@GSTReckoner@GSTATofficial@gstat but filing was enabled on 18 December 2025, GSTAT shall not be at fault that majority people are filing during the last days.

The position will be same even if date is extended.

The GSTAT does not have any jurisdiction to extend the last day of filing #limitation.

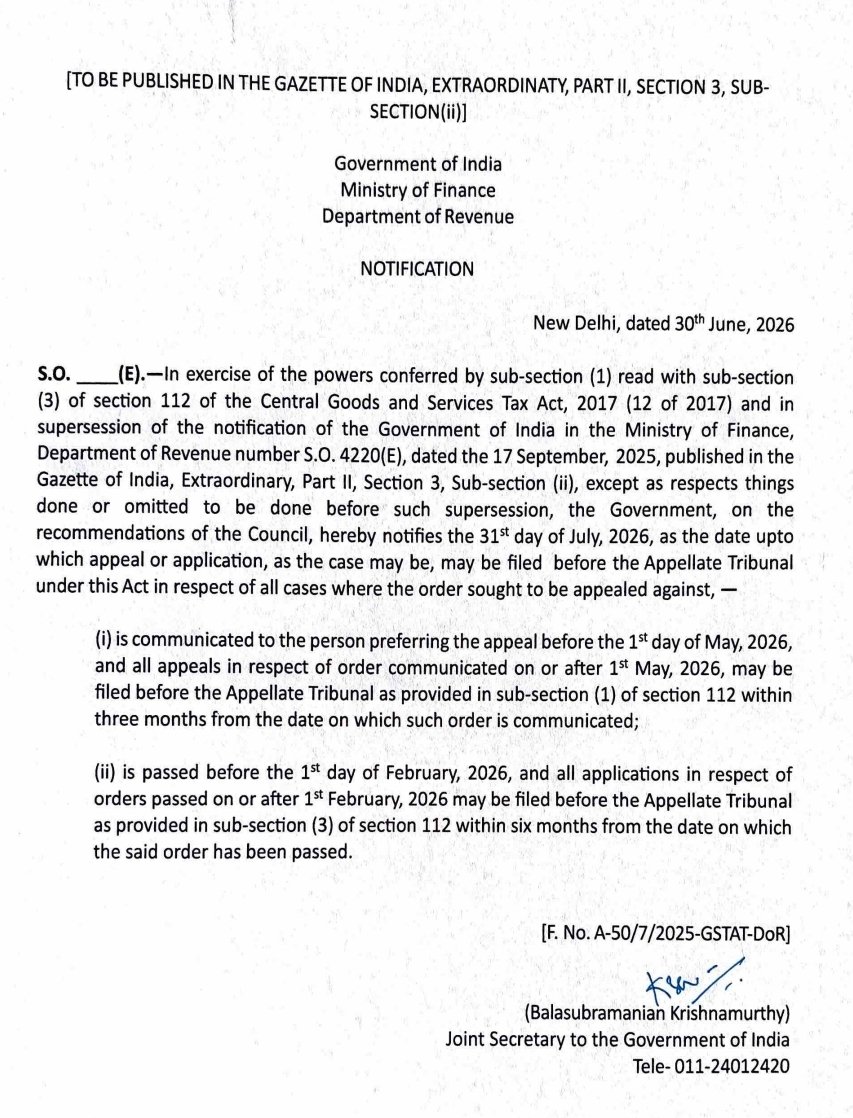

It is therefore urged that all the Tax Payers/Tax Officials-Appellant should file their second Appeal under Section 112 of the CGST Act before 30th June 2026 to avoid last minute rush.

