It only looked stable until someone checked the timing.

Tesco was one of the most trusted retailers in Britain. That was part of the problem. When a business is huge, familiar, and deeply embedded in everyday life, people often assume the reporting must be solid too.

In 2014, that confidence cracked. Tesco announced that expected first-half profit had been overstated by £250 million, later revised to £263 million. The issue was not fake stores or invented customers. It was much more ordinary: booking money from suppliers too early and delaying costs.

That detail matters. Frauds like this often survive because they sit inside normal business activity. Supplier rebates, promotional payments, and commercial income are real. Move them into the wrong period, and weak performance can suddenly look acceptable.

The collapse did not begin with one dramatic leak. It came from internal concern, suspended executives, outside legal review, and then a Serious Fraud Office investigation. Once the timing was examined properly, the gap was too large to explain away.

That’s what makes this case memorable to me. Not how exotic it was, but how familiar it looked before the break.

Which kind of accounting scandal do you think is harder to spot: invented revenue or real revenue recognized at the wrong time?

If you want more breakdowns like this, follow for the next one.

#FinancialCrime #AccountingScandal #Tesco #CorporateFraud #ForensicAccounting #BusinessHistory #FraudCase #Markets

It starts looking different once the cash stops moving.

Banco Espírito Santo did not collapse because one headline scared the market. It collapsed because a web of family-owned companies had been using short-term debt, related-party funding, and weak internal controls for so long that eventually the numbers had to reconcile.

That turning point came in 2014. An audit at Espírito Santo International found accounting irregularities and hidden liabilities. Then missed debt payments exposed a simple truth: the group did not have the cash to support the promises already made.

What made this story dangerous was how credible it looked from the outside. BES was one of Portugal’s best-known banks, tied to one of its most powerful business dynasties. That reputation bought time, and in fraud stories, time is often the most valuable asset.

Once confidence broke, everything moved fast. The bank reported a €3.6 billion first-half loss in July 2014, trading was halted, and Portuguese authorities stepped in with a €4.9 billion rescue that split the bank into bad assets and Novo Banco.

The collapse did not begin when people started asking questions. It began when the structure could no longer fund itself.

Which part of financial fraud stories do you pay closest attention to: the hidden mechanics, or the exact moment the story stops holding together?

If you want more breakdowns like this, follow Novo Banco’s origin story through the full thread.

#FinancialCrime #BankingCrisis #Fraud #CorporateGovernance #Portugal #BancoEspiritoSanto #ForensicAccounting #FinanceHistory

It’s unsettling how easy fake revenue can look when the product really exists.

Quintis was not selling pure fiction. It had sandalwood plantations, real customers, and a story investors wanted to believe: premium Indian sandalwood, scarce supply, and future high-margin sales.

That mix is what made the fraud harder to spot. The company did not need to invent everything. It only needed to overstate sales, book revenue early, and use related-party deals to make demand look stronger than it was.

By 2017, Quintis had reached a market value of about A$3.4 billion on the ASX. Then the questions started: who was really buying, when was revenue actually earned, and how much of the reported demand was tied to entities linked to the company itself?

What matters in cases like this is mechanics. Once a business can point to real assets, real contracts, and real headlines, people stop checking whether the cash and accounting match the story.

Which detail makes you question a growth story fastest: revenue timing, related-party deals, or cash flow?

If you want more breakdowns like this, follow for the next thread.

#financialcrime #fraud #accountingfraud #Quintis #investing #corporategovernance #forensicaccounting #ASX

It’s unsettling how little needs to be real for a fraud to keep moving.

Trafigura is one of the biggest commodity traders in the world. In 2023, it revealed a $577 million loss after discovering that cargoes it believed contained nickel were, in many cases, made up of far lower-value material.

The case centered on Indian businessman Prateek Gupta and companies linked to TMT Metals and UD Trading Group. On paper, the transactions looked routine: warehouse documents, shipping paperwork, inspections, financing, and repeat trades over time.

That was the power of the scheme. It did not depend on a wild new invention. It depended on trust in documents, counterparties, and a market structure where goods move across ports, warehouses, and intermediaries long before anyone opens every container.

One reason this worked is simple: when a relationship has already produced profitable trades, people stop expecting the next shipment to be the one that breaks the story. That is often when the risk is highest.

The collapse came when Trafigura started physically inspecting containers and found the contents did not match the paperwork. A trade finance structure that looked solid on screen suddenly turned into a very expensive evidence trail.

