

The "country of the future" joke lands because Brazilians have heard promises from their own leaders for centuries.

Every new president, every new capital, every new economic plan came with the same speech about transformation.

The skepticism is earned. Brazilians are not pessimistic by nature. They are experienced. They've watched cycles of boom and bust repeat for generations.

The optimism of outsiders and the skepticism of insiders are both rational responses to the same history viewed from different distances.

So what does 500 years of history teach you about investing in this country?

Brazil's problems are institutional. Built by humans over centuries. Changeable (slowly) through reform, technology, and generational turnover.

Brazil's advantages are physical. Soil, water, sunlight, minerals, geography, biodiversity. Unchanged by elections, currencies, or corruption scandals.

Institutions improve over time. The physics of the endowment does not change.

The country with the most arable land on earth, 12% of the world's freshwater, 94% of global niobium reserves, 87% renewable electricity, and export routes through uncontested Atlantic waters will be worth more in 2075 than it is today regardless of who sits in the Planalto.

The history explains why Brazil is hard. The endowment explains why it's worth it.

Realism is the only edge that survives contact with the ground. And realism requires understanding where the country came from before you bet on where it's going.

For further reading, I recommend the book: "Brazil: A Biography" by Lilia M. Schwarcz and Heloisa M. Starling.

𝐓𝐡𝐞 𝐛𝐚𝐜𝐤 𝐝𝐨𝐨𝐫 𝐢𝐧𝐭𝐨 𝐆𝐨𝐥𝐝𝐦𝐚𝐧 𝐒𝐚𝐜𝐡𝐬.

𝐋𝐥𝐨𝐲𝐝 𝐁𝐥𝐚𝐧𝐤𝐟𝐞𝐢𝐧 grew up in the housing projects of East New York. His father was a postal worker.

He studied law. By his own admission, he knew nothing about Wall Street — hadn't taken finance, didn't read the WSJ, and couldn't get past the HR gatekeeper at Goldman Sachs.

So he went in the back door. Got a job at J. Aron, a commodities firm Goldman later acquired. He rose through the ranks, became CEO, and navigated the worst financial crisis in 80 years.

His new book 𝐒𝐭𝐫𝐞𝐞𝐭𝐰𝐢𝐬𝐞 is an enjoyable read. Four common themes I see amongst many of the successful businesses I've studied:

𝟏. 𝐘𝐨𝐮𝐫 𝐛𝐞𝐬𝐭 𝐢𝐝𝐞𝐚𝐬 𝐚𝐫𝐞 𝐚𝐥𝐫𝐞𝐚𝐝𝐲 𝐨𝐧 𝐭𝐡𝐞 𝐟𝐫𝐨𝐧𝐭 𝐥𝐢𝐧𝐞

The people closest to the business usually know how to fix it. They just wait for permission. Ask them what should be done — then tell them to do it.

𝟐. 𝐂𝐮𝐥𝐭𝐮𝐫𝐞 𝐢𝐬 𝐭𝐡𝐞 𝐮𝐥𝐭𝐢𝐦𝐚𝐭𝐞 𝐜𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐚𝐝𝐯𝐚𝐧𝐭𝐚𝐠𝐞

The Goldman partnership mentality — everyone an owner, long-term over short-term — was the firm's real edge. With the right culture, size becomes a strength, not a liability. But it requires active leadership. "It can't be just in words; it has to be in actions."

𝟑. 𝐓𝐡𝐞 𝐏&𝐋 𝐢𝐬 𝐲𝐨𝐮𝐫 𝐦𝐨𝐬𝐭 𝐩𝐨𝐰𝐞𝐫𝐟𝐮𝐥 𝐦𝐚𝐧𝐚𝐠𝐞𝐦𝐞𝐧𝐭 𝐭𝐨𝐨𝐥

Blankfein didn't always call meetings or give directives. He changed what people could see. Split the P&L and everyone has to stand on their own — accountability without a word spoken. Combine them and you give people room to take more risk. Visibility shapes behaviour faster than any instruction ever could.

𝟒. 𝐂𝐫𝐢𝐬𝐞𝐬 𝐚𝐥𝐰𝐚𝐲𝐬 𝐥𝐨𝐨𝐤 𝐰𝐨𝐫𝐬𝐞 𝐰𝐡𝐞𝐧 𝐲𝐨𝐮'𝐫𝐞 𝐢𝐧𝐬𝐢𝐝𝐞 𝐭𝐡𝐞𝐦 — 𝐬𝐭𝐮𝐝𝐲 𝐡𝐢𝐬𝐭𝐨𝐫𝐲

The present feels uniquely dangerous because it's unresolved. History is safely on the shelf. But Blankfein's point is sharp: we've navigated civil war, nuclear standoffs, assassinations, and social upheaval. We just forget. Studying history isn't an academic exercise — it's a practical reminder that humans have been here before and found a way through.

The path doesn't have to be linear. The front door isn't the only door.