it's like a low float high FDV token TGEing this Friday. there will be volatility for sure.

if sophisticated actors choose to pump it and people FOMO into $SPCX, it's likely they are going to liquidate the most profitable positions. (Semis ?)

That's the doom case.

Sense of urgency is different, imo. We have known about SpaceX IPO for weeks including the details of the IPO. Those who fears will prepare for it.

Trump coin actually a surprise that few people knew it was real.

I went from spending ZERO to over $30,000 per year run rate in Claude in just 6 month. This thought crossed my mind multiple times whether its worth it. Not because I don't see value in hidden angles sheet that we produce daily. It's because of usage limitations even with that much amount of spending. This note from Citadel touches upon this: "... ration scarce capacity towards the areas where the marginal productivity of AI justifies the marginal cost of using it." This note is yet another reason why semiconductors are getting wrecked daily.

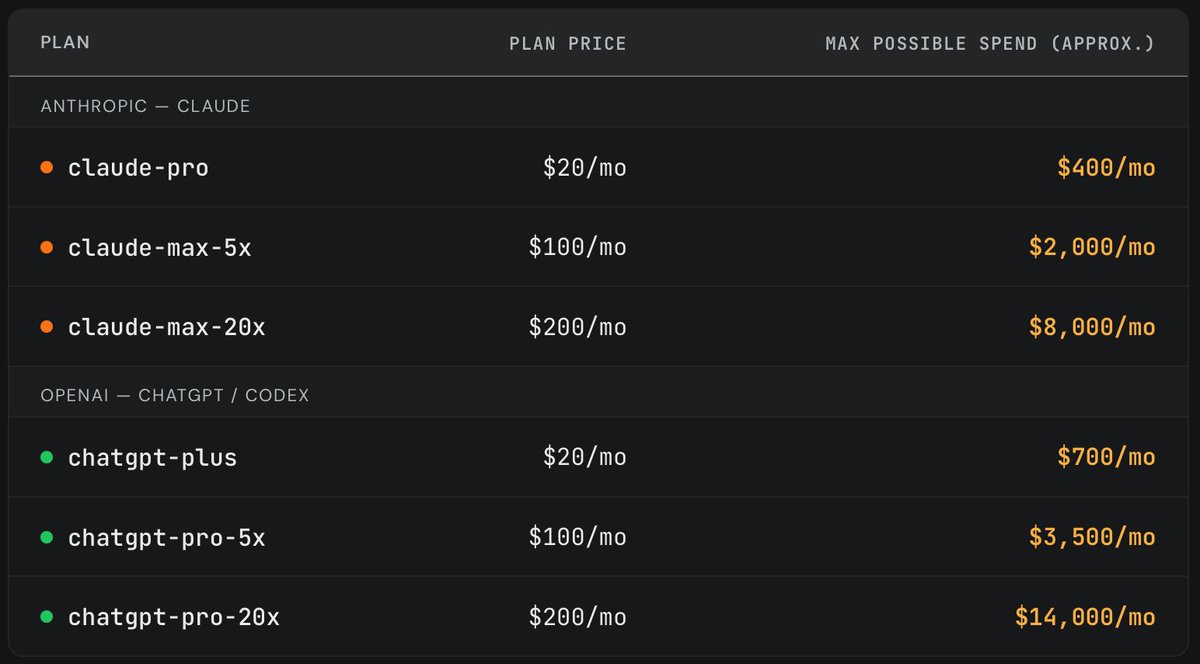

Recently, we purchased one of each Anthropic/OpenAI subscription plan and randomly ran long horizon coding tasks until we exhausted the weekly limit. It's widely believed that a $200/month plan maxes out at ~$2000/month worth of tokens (assuming API pricing). However, we found that the subscriptions are actually far more generous. (2/4)

The most basic way AI could blow up imo. I'm not saying it does but this is the most obvious way I can see it happening

- Per seat subscriptions are massively subsidized. The flat fee was priced way below what heavy usage actually costs

- For real business use you have to move to the API anyway. Data protections, work integrations and compliance officer approval

- On the API you pay metered rates, and businesses are burning credits way faster than the per seat pricing ever led them to expect

- This is everywhere right now. Internally for us, Codex users, Uber torching its entire 2026 AI budget in 4 months, the Microsoft comments. Just go try an API

I shared more on this here: https://t.co/iZrqrCAIRW

- And I don't think most businesses have the money to keep paying increasing API rates without a real change to how they operate (caps needed)

- Because they have a cheap alternative. They can reach open source models through any aggregator (OpenRouter, Venice, Baseten, Together) and still get strong privacy. Venice private data centers, or E2EE/TEE serving GLM 5.1.