What detail from this case stands out most to you: the fake documents, the repeated rollovers, or the fact that it reached a company as sophisticated as Trafigura?

If you want more real breakdowns like this, follow for the next story.

#FinancialCrime #Fraud #Trafigura #CommodityTrading #CorporateFraud #ForensicAccounting #WhiteCollarCrime #RiskManagement

It’s unsettling how easy fake growth can look when the shelves seem full.

Crazy Eddie was one of the best-known electronics chains in New York in the 1970s and 1980s. The ads were loud, the sales were real, and customers believed they were looking at a high-volume retail machine.

That image helped the company go public in 1984 and build credibility with investors. But behind the numbers, members of the Antar family were doing something much more deliberate: first hiding cash to evade taxes, then reversing the scheme and pumping fake inventory and fake profits into the books.

The mechanics matter. They overstated inventory, manipulated purchase records, and used false counts to inflate gross margin. In retail, inventory is one of the easiest places to manufacture profit, because if the stock number is wrong, earnings can look stronger without any real improvement in the business.

By the time the fraud unraveled, investors were left with a company that looked profitable on paper and was far weaker in reality. The story is a reminder that strong sales, media visibility, and a famous brand do not prove the accounts are clean.

Which fraud case do you think was the most mechanically clever?

If you want more breakdowns like this, follow for the next one.

#FinancialCrime #Fraud #CorporateFraud #AccountingFraud #WallStreet #ForensicAccounting #Investing #SEC

It looked like a retail success story.

Phar-Mor was founded by Mickey Monus and grew fast in the late 1980s by promising “power buying” and deep discounts. Customers saw busy stores. Investors saw growth. Banks saw a chain expanding across the U.S.

What they didn’t see was the accounting trick underneath it. Executives inflated inventory, buried losses, and created false entries to make the business look profitable when it was already bleeding cash. By 1992, the hole was estimated at roughly $500 million.

That detail matters because this wasn’t a complicated Wall Street product. It was a simple retail fraud hidden in one of the most basic numbers on the balance sheet. If inventory is fake, profit can be fake too.

The scheme lasted because rapid expansion gave management cover. New stores, new lenders, and reported sales growth made the story feel credible enough that fewer people pushed hard on the underlying numbers.

And when it finally broke, thousands of employees, suppliers, lenders, and investors paid for a lie that had been building for years.

Which kind of fraud do you think is more dangerous: the complex one nobody understands, or the simple one everyone assumes is fine?

More real financial crime breakdowns from Phar-Mor.

#FinancialCrime #AccountingFraud #PharMor #CorporateFraud #ForensicAccounting #RetailCollapse #WhiteCollarCrime #BusinessHistory

Sometimes the people behind a fraud are exactly the people everyone was trained to trust.

That’s what makes Toshiba so difficult to shake off. This was not a fringe startup, a loud promoter, or a flashy outsider story. It was one of Japan’s most respected companies, run by executives who looked disciplined, experienced, and deeply embedded in the corporate establishment.

Hisao Tanaka, Norio Sasaki, and Atsutoshi Nishida did not build credibility overnight. They rose through Toshiba over decades, held top leadership roles, and managed a company tied to everything from electronics to infrastructure to nuclear power. In Japan’s corporate culture, that kind of pedigree mattered.

The pressure started at the top. Managers were pushed to hit aggressive profit targets called “challenges,” even when business conditions made those numbers unrealistic. Instead of reporting weak results, divisions delayed losses, pulled profits forward, and used percentage-of-completion accounting to make projects look healthier than they were.

By 2015, an independent investigation found Toshiba had overstated profit by about ¥151.8 billion, roughly $1.2 billion, over seven years. The fraud was not hidden in one dramatic transaction. It spread across PCs, semiconductors, infrastructure, and other units because the system rewarded obedience more than honesty.

What stays with me is how ordinary the setup looked from the outside. Respectable executives. Familiar brand. Internal targets. That is often enough to keep people from asking the second question.

Which corporate fraud still surprises you most when you look at who was running it?

If you want more breakdowns like this, follow for more real financial crime stories.

#FinancialCrime #AccountingFraud #Toshiba #CorporateGovernance #FraudCase #ForensicAccounting #WhiteCollarCrime #BusinessHistory

He looked exactly like the person you were supposed to trust.

That was the point of Bernard Madoff.

