Yesterday, $DELL spiked 45% after its Q1 earnings.

Options exploded 20000%-30000% in 1 day (rare).

Next week, there's 4 earnings with exact same set-up:

1. $CRWD 📅 Earnings: June 3 (After Close)

As enterprises deploy thousands of AI agents, cloud workloads, and connected endpoints, the security perimeter expands infinitely, making Falcon's AI-driven threat detection not optional but mandatory.

No one builds a $500B AI datacenter and skimps on security. $CRWD is the toll booth on the AI buildout highway and that moat compounds with every new customer and dataset feeding its threat intelligence engine.

Target: $800 median | $700 Wedbush & Benchmark | $750 Oppenheimer

2. $AVGO 📅 Earnings: June 2 (After Close)

Custom AI chip (XPU) demand from hyperscalers accelerating every quarter. $AVGO is the silent infrastructure backbone of the AI supercycle.

While $NVDA dominates training, Broadcom owns the custom silicon layer designing the XPUs that $GOOG, $META, and Tiktok use to run inference at hyperscale, plus the networking chips that stitch datacenters together.

As hyperscalers race to reduce $NVDA dependency and build proprietary AI chips, Broadcom is the only company with the design expertise and manufacturing relationships to deliver.

Target: $500 avg | $480 Susquehanna | $560 high

3. $PANW 📅 Earnings: June 2 (After Close)

Platformization strategy converting AI security budgets into sticky, recurring revenue.

AI doesn't just create new threats it supercharges existing ones, making next-gen cybersecurity a non-negotiable line item for every enterprise on the planet.

PANW's platformization strategy is purpose-built for this world: one unified platform replacing dozens of point solutions, with AI models running across network, cloud, and endpoint security simultaneously.

Target: $320 avg | $340 high | $300 median (75 analysts)

4. $GTLB 📅 Earnings: June 2 (After Close)

AI-native DevSecOps platform controls full dev lifecycle as code volumes explode.

AI is going to produce more code in the next five years than humans wrote in the last fifty and all of it needs to be managed, secured, and deployed somewhere.

While competitors like GitHub Copilot focus on code generation, GitLab controls the entire pipeline and that becomes more valuable, not less, as AI-generated code volumes explode.

Target: $40 median | $60 high (Macquarie) | $27 low (Cantor)

$ORCL earnings is on June 10 and $MU is on June 24. These will explode like $DELL did most likely.

♻️ RESHARE this post and write 1 comment, I'll DM the best $MU contract to get for earnings right now.

Reasons to follow me if you’re interested in $ONDS:

• I post daily $ONDS content and have done since November 2025. I’ve posted about $ONDS 1,993 times in 212 days, or on average 9.4 posts a day. No AI slop, just real updates.

• Bringing information to you even before press releases. World Cup 2026 contracts, Bundeswehr deployments, Firestorm investment, new product videos (Iron Wave), countless partnerships, new hires and hidden orders/deployments.

• Breaking news as soon as it hits the wire, simplified SEC filings without the legal jargon.

• In-depth content such as the full staff directory of $ONDS and their careers (400+ members of staff). The full list of known customers, partners and investments etc.

Happy to have you along if you’re following $ONDS. Always learning and sharing what I find.

5 Stocks under $20 I either own or am looking to Buy at today’s prices📈

1. Ondas $ONDS

• Stock Price: $9.06

• $50.12 million Q1 Revenue 1080% YoY🤯

• $457 million Backlog

Ondas is a defence tech company building around autonomous drones and wireless infrastructure. Has made 6 HUGE acquisitions in 2026 already.

SK Hynix just found a way to cool HBM memory from inside the package by cutting thermal resistance by 30% & paving the way for HBM5 stacking.

With SK Hynix already supplying a major share of next-gen HBM for $NVDA Rubin, this shows why memory is becoming a core AI performance.

$NOW Only 2000 shares of ServiceNow will make you a millionaire when the stock reaches $500 a share. I strongly believe it can achieve that in 2 years.

🚨 ServiceNow CEO Bill McDermott just dropped this on the AI hype:

“Most businesses don’t want to build workflow software for everything internally. They want one responsible AI Control Tower.”

ServiceNow is becoming the fabric connecting every hyperscaler, every LLM, systems of record and now full security (cybercrime = $1 Trillion/month problem).

True agentic enterprise is here: MoveWorks, VZA identity, Armis OT/security. Integrated major moves in just 20 days.

Jensen Huang ( $NVDA CEO) approves, they’re teaming up on the agentic future.

2030 Price Target: $1,200 – $2,000+ per share as they hit $30B+ revenue and own the enterprise AI operating system.

While others talk apocalypse, ServiceNow is building it.

$NOW to the moon.

Who’s loading up?