More on open source inference provider raises here: https://t.co/7kf56P44yQ

- And the discount is enormous. DeepSeek V4 codes within a hair of Opus on SWE bench at roughly 1/30th the price, and the cheapest open models run closer to 1/100th

- Chinese labs open source frontier grade models. The model is the single biggest cost an inference provider has, and they get it for free

- This idea dies if China goes closed source. That is actually bullish web2 AI labs, because if everyone is closed you pay up for the best intelligence. China goes closed source if they are tired of giving away an asset and they want the revenue and data flow to train new models

- Is this showing up in web2 AI lab revenue yet? No. Revenue is off the charts. Anthropic went from 9B to 47B run rate in five months

- So go forward, what happens?

- I think revenue slowly starts leaking to the open source inference providers (see Venice usage, OpenRouter's $113M raise, Baseten is raising at $11B or triple its valuation in three months, on revenue that went from $200M to $600M annualized in a single quarter)

- It doesnt move overnight, but it caps the labs ability to raise prices, and margins are already deeply negative. OpenAI is reportedly running near negative 122%

- With margins that bad there is no cash flow, so the labs are fully dependent on outside capital to buy GPUs, train models, and keep subsidizing usage (I.e. see Google tapping $80b equity sale, granted 30b for employee RSU taxes. Clearly they think Equity is overvalued or you wouldn't sell it)

- The break comes when that capital stops. Pricing is capped so margins cant improve, and the moment investors lose conviction on payback, the whole flow reverses

- Why would they lose conviction on payback? Back to the start - the inability to improve margins or get businesses to pay more

- This is also limiting, if we start making new drugs with AI or create entirely new businesses, you better believe people will pay up to the max for AI usage

SemiAnalysis occasionally publishes non-semiconductor analysis, and I really enjoyed reading this one. I know almost nothing about robotics, but I found this kind of content really fascinating.

Testing a equities thesis: permanent underclass index

- We already know 99% of consumer brands are giving us terrible quality. Luxury or otherwise

- Value accrues to barbell:

$100k/hr SF escorts who play DnD on one side, TJ Max clothing for 90% of america on the other side

It's AI resilient as well:

AGI hits: Underclass given slop dividends sufficient to caloriemax

No AGI - Economic recession due to levered AI buildout. Chicken nuggets no caviar in 2028

There's a thesis to play with about a rotation away from ecommerce, which has largely become a scam front for drastically upcharged goods from Chinese factories. Amazon delivers upcharged slop really fast, I might as well just go buy the same slop for a 15 min drive. In fact the slop is often better, and much cheaper.

Walk into a TJ MAX, you feel the America inside of you.

The Underclass isn't so bad here.

I'm sorry dad.

This is not a robotics thesis. It is a funnel.

Slick video, charismatic marketer, “why I bet my career on robotics.” He works for $BOT. RoboStrategy, the closed-end vehicle Andrew Kang now runs and openly brands the “MicroStrategy of robotics.”

Same playbook: a committed equity facility that only works if the share price stays bid and retail keeps showing up to absorb the issuance. The content is the top of the funnel. You are the liquidity.

We traded millions of dollars of converts on the real robotics names in the late 2010s, mostly within a convertible arbitrage mandate, not fundamental stock-picking. Which is exactly why we can point at the honest alternatives here, the ones nobody is cutting a hype video for, because there is no salesman making big bucks dumping them on you.

If you want robotics exposure, the honest version is already listed in Tokyo. FANUC (6954), 20%+ operating margins through full vertical integration. Keyence (6861), asset-light, ROE most software firms would kill for. Yaskawa (6506), the servo muscle behind half the world’s arms. The Japanese Big Five ship 40%+ of global industrial robots. These are priced for competence, audited for decades, and you can size them without praying a NAV premium holds. Dull. Real. Yours at a clearing price.