He wasn’t some outsider yelling about impossible returns. He was a former NASDAQ chairman, a market maker, a fixture of Wall Street, and a familiar name in wealthy circles from New York to Palm Beach.

By the time investors started asking harder questions, the image was already doing half the work. People weren’t just trusting performance. They were trusting his reputation, his clients, his exclusivity, and the feeling that access to him meant you were part of something sophisticated.

That is what makes this case so disturbing. The fraud did not survive because it looked reckless. It survived because it looked respectable.

Even more unsettling: multiple warnings surfaced for years, including detailed concerns from Harry Markopolos, but the combination of prestige, consistency, and social proof kept the machine alive until the 2008 financial crisis forced redemptions the scheme could not meet.

Do you think elite reputation makes fraud harder for people to question?

If you want more stories like this, follow for the next breakdown.

#FinancialCrime #BernieMadoff #WallStreet #PonziScheme #Fraud #FinanceHistory #TrueCrime #Investing

It’s hard to forget how ordinary this fraud looked.

Carillion was not a meme stock story or a flashy startup collapse. It was a major UK outsourcer tied to hospitals, schools, rail, and public contracts. That was exactly why so many people trusted it.

The problem was not one dramatic theft. It was years of optimistic accounting, weak cash generation, rising debt, and contract profits that existed on paper long before the economics were real.

By the time the market fully understood the gap, the company had just £29 million in cash and about £7 billion in liabilities. In January 2018, it went into compulsory liquidation.

What makes this case important is how believable it all sounded while it was happening. Revenue kept coming in. Big projects kept getting announced. The public story still looked stable even as the balance sheet deteriorated.

That is often how financial failure scales: not with one unbelievable lie, but with a long chain of assumptions nobody wants to challenge early enough.

Which corporate collapse do you think looked most credible right before it broke?

More deep breakdowns like this from Carillion soon.

#FinancialCrime #AccountingFraud #Carillion #CorporateCollapse #ForensicAccounting #FinanceTwitter #BusinessHistory #CorporateGovernance

It’s disturbing how long fake value can survive once prestige takes over.

Steinhoff did not look like an obvious fraud story. It owned real businesses, operated in more than 30 countries, and had a market value of about €20 billion in 2017. To most people, it looked like a legitimate global retail empire.

That was the cover. Behind it, investigators later found years of fictitious and irregular transactions, inflated asset values, and related-party deals that made weak businesses look stronger than they were. The alleged profit did not come from one brilliant operating model. A lot of it came from accounting that made losses disappear.

What made it work was credibility. Markus Jooste was treated as a proven operator. Big acquisitions made Steinhoff look ambitious and sophisticated. Listings in Frankfurt and ties to major lenders helped create the sense that serious people had already done the checking.

When the accounting finally started to unravel in December 2017, the share price collapsed by more than 90% in days. Billions were wiped out, investors were trapped, and one of Europe’s biggest corporate scandals was suddenly impossible to ignore.

The part people miss is that frauds like this do not always rely on fake products or fake customers. Sometimes the lie sits inside valuations, intercompany transactions, and documents most outsiders never see.

Which corporate fraud do you think was most convincing before it broke?

If you want more breakdowns like this, follow for the next one.

#FinancialCrime #CorporateFraud #Steinhoff #AccountingScandal #Investing #ForensicAccounting #FinanceHistory #BusinessBreakdown

It’s disturbing how long fake profit can look like real performance.

HealthSouth was once one of America’s biggest rehabilitation hospital companies. Founded by Richard Scrushy in Birmingham, Alabama, it grew fast, reported strong numbers, and looked exactly like the kind of public company investors were supposed to trust.

But behind that image, executives were adjusting the books quarter after quarter just to hit Wall Street targets. By 2003, federal investigators said HealthSouth had overstated earnings and assets by roughly $1.4 billion.

What makes this case worth revisiting is how ordinary the pressure looked at first. Miss an earnings target, make a “temporary” fix, then repeat it next quarter because the gap gets bigger. That is how a public-company lie becomes a system.

The fraud did not collapse because the story suddenly stopped sounding good. It collapsed because investigators, cooperating executives, and hard numbers finally forced the company’s internal fiction into the open.

Which detail usually surprises you most in cases like this: the scale, the simplicity, or how long it stayed hidden?

If you want more real breakdowns like this, follow for the next case.