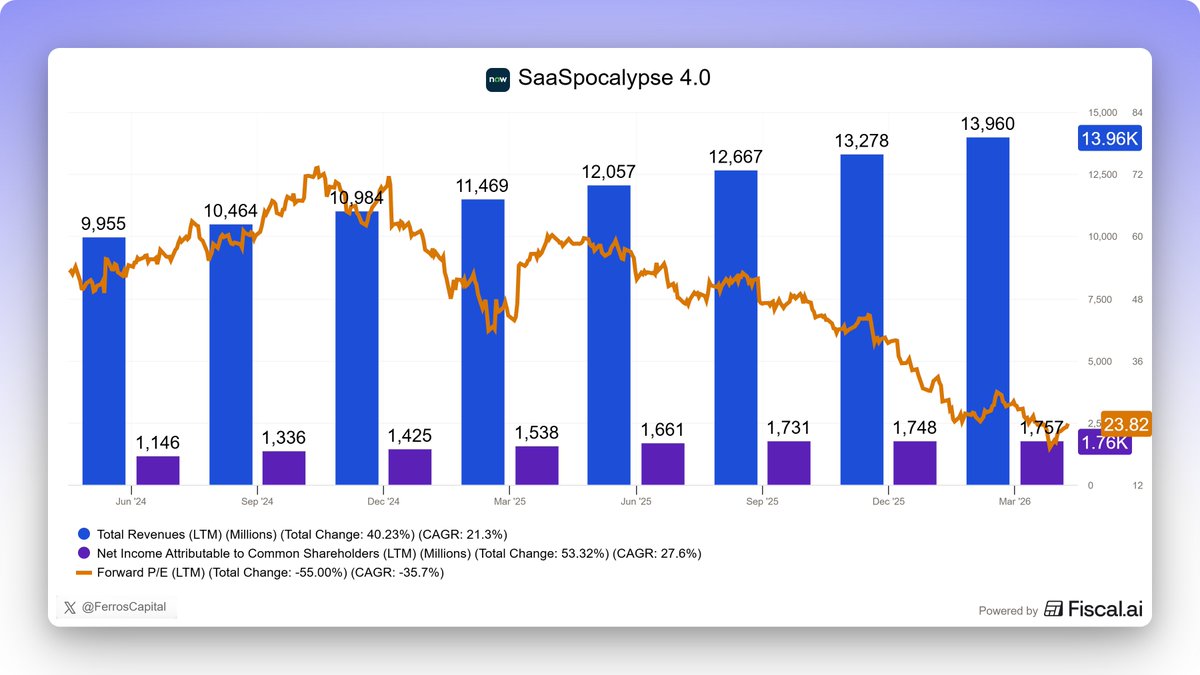

Wall Street’s SaaSpocalypse (4.0 Now!) is the most expensive delusion of 2026. I didn't think I would have to write this out but given the current Stock drop on $NOW , it seems appropriate.

Truthfully, I have never been in pure SaaS stocks besides $ADBE and $CRM for a short term years ago. Now, with the current re-rating from over 200$ per share to below 90$, this deserves my attention - and probably other investors too.

The whole panic thesis still assumes generative AI lowers the barrier to entry so drastically low, that Fortune 500s will fire all their SaaS vendors and build custom software with prompt engineers.

Let's actually audit $NOW (ServiceNow) to dismantle this mathematically and see if there is any merit to it.

1. Massive Enterprise Liability: LLMs are probabilistic engines. In mission-critical Tech, hallucinations can and will break systems. The more you have worked with AI, the more familiar this is to anyone reading this.

Equipping an entry-level developer with AI does not magically forge a master architect. Nor does it neutralize the immense gravity of legacy enterprise code. A sprawling architecture so complex that even the senior engineers who built it are usually terrified to alter it.

Unrestricted AI is a liability; governed AI can be a weapon.

2. Architectural Gravity: You don't rip out the operational nervous system of a global enterprise with a custom ChatGPT wrapper. ServiceNow’s moat isn't just code; it's decades worth of compliance, security, and integration logic.

Rebuilding that foundation requires an army of top-tier engineers. This structural moat applies equally to giants like $MSFT and other Software stocks. The barrier to entry hasn't fallen; the complexity of orchestration has exponentially increased.

3. The Physics of Compute: AI tokens burn massive capital. If you have scaled API infrastructure yourself, you know that token consumption obliterates budgets instantly. Even worse so at enterprise scale.

The foundational API providers (Anthropic, OpenAI) simply do not possess data center capacity to support this.

Even now, Anthropic is already putting restrictions on newer Models because they simply cannot service everyone, despite saying otherwise. ServiceNow already commands this infrastructure on optimized hyperscaler rails.

ServiceNow Chairman and CEO Bill McDermott's first sentences in the last earnings report were: "Since our founding, we’ve built our platform around the work customers need to accomplish. Today, they rely on ServiceNow to be their AI control tower for business reinvention." -> Enterprises demand an orchestration layer and $NOW is delivering.

Despite this, algorithms just wiped 16% off the stock over noise. Look at the actual Q1 reality:

• Remaining Performance Obligations (RPO) hit a staggering $27.7 Billion (+25% YoY). Enterprises aren't leaving; they are locking in for the next decade.