And if you actually want the convexity, the asymmetric leg, it is one layer down in the actuation supply chain, not in a closed-end fund. Harmonic Drive Systems (6324), Nabtesco (6268), the strain-wave reducer makers. A humanoid needs roughly 20 harmonic drives per unit, which makes precision reducer supply the binding constraint on the entire scaling story. That is where the torque is. That is also where you get your face removed if the shipment curve disappoints. Omdia has 2025 humanoid shipments up ~480% to ~13,000 units, real growth, and a rounding error against the valuations now leaning on it.

So here is the actual choice. You can own the cash-generating incumbents directly, at a price, with no wrapper skimming you. You can own the actuation convexity directly, eyes open, and underwrite the humanoid curve yourself. Or you can buy a single ticker at a premium to its own book, structured so the manager can print on your ‘enthusiasm’, and call that a career bet.

Robotics is real. The compounding is real. The funnel is also real, and it is looking for your money.

The edge was never finding the names. The edge is knowing who is selling, and to whom.

BREAKING: Iran says it has now fully blocked the Bab el-Mandeb Strait, along with the complete closure of the Strait of Hormuz, with the next step being strikes on oil, gas and energy infrastructure of US-allied Gulf countries in response to today's Israeli strikes on the Petrochemical Complex, per a source close to Iran's Ghalibaf.

[속보] 삼성·하이닉스, 2분기 또 최대실적 가능성…영업익 150조 전망

7일 연합인포맥스가 최근 1개월 내 보고서를 낸 증권사 15곳의 컨센서스(실적 전망치)를 집계한 결과, 삼성전자와 SK하이닉스의 2분기 합산 영업이익은 150조원을 상회할 것으로 전망되고 있다.

삼성전자의 2분기 매출과 영업이익이 각각 171조7천347억원, 88조3천29억원으로 추정된다.

이는 지난해 같은 기간과 비교해 매출은 130%, 영업이익은 1천788% 급증한 수치다. 전 분기 영업이익(57조2천328억원)보다도 30조원 이상 늘어난 수준이다.

이 같은 실적 전망에는 반도체 사업의 호조가 결정적인 역할을 했다. 올해 들어 삼성전자 반도체 사업을 담당하는 디바이스솔루션(DS)부문은 전사 영업이익의 약 95%를 차지하며 실적을 견인하고 있다.

증권가에서는 메모리 사업부에서 D램 약 60조∼70조원, 낸드 약 20조원에 달하는 영업이익을 낸 것으로 전망한다. 다만 시스템LSI·파운드리 사업부의 경우 2분기에도 적자가 예상된다.

삼성전자의 경우 세계 최대 규모의 캐파(생산능력)를 바탕으로 범용 D램 제품 생산·판매를 확대한 것이 주효했던 것으로 풀이된다. HBM 판매도 증가세를 이어가고 있다.

SK하이닉스 역시 사상 최대 실적 경신이 유력하다. 연합인포맥스 집계 결과 SK하이닉스의 2분기 매출과 영업이익은 각각 83조4천135억원, 64조3천195억원으로 추정된다. 직전 분기 영업이익은 37조6천103억원이었다.

영업이익률도 종전 최고 기록이었던 1분기(약 72%)를 넘어설 것으로 예상된다. 일각에서는 80%에 육박할 수 있다는 전망도 나온다.

'수익성의 지표'로 불리는 파운드리 업계 1위 TSMC와 격차도 더욱 커질 수 있다. TSMC의 2분기 영업이익률은 56.5∼58.5%로 전망된다.

SK하이닉스는 당분간 메모리 공급 부족 현상이 지속될 것으로 예상됨에 따라 중장기 캐파 확대에 나선다는 방침이다.

SK하이닉스는 현재 청주 M15X·P&T7, 용인 반도체 클러스터, 미국 어드밴스드 패키징 공장 등에 대규모 투자를 이어가며 생산 역량 강화에 나서고 있다.

최태원 SK그룹 회장은 지난 2일 컴퓨텍스 2026 행사장에서 "메모리 병목현상은 2030년까지 계속될 전망"이라며 "향후 5년 동안 웨이퍼 기준 반도체 생산 능력을 2배로 늘릴 계획"이라고 말했다.

truly believe $BB is going make waves in the coming months if not weeks.

Surprised people still think it’s a dead phone company little do they know physical AI is on the rise and robotics is going to take over.

QNX mode.