#FinancialCrime #AccountingFraud #HealthSouth #CorporateFraud #WhiteCollarCrime #SEC #ForensicAccounting #Investing

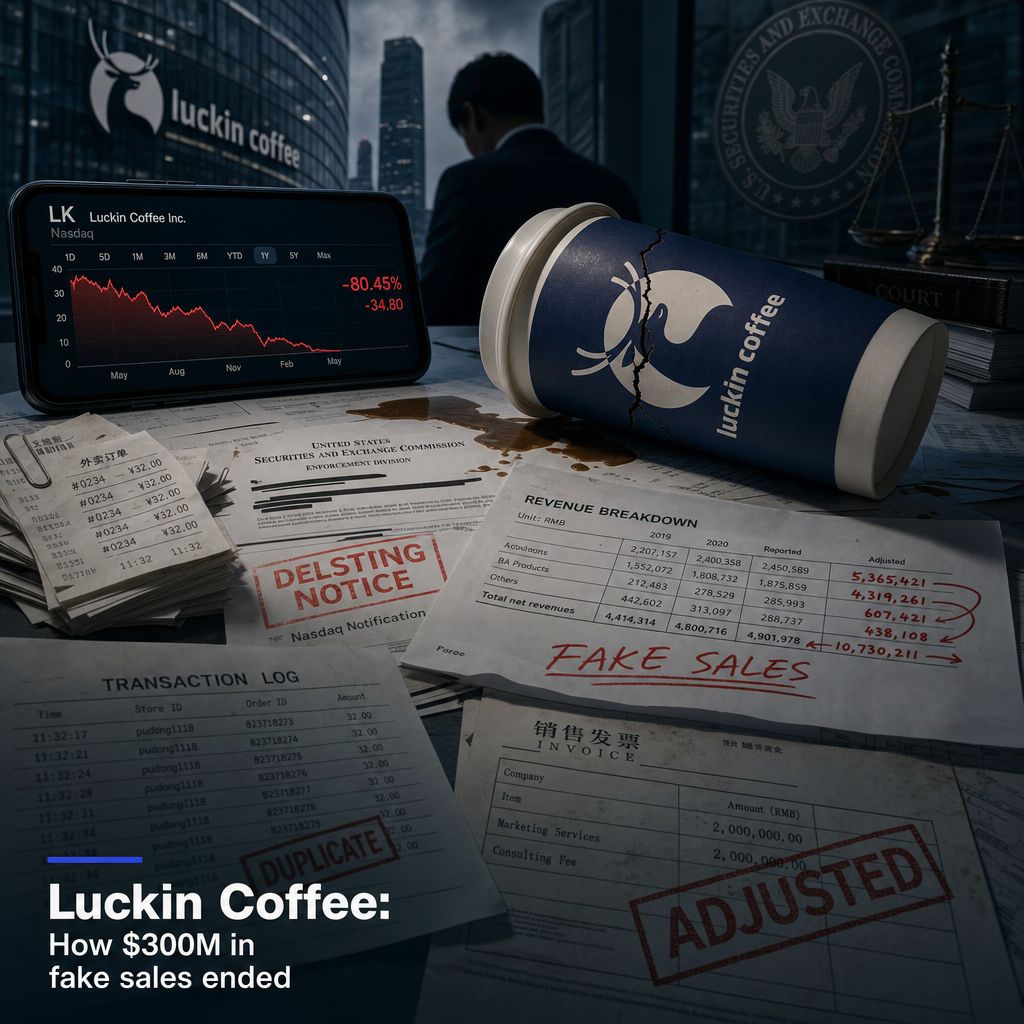

It’s strange how easy growth can look when no one checks the receipts.

Luckin Coffee sold investors a perfect story in 2019: China’s fast answer to Starbucks, thousands of stores, explosive mobile orders, and a brand that seemed built for scale. The company listed on Nasdaq in May 2019 and quickly reached a market value of around $12 billion.

But behind that image, employees were fabricating transactions. Between the second and fourth quarters of 2019, the company inflated sales by roughly RMB 2.12 billion, about $300 million at the time. The method was not abstract. Fake vouchers, inflated order counts, and manipulated expenses made the business look far stronger than it was.

What made it work was how believable the outside story already looked. The stores were real. The app was real. The expansion was real. When a company grows fast enough, people often stop asking whether the economics underneath it make any sense.

