What is everyone's thoughts on $BMI at 16x LTM EBITDA currently? Share Px -51% LTM (-28% YTD).

Seems like a great play on water, especially with accelerating water demand attributable to data centers. Performance appears at trough levels with a relatively flat FY26 and revenue growth re-accelerating to 8% in FY27.

Trough levels w/ favorable multiple + steady grower + income + end-market tailwinds

What am I missing? Anyone have thoughts? @Groundwork_HQ - I believe you have discussed it before.

Are companies like $XYL $VLTO just that much better?

@deanm0riarty@dwlz But I’ll give ya my thoughts. I had to log off the call at the 1hr mark to take GF car to car wash so need to finish reading whatever happened afterwards.

@deanm0riarty@dwlz I’ll give my thoughts later or tomorrow. I’m listening to the call right now. But tbh I don’t think I have missed anything. Listening to the call I’m convinced its position in AI is getting even stronger.

@junkbondanalyst These dudes might be the most brain dead humans I’ve seen. They are only looking ST and not considering the longer term damage. Throws really any chance of mending a relationship with Elon out the window

You are spot on. Quiet performers who post moderate, but consistent, growth outpace hype cycles, especially over long periods of time. It's a much better way to invest that is becoming increasingly less common as investors turn over rocks for the next "bottleneck" or "chokepoint" to try and make 10x in to days. Great companies like that, and many other industrial compounders, trade at premium multiples bc they have proven over long periods that they allocate capital efficiently and generate robust returns on capital, enriching shareholders. They built up goodwill with investors because of their track record.

$ESE continues to be a name that receives little attention on X, yet chugs along and puts up strong numbers.

Stock price is +57% since I highlighted the Company in Aug'25. ESE deserves more attention.

25.1x LTM EBITDA / 23.8x CFY EBITDA / 21.7x FY27 EBITDA - all pretty hefty multiples

FY27 is the more normalized EBITDA figure as revenue growth in the FYE 9/30/26 is expected ~20% due to M&A and revert back to the historical MSD in FY27.

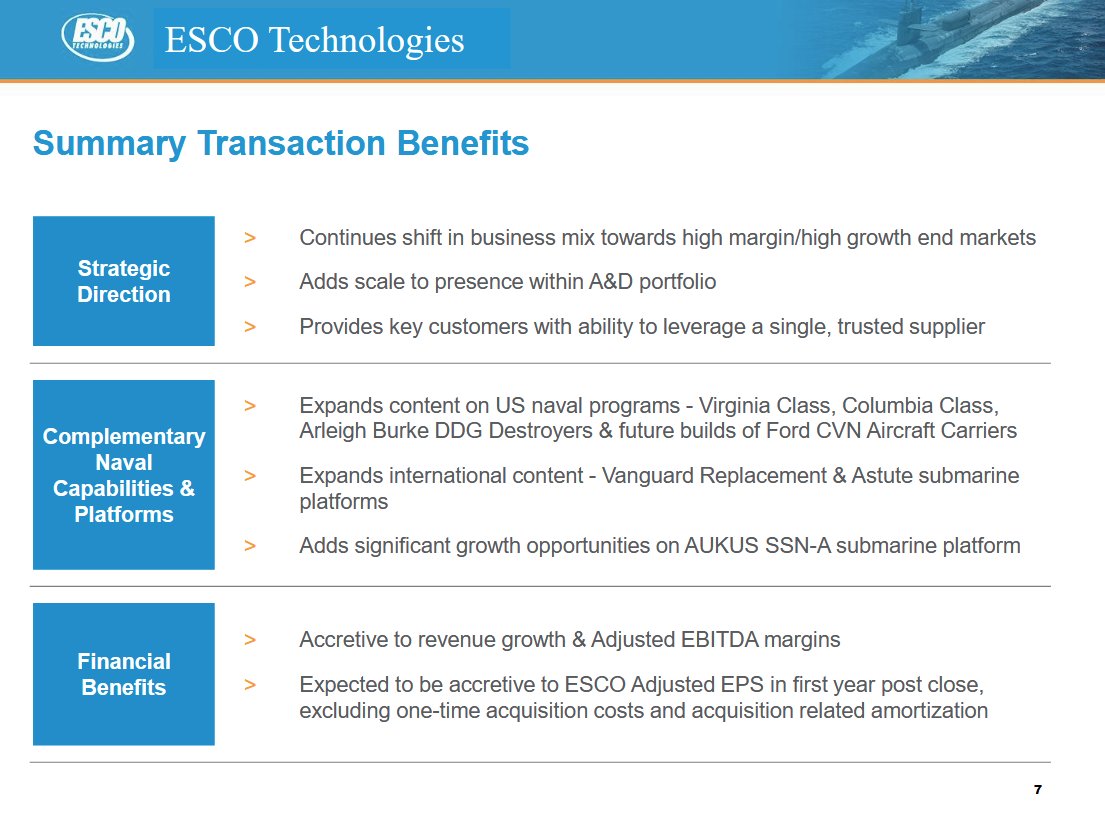

ESE done a great job of diversifying its business and adding content, especially on Navy Subs. On Subs it has made acquisitions to add content across the build cycle (vs. just earlier or at the end) to smooth earnings. Also has Missile exposure.

> Utility Solutions segment - develops, manufactures, and delivers diagnostic testing solutions and decision support tools for the renewable energy industry, primarily wind and solar. The segment provides exposure to the AI build out especially as solar growth is anticipated to accelerate due to its LCOE and the shortest amount of time to get a project up n running.

I continue to love the business and will monitor it closely for a pullback. Worth checking out and doing DD on.

$ESE UTR biz I forgot about and circling back. If you can't tell, I love IndustrialCos w/ A&D tilt esp Navy, AF, missiles.

Recent acq. of SM&P is game changing as it:

🔹 Increases content on submarines

🔹 Gains exposure to UK Royal Navy (subs & surface) & U.S. surface fleet

🔹 OEM & Aftermarket + Recurring revenue & accretive margins

🔹Large backlog

🔹 Smooths out revenue across the ship/sub build cycle (SM&P products = early in build + ESE = later in build)

Europe / EU is always so far behind the U.S., it's astonishing. They can never really lead in anything with such a regulatory burden and general unwillingness to support start-ups / high growth industries. Though, it appears there are some pockets that are starting to at least partially course correct.