This year I present a handful of my top ideas for 2026 (in alphabetical order of tickers). Some of these names are fairly uncorrelated with the market (and a few definitely are not). As a reminder please do your own work and be mindful of the low trading liquidity in many of these.

$BWEL JG Boswell at $459/share (LOW RISK / HIGH REWARD)

JG Boswell has been the deep value stock that even the most disciplined investors have lost patience with (including yours truly!). Despite the last year being horrible for both tomatoes and cotton, $BWEL put up ~$40mm of adj. EBITDA. It is extremely rare for both of its core crops to be bad at the same time (i.e., something good should happen with one of them this year) and their pistachio crop will generate increasingly material cash flow for the next 10 years as it matures. Creation value per acre is around ~$3k (or lower) depending on your assumptions which compares to FMV of $15k/acre. There's a lot of room for the stock to appreciate and still trade poorly!

$MLP Maui Land & Pineapple at $17 (LOW RISK / HIGH REWARD)

This name has seen a recent cluster of insider buying by the CEO (Race Randle), Chairman (Scot Sellers) and controling shareholder (Steve Case). The company's undiscounted land value is ridiuclously high relative to its stock price (like 8-15x) but the open question is the time to monetize. In a frothy stock market, this seems like an interesting, low risk place to deploy capital.

$PLAY Dave & Buster's at $16 (MEDIUM RISK / VERY HIGH REWARD)

Dave & Buster's is in the midst of a turnaround, with tangible signs of progress, but an exasperated investor base. Valuation is ~4.5x EBITDA which compares to its long history of 6-10x+ EBITDA. It's also worth pointing out that within this business is a bowling business called Main Event which is ~half of the company's TEV and worth ~8-10x if sold separately. $PLAY is going through a capital intensive remodel phase (with mixed results). The company recently put in a new CEO and results are turning, but the street is rightly worried about the staying power of the improvement. 2026 could be disappointing on the topline, but my gut is that there is a lot of low hanging fruit that will result in nicely improving results in 2026. There are no near-term liquidity issues and this is a nice multi-year option. I think it's highly asymmetric, wherein downside should be limited given b/s duration + low hanging fruit on costs with colossal upside on any real turnaround (every ~1x EV/EBITDA revaluation upward is around 100% on the stock). Don't waste your time on this one if you can't handle the volatility.

$TIPT Tiptree at $18.27 (SAFE PLACE TO PARK CASH)

This is by far my lowest beta pick. $TIPT is essentially doing the opposite of a de-SPAC. It is morphing from an operating company to a cash shell. It has agreements to sell its assets and will have $24.60/share in net tangible book value upon closing of Fortegra in 1H26. Post closing, the company will return the cash, make a large acquisition or a combination thereof. One of $TIPT's directors recently bought stock at $18.21/share and most importantly insiders own ~35% of the company. Upon completion of the Fortegra divestiture, I expect this to pull toward 85-95% of TBV ($20.91-23.37/share) representing a 14-28% return. Further upside potential when they announce an acquisition. If this were a true SPAC (with a 24 month put) I think this management team would trade at a premium.

$WEBC Webco at $218 (warning: VERY ILLIQUID)

Webco ended the year near its ATH, however, it is incredibly cheap at ~0.5x TBV and ~4x EBITDA. About a year ago, the company did a privately negotiated buyback of ~15% of its stock at $200, which was a premium to the prevailing $185/share trading price. No surprise, but in the last few quarters, the results have turned and the company should generate meaningful FCF in 2026. I believe the take private valuation for this company is ~$350-400/share.

And a few other old favorites that I'll throw in here:

$CBBI CBB Bancorp at $11 (LOW RISK + HIGH REWARD)

This name has been discussed on FinX extensively and I'm not going to break new ground here. But I will say that the new board member gives me some hope that something will happen in the name in the short-term.

$FMBL at $8,349 + $QUCT at $2,100. (LOW RISK)

Both of these names had an amazing 2025 due to the company taking shareholder friendly actions (for FMBL, raising a $200mm pref, for QUCT signalling asset sales and having improved results). Both of these names continue to very cheap relative to their take private valuations. And, due to conservatively positioned balance sheets they both have little downside.

$FPH at $5.59 (LOW RISK + HIGH REWARD)

It feels like hubris to re-recommend $FPH as a top pick for the upcoming year and I do think that at this price it's not as interesting (obviously). However, there are a lot of good catalysts coming with this name, including the announcement of JV partners in both Valencia and SF and the potential favorable resolution of the litigation against $TTEK (in addition to continued high value land sales in Irvine). $10-15/share continues to be where I think this goes to over time.

Wild to me that when $MAPS was trading 2x higher, it was a seemingly beloved consensus long on here, and now due to STRATEGIC delisting it's traded off massively, sits at net cash, all while generating $40 mm of EBITDA.

$WEBC, a very illiquid OTC name, is worth attention. $181/$195 right now. One month ago when $WEBC was $160-170, the company paid a sizable premium to buy back 17% of the company's stock at $200/share (in a block trade), bringing the Weber family's ownership from 65% to 79%.