#GSTAT

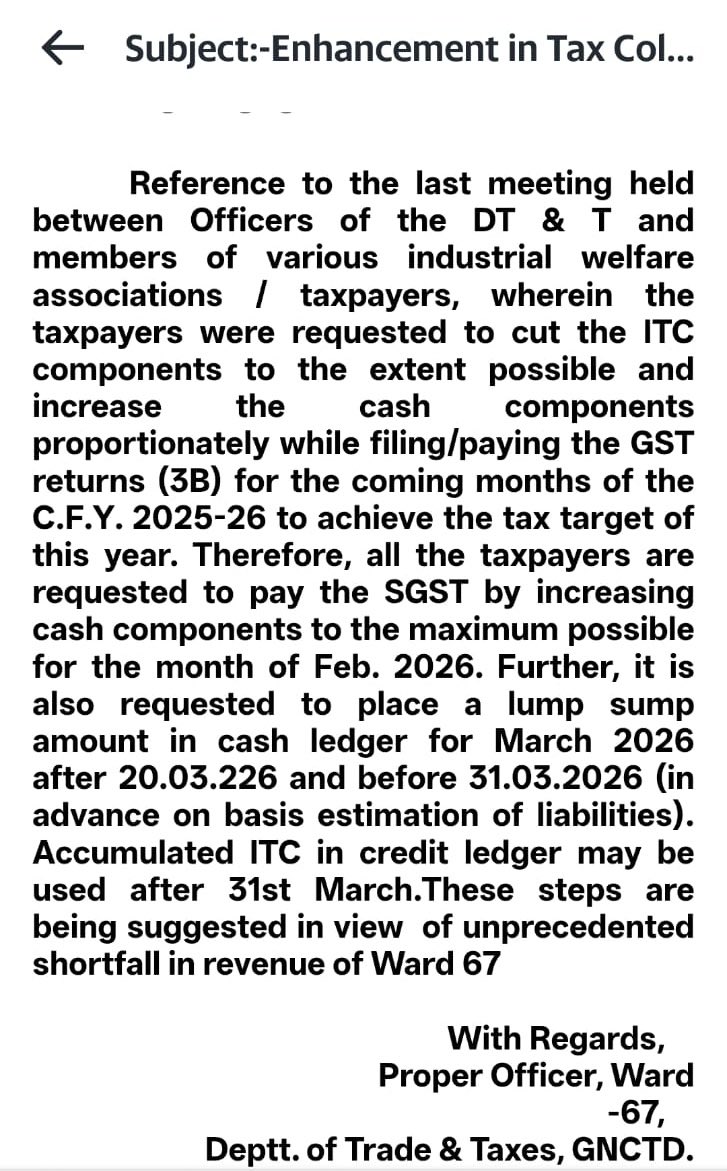

@PratibhaGoyal Officers are calling and pressurising taxpayers to deposit money in cash ledger just to meet target, its completely illegal. GST law has no concept of advance tax.

How will a Director pay 10% pre-deposit, when penalty is imposed on him, and he’s not even registered under GST? 🤯

As From 1 Oct 2025, law is clear 👇

👉 10% pre-deposit is mandatory where only penalty has been demanded without involving demand of tax.(Sec 107(6) of the CGST Act).

And in practice, along with demand on the company,

a separate penalty is often imposed on Directors/Partners for alleged involvement (aid/abetment, etc.)

Now think about this situation:

Penalty is imposed on Directors/Partners, who are:

❌ Not registered under GST; and

❌ Not even liable to take registration

So practically… how the payment shall be done?

I dealt with this recently, and here’s the exact workaround that worked:

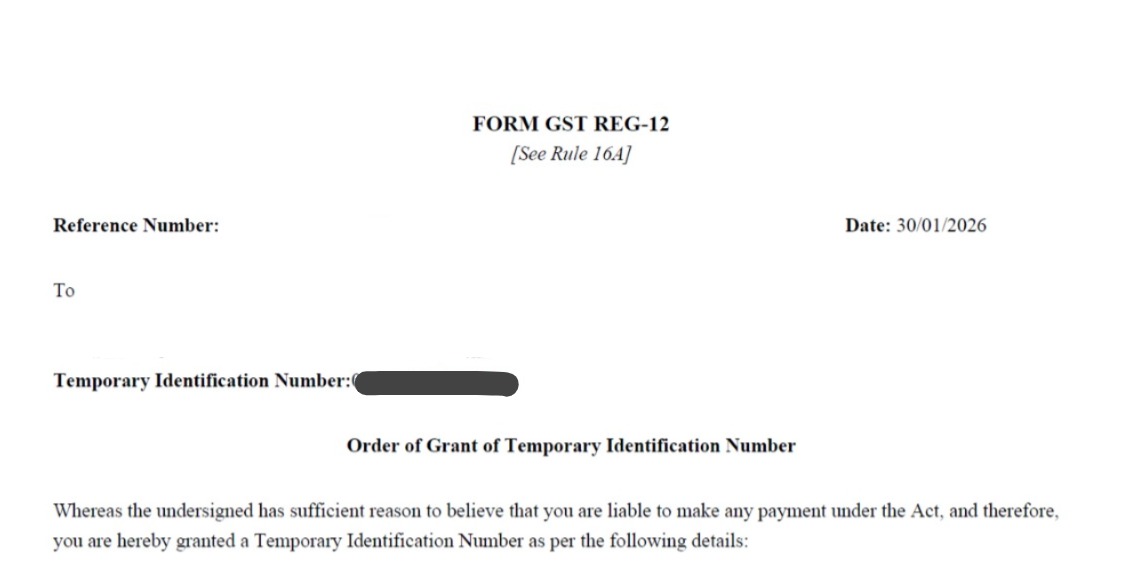

👉 Department (of director's residential jurisdiction) can do suo-moto registration

What I did:

✔️ Filed a letter to jurisdictional officer

✔️ Got Temporary Identification Number (TIN)

✔️ Login ID & Password generated

✔️ Paid 10% pre-deposit in Cash Ledger

✔️ Adjusted via DRC-03

✔️ Attached the said DRC-03 with the appeal filed manually

🎯 For the said purpose, I’ve drafted the TIN request letter.

👉 Follow me & DM “TIN”, I’ll share the Ms Word file of the same with you

#GST #GSTAppeal #TaxLitigation #CA #IndirectTax #GSTIndia