The collapse started when Muddy Waters received an anonymous 89-page report in early 2020, based on tens of thousands of hours of store surveillance and receipt analysis. In April 2020, Luckin admitted the fabrication. The stock crashed, the company was delisted from Nasdaq, and investors were left with the difference between the story and the numbers.

Which matters more in a fraud case like this: the fake numbers, or the real business that makes the lie easier to believe?

If you want more stories like this, follow for the next breakdown.

#FinancialCrime #AccountingFraud #LuckinCoffee #CorporateFraud #FraudCase #ForensicAccounting #Investing #WhiteCollarCrime

The part after the collapse is usually where the real damage becomes visible.

Luckin Coffee did not just lose a growth story. After the fraud surfaced in 2020, the company was removed from Nasdaq, paid a $180 million SEC settlement, and admitted that employees had fabricated roughly RMB 2.12 billion in sales.

What makes this ending worth studying is how ordinary the original business looked. It sold coffee, opened stores fast, offered app-based discounts, and gave investors a simple narrative: China’s answer to Starbucks, built for scale.

Once that story broke, everything changed. Shareholders were hit, creditors had to negotiate through restructuring, executives were pushed out, and the company’s reputation became tied to one of the clearest examples of fabricated retail growth in recent years.

The lesson is not just that fraud gets punished. It’s that fake operating numbers can destroy trust faster than almost any bad quarter, especially when a company used speed, brand visibility, and market excitement as proof that the numbers must be real.

Which ending sticks with you more in these cases: the moment the fraud is exposed, or the years of fallout after?

If you want more real financial crime breakdowns, follow for the next one.

#FinancialCrime #Fraud #LuckinCoffee #AccountingFraud #CorporateScandal #Investing #SEC #ForensicAccounting

The ending is the part people forget.

Luckin Coffee looked like one of the fastest-growing consumer companies in China. In less than 2 years, it opened thousands of stores, raised major capital, and listed on Nasdaq in May 2019 at a valuation of roughly $4 billion.

Then in April 2020, the company announced an internal investigation had found fabricated transactions worth about RMB 2.2 billion, roughly $310 million. The growth story investors trusted was not built on normal demand. A meaningful part of it had been manufactured.

What followed was brutal. The stock collapsed by more than 80%, Nasdaq moved to delist the company, and shareholders filed lawsuits while regulators in both the US and China moved in.

In December 2020, Luckin agreed to pay a $180 million penalty to the SEC for misleading investors. Its chairman Charles Zhengyao was pushed out, senior executives were removed, and the company entered provisional liquidation in the Cayman Islands before later restructuring.

The striking part is that the business did not disappear completely. Even after the fraud scandal, Luckin kept operating stores in China, reorganised, and eventually reported a commercial recovery under new management.

That is what makes cases like this so difficult. A company can have a real product, real customers, and still fake crucial numbers when the pressure to sustain hypergrowth gets too high.

Which part shocks you more: how the fraud was done, or how the company survived after it was exposed?

More case breakdowns like this from Luckin Coffee.

#FinancialCrime #FraudCase #LuckinCoffee #CorporateFraud #SEC #Investing #Nasdaq #AccountingFraud

Sometimes a fraud survives for years because one document never gets checked properly.

Peregrine Financial Group looked like a serious futures broker. It was based in Cedar Falls, Iowa, handled customer money, and was run by Russell Wasendorf Sr., a well-known industry figure who had spent years building credibility with regulators and industry groups.

But the collapse did not begin with some dramatic market event. It began in July 2012, when regulators asked for direct confirmation of customer funds from U.S. Bank instead of relying on paperwork sent through the firm.

That one change mattered because the paperwork had been the fraud. For years, Wasendorf used a P.O. box, intercepted bank mail, and forged statements to make it look like customer accounts held about $220 million when the real balance was only around $5 million.

On 9 July 2012, after a suicide attempt and a confession, the gap was no longer deniable. Investigators found that more than $215 million in segregated customer funds had been stolen, and Peregrine Financial Group collapsed almost immediately.

The case is a reminder that trust signals are not controls. Sometimes the entire illusion lasts until one outsider insists on getting the answer from the bank itself.

What financial crime collapse do you think turned on the smallest procedural change?

More real case breakdowns from this series soon.

#FinancialCrime #Fraud #TrueCrime #WallStreet #CorporateFraud #AccountingFraud #Finance #Investing

What gets me about WorldCom is how the collapse began with something that looked boring.

Not a dramatic raid. Not a leaked confession. Just accounting entries that did not make sense.