One analogous situation I can think of is $MCEM. Several years ago $MCEM was trading in the 60s, and the company did a dutch tender at a premium to acquire shares. We all know what happened after that.

While $MCEM was in retrospect incredibly cheap, $WEBC is by no means expensive. Additionally, I am struggling to find a counterexample of an OTC company buying back stock at a premium, and then not doing very well.

Maybe the Weber family knows something we don't. Given they already control this thing, I don't see a non-economic reason to further consolidate their ownership.

$TIPT filed an 8-K this morning where they said they expected the Fortegra deal to close by Friday 5/29. Pro forma TBV is ~$24/share, stock last 17.17.

Another great quarter from $WEBC with accelerating top line and gross margin expansion. Company continues to buy back and refresh buyback.

https://t.co/w22AeWh2pH

$WEBC reports continued improvement in results, with large yoy increases in revenues, gross margin and earnings. They stepped up buybacks again in the quarter, repurchasing 15k shares (~2% O/S).

$TIPT filed an 8-K this morning where they said they expected the Fortegra deal to close by Friday 5/29. Pro forma TBV is ~$24/share, stock last 17.17.

I don't know if I fully agree with that. $CBBI trades at 0.4x for two reasons: 1) OTC listing and 2) no buyback. If there was a company sponsored buyback, it would probably trade at 0.6-0.7x and therefore the buybacks would be less accretive.

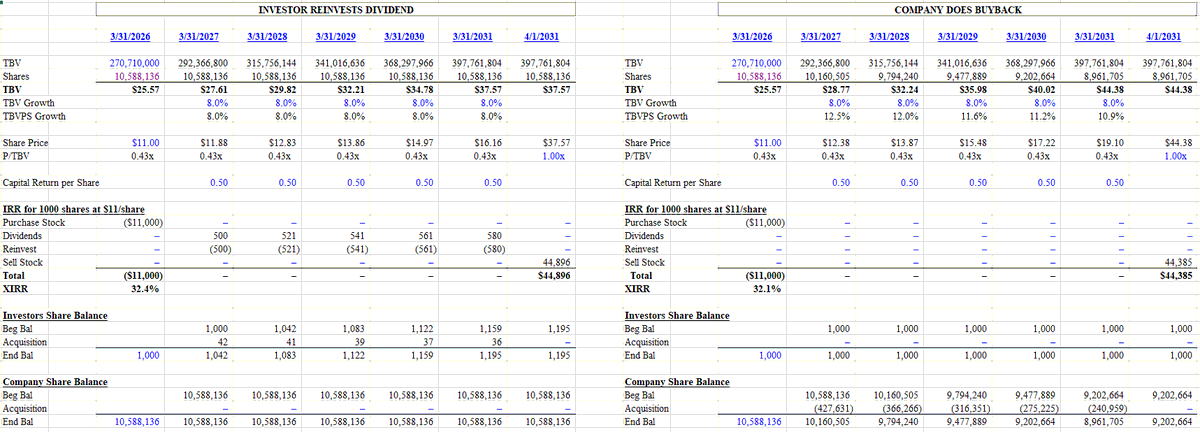

Also if you look at my numbers you'll see that the projected share price in the non-buyback scenario is $16.16 in five years plus $2.50 in dividends vs. $19.10 in the buyback scenario. Pretty close.

If you're a short-term holder, you want the buyback to re-rate this to 0.6-0.7x. If you want to long-term compound, it's not clear the buyback is that much better to me.

$CBBI followers- the tables below show two scenarios assuming a sale in 5 years at 100% of TBV:

1) Investor reinvests the .50/yr dividend into more shares

2) CBBI suspends dividend and instead does a share repurchase

The analysis shows that the results are roughly the same (BEFORE TAXES). The point here is to show that if you reinvest your dividend you can somewhat replicate the economics of a buyback. One assumption that is likely optimistic in the company buyback scenario is that they'd continue to be able to buy back at 0.4x TBV. If you tinker with that, the buyback is less valuable.

cc: @mwphnh

I’m going to send you a spreadsheet later which will lay it out. The cheap stock price is a gift to investors. If they were more aggressive on a buyback, the stock would trade higher and the buybacks wouldn’t be as accretive. If you take your after tax dividend and buy back stock at sub 0.5x TBV you will do very well.

$CBBI continues to do its thing. TBVPS up to $25.57/share. Run-rate earnings probably around $2 implying a mid 5x P/E. If you don't like the lack of buyback, reinvest the dividend into more shares. Biggest discount of its peers due to OTC listing and lack of buyback.

$OPBK raises dividend and reports slight improvement in EPS vs. last quarter. Seems to be trading in the mid 7s P/E.

$PCB reports and trading maybe in the 8s on P/E.

$HAFC trading around 10x P/E and hitting ATH. A premium vs $OPBK and $PCB for a larger balance sheet.

All very cheap.

@mwphnh The ratios won’t change - you’re right about that, but you can replicate the economics by reinvesting the dividend (adjusting for dividend taxes).

@leevalueroach I opened up the 10-Q files today and looking at footnote 5. It shows 110mm S/O, which includes 5mm shares associated with the the HDFS business.