• Now Assist AI customers spending >$1M surged 130% YoY.

• The price collapsed to $86 at the time of writting. Against $4.17 Fwd 2026 EPS, the Forward P/E drops to 20.6x.

• Against a 20%+ Forward EPS CAGR, the PEG compresses to a flawless 1 (assuming they can keep up their EPS growth).

The workflow Software monopolies aren't dying. They are evolving into the ultimate AI toll-bridges. $NOW extracts the tax on the enterprise deployment of AI.

Compute is physically so constrained by HBM memory (Check out my $SKHynix thesis), enterprises are forced to rely on highly efficient, centralized platforms like $NOW to orchestrate their workflows.

Sooner or later, this negative Sentiment will pass - at least for $NOW. Are you buying the Dip?

Data & Chart by @fiscal_ai

$ONDS received an initial $10M order under a broader $50M Israel border demining award.

Including its separate Syria border project, Ondas now has about $80M in active demining tenders.

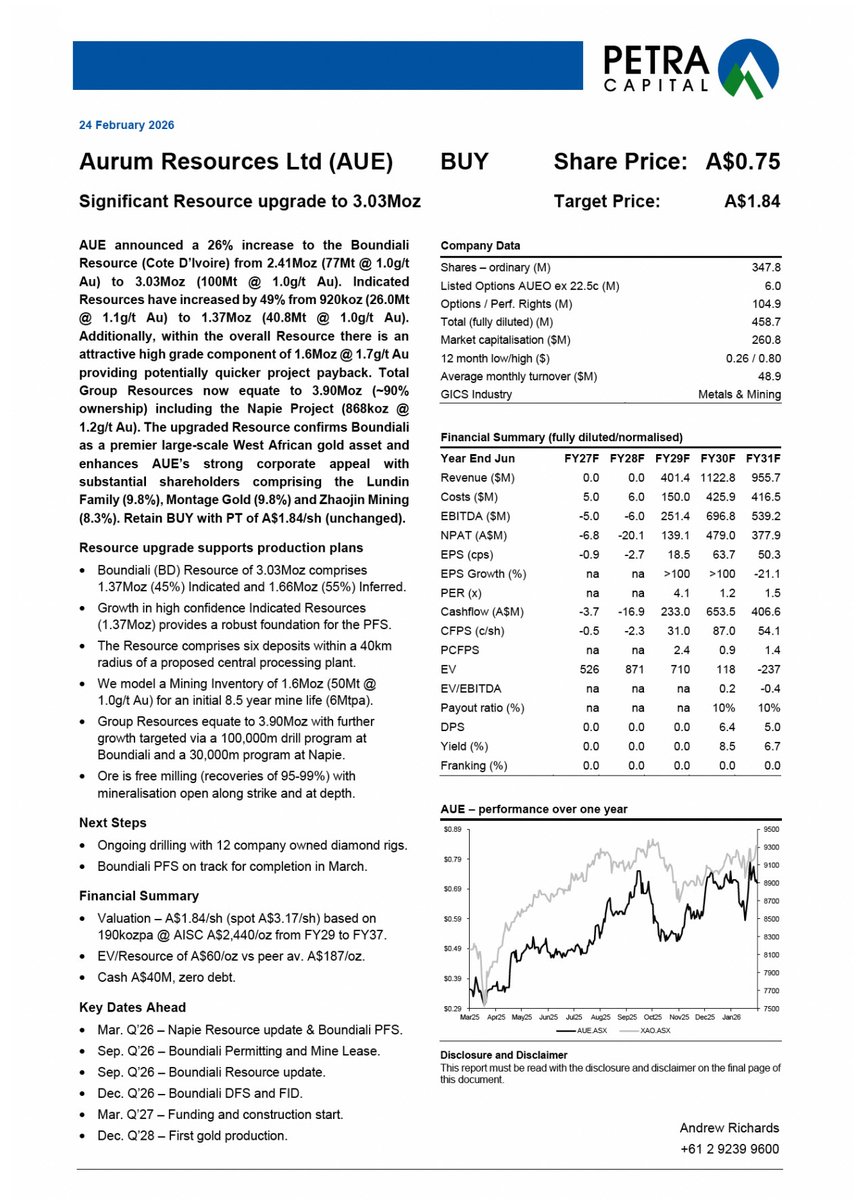

. @AurumResources (#ASX: $AUE) is rated BUY by Petra Capital with a $1.84 price target, implying ~188% upside to the current share price of $0.64.

The note follows a 26% increase in the Boundiali Resource to 3.03Moz, lifting total group resources to 3.90Moz including Napié. Petra says the upgrade confirms Boundiali as “a premier large scale West African gold asset”, with Indicated Resources increasing 49% to 1.37Moz.

The resource also includes 1.6Moz at 1.7g/t gold, a higher grade component that could support faster project payback. With 12 rigs drilling, a 100,000m program underway, and the Boundiali PFS due this quarter, Petra highlights strong momentum as the project continues to move toward development.

Full report here: https://t.co/IHWUk8r4Pl