By the early 2000s, WorldCom was one of the biggest telecom companies in the US. It had grown through acquisitions, including its $37 billion deal for MCI in 1998, and investors had been trained to expect constant growth. That expectation became the trap.

When telecom demand slowed after the dot-com boom, the business could not support the numbers Wall Street wanted. Instead of reporting weaker profits, executives shifted billions of dollars in ordinary line costs onto the balance sheet, making expenses disappear from the income statement.

The turning point came in 2002, when internal auditor Cynthia Cooper and her team kept digging despite resistance from senior management. They found that roughly $3.8 billion had been improperly classified. That discovery opened the door to a much larger fraud that eventually totaled more than $11 billion.

It is a good reminder that some of the biggest collapses start in spreadsheets, not headlines.

Which fraud collapse do you think was exposed in the most revealing way?

If you want more breakdowns like this, follow for the next one.

#WorldCom #FinancialCrime #AccountingFraud #CorporateFraud #MCI #SEC #Audit #BusinessHistory

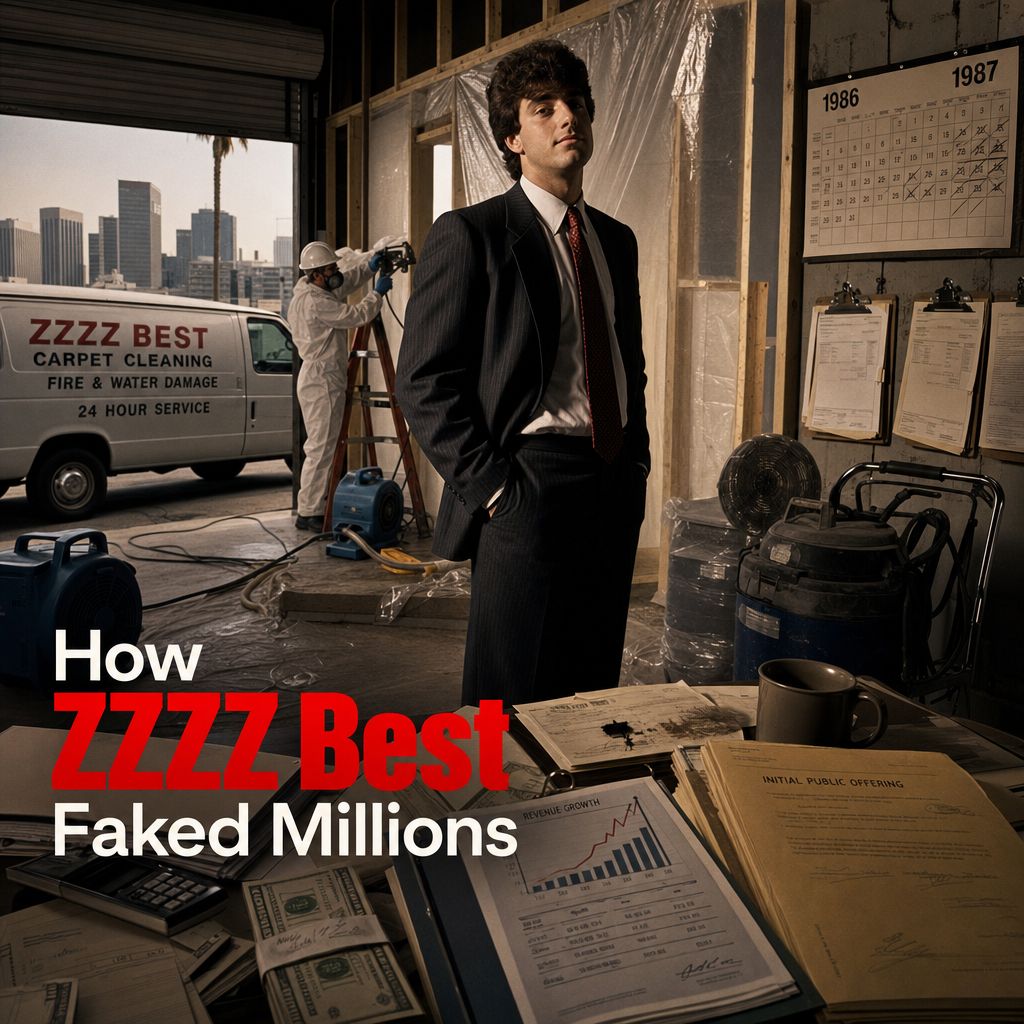

What gets me is how little real business was needed to sell a big success story.