If any 1 of these guys are bullposting a coin, you're not early. If all 3 of them are bullposting a coin, you're *definitely* not early. If all 3 of them are bullposting a coin and said coin is already up more than 10x, and you still buy in, you probably need to find a new hobby.

I see a lot of people knife catching & calling bottoms. Take it from me, it’s not worth it. I thought 30k was a good bottom in 2022…then it moved to 16k 💀

Wait for confirmation bc if this is bottom there’s plenty of upside…if not then you’ve not lost money

TLDR: Take your time and dca spot, wait to leverage until there is more evidence is bottom is in.

This is a really impressive tool built by @derivativemonky for options traders

https://t.co/HunPO4kYpa

GEX profile indicating we maybe bottom around 60k?

The way to understand the ZCash bug is it’s not infinite mint of ZEC itself. It’s more like the shielded pool (Orchard) could become insolvent. Think of it more like the KelpDAO hack for ETH.

Very little reason not to proactively unshield any ZEC today. Being early to the exit is always better in a bank run. Consider Orchard burned, and don’t re-shield until there’s a new pool with a clean history

Turns out ZEC did have a hidden infinite inflation bug. The price action historically was consistent with it. If someone is sitting on infinite ZEC they had minted, they’d slowly liquidate to not reveal this fact.

![ohmahahm's tweet photo. [속보] 삼성·하이닉스, 2분기 또 최대실적 가능성…영업익 150조 전망

7일 연합인포맥스가 최근 1개월 내 보고서를 낸 증권사 15곳의 컨센서스(실적 전망치)를 집계한 결과, 삼성전자와 SK하이닉스의 2분기 합산 영업이익은 150조원을 상회할 것으로 전망되고 있다.

삼성전자의 2분기 매출과 영업이익이 각각 171조7천347억원, 88조3천29억원으로 추정된다.

이는 지난해 같은 기간과 비교해 매출은 130%, 영업이익은 1천788% 급증한 수치다. 전 분기 영업이익(57조2천328억원)보다도 30조원 이상 늘어난 수준이다.

이 같은 실적 전망에는 반도체 사업의 호조가 결정적인 역할을 했다. 올해 들어 삼성전자 반도체 사업을 담당하는 디바이스솔루션(DS)부문은 전사 영업이익의 약 95%를 차지하며 실적을 견인하고 있다.

증권가에서는 메모리 사업부에서 D램 약 60조∼70조원, 낸드 약 20조원에 달하는 영업이익을 낸 것으로 전망한다. 다만 시스템LSI·파운드리 사업부의 경우 2분기에도 적자가 예상된다.

삼성전자의 경우 세계 최대 규모의 캐파(생산능력)를 바탕으로 범용 D램 제품 생산·판매를 확대한 것이 주효했던 것으로 풀이된다. HBM 판매도 증가세를 이어가고 있다.

SK하이닉스 역시 사상 최대 실적 경신이 유력하다. 연합인포맥스 집계 결과 SK하이닉스의 2분기 매출과 영업이익은 각각 83조4천135억원, 64조3천195억원으로 추정된다. 직전 분기 영업이익은 37조6천103억원이었다.

영업이익률도 종전 최고 기록이었던 1분기(약 72%)를 넘어설 것으로 예상된다. 일각에서는 80%에 육박할 수 있다는 전망도 나온다.

'수익성의 지표'로 불리는 파운드리 업계 1위 TSMC와 격차도 더욱 커질 수 있다. TSMC의 2분기 영업이익률은 56.5∼58.5%로 전망된다.

SK하이닉스는 당분간 메모리 공급 부족 현상이 지속될 것으로 예상됨에 따라 중장기 캐파 확대에 나선다는 방침이다.

SK하이닉스는 현재 청주 M15X·P&T7, 용인 반도체 클러스터, 미국 어드밴스드 패키징 공장 등에 대규모 투자를 이어가며 생산 역량 강화에 나서고 있다.

최태원 SK그룹 회장은 지난 2일 컴퓨텍스 2026 행사장에서 "메모리 병목현상은 2030년까지 계속될 전망"이라며 "향후 5년 동안 웨이퍼 기준 반도체 생산 능력을 2배로 늘릴 계획"이라고 말했다.](https://pbs.twimg.com/media/HKLHz-raUAAq-pu.jpg)