Barry Minkow was still a teenager when ZZZZ Best became one of the most talked-about companies in Los Angeles. On paper, it looked like a fast-growing carpet cleaning business that had expanded into insurance restoration after fires and floods.

That second part was the key. Restoration work sounded bigger, more corporate, and harder for outsiders to verify. Minkow and his team used fake job sites, forged documents, and coached witnesses to convince auditors, bankers, and investors that millions in revenue were real.

By 1987, ZZZZ Best had gone public and was valued at around $200 million. The illusion held because people saw a young founder, rising sales, respected advisers, and apparent contracts with insurers. Those signals did a lot of the work.

The collapse came when investigators started checking the details behind the restoration jobs and found that some sites were staged or didn’t belong to ZZZZ Best at all. Once that pressure started, the numbers could not support themselves.

That is what makes this case worth studying: not just the fraud, but the mechanics. How a story moved through paperwork, job sites, lenders, and public markets until it looked real enough to fund itself.

Which fraud case do you think was most dependent on appearances rather than actual cash flow?

If you want more breakdowns like this, follow for more real financial crime stories.

#FinancialCrime #Fraud #AccountingFraud #WallStreet #CorporateFraud #TrueCrime #Investing #BarryMinkow #ZZZZBest #BusinessHistory

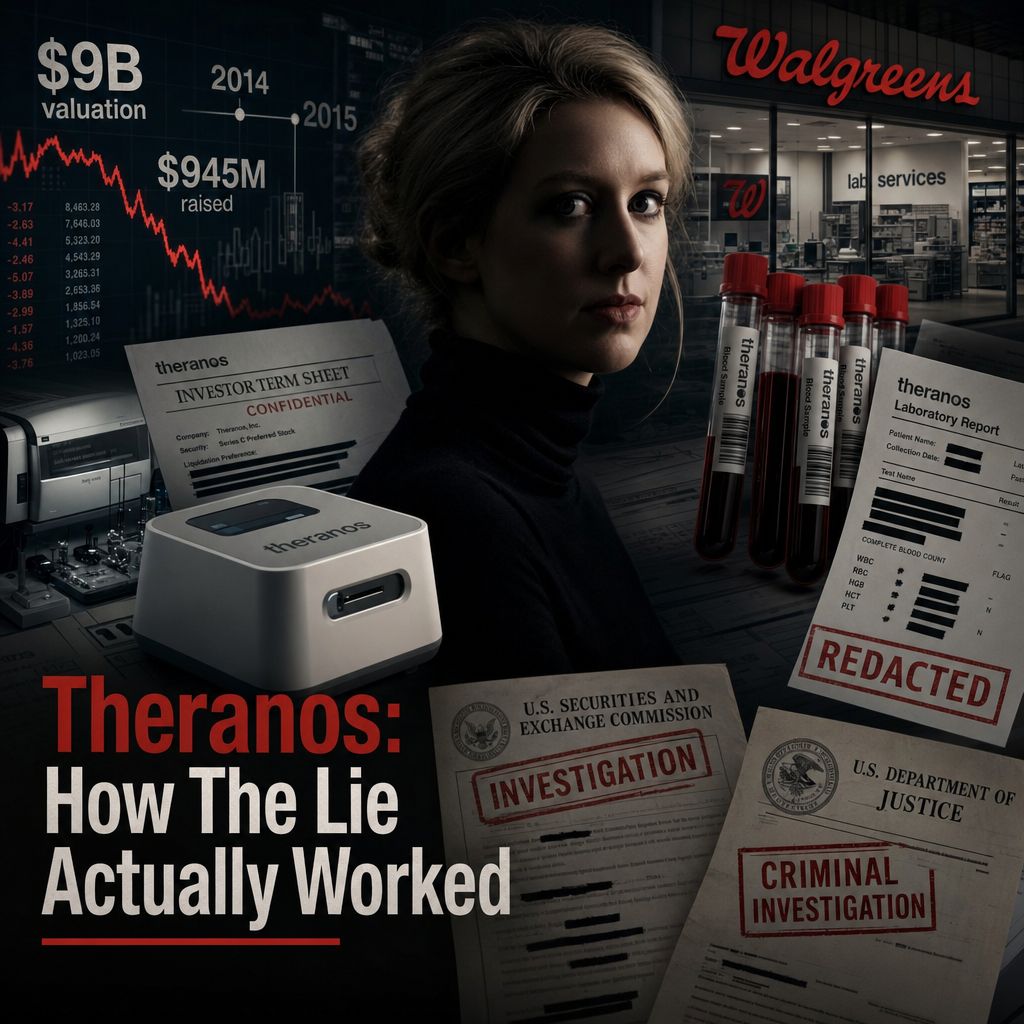

What stays with me is how little real science there was beneath so much certainty.

Theranos was not just a bad startup that failed. It spent years claiming its Edison machine could run hundreds of blood tests from a finger-prick sample, even while many tests were actually being done on traditional Siemens analyzers behind the scenes.

That detail matters because the fraud was not only in the marketing. It was in the gap between what patients, investors, and partners thought the technology was doing and what the company’s lab operations were actually capable of.

By 2014, Theranos had been valued at about $9 billion. Walgreens had put Theranos wellness centers in Arizona stores. High-profile investors and board members made the story feel safer than it was.

Then the reporting started. In 2015, John Carreyrou at The Wall Street Journal exposed serious problems with test accuracy, device capability, and internal practices. Regulators followed, deals unraveled, and the image collapsed much faster than it had been built.

The part people miss is that this was not one dramatic trick. It was a chain of decisions: overstated technology, hidden lab work, controlled information, and relentless pressure to keep the promise alive.

Which fraud case do you think looked the most believable before it fell apart?

If you want more breakdowns like this, follow for the next deep dive.

#Theranos #ElizabethHolmes #FinancialCrime #Fraud #CorporateFraud #StartupFraud #WhiteCollarCrime #BusinessHistory #WallStreetJournal #Fintech

The part that stays with me is how ordinary the lie looked at first.

Enron was not selling some impossible fantasy. It was a Houston energy company that looked sophisticated, connected, and unstoppable. By 2000, it reported about $100.8 billion in revenue and was celebrated as one of America’s smartest businesses.

But the core misconduct was brutally simple. Executives used mark-to-market accounting to book years of projected profit on day one, even when the cash might never arrive. Then they pushed debt and weak assets into off-balance-sheet partnerships so Enron could keep reporting growth while the underlying business deteriorated.

Andrew Fastow’s SPEs, including LJM and Chewco, helped move liabilities away from Enron’s financial statements. Losses were hidden, earnings were smoothed, and investors were shown a cleaner company than the one that actually existed.

What made it work was trust. Big banks were involved, Arthur Andersen signed the accounts, analysts praised the model, and the stock price became its own form of proof. That combination made basic skepticism feel almost unsophisticated.

When confidence broke in late 2001, the numbers could not protect the story anymore. Enron filed for bankruptcy on December 2, 2001, investors were wiped out, employees lost jobs and retirement savings, and one of the most admired companies in America collapsed into a case study in financial deception.

Which financial fraud case do you think people still misunderstand the most?

If you want more breakdowns like this, Enron is one worth studying closely.

#Enron #FinancialCrime #CorporateFraud #AccountingFraud #WhiteCollarCrime #Finance #Investing #BusinessHistory

It’s disturbing how easily fake cash can hide inside an ordinary business.

Patisserie Valerie did not look like a complicated fraud story. It sold cakes, coffee, and meals on British high streets. Customers saw busy shops. Investors saw a growing retail chain. On paper, it looked stable.

The misconduct was far more basic and far more dangerous. The accounts allegedly overstated cash, understated debts, and hid the company’s real financial position for years. In October 2018, the board said it had discovered significant accounting irregularities and a potential fraud.

What made the case so striking is that this was not a mysterious crypto token or an exotic offshore fund. It was a consumer brand listed on London’s AIM market, chaired by well-known entrepreneur Luke Johnson, with reported revenues of more than £100 million.

Then the numbers stopped making sense. The company disclosed a potential £20 million black hole, later investigations pointed to around £94 million of misstated balances, and the business went into administration in January 2019.

That gap was not just an accounting issue. Jobs were lost, shareholders were wiped out, and trust in a familiar brand collapsed almost overnight.

Which corporate fraud case shocked you most because the business looked so normal?

If stories like this interest you, Patisserie Valerie is a case worth studying closely.

#FinancialCrime #AccountingFraud #PatisserieValerie #CorporateFraud #ForensicAccounting #BusinessScandal #FraudCase #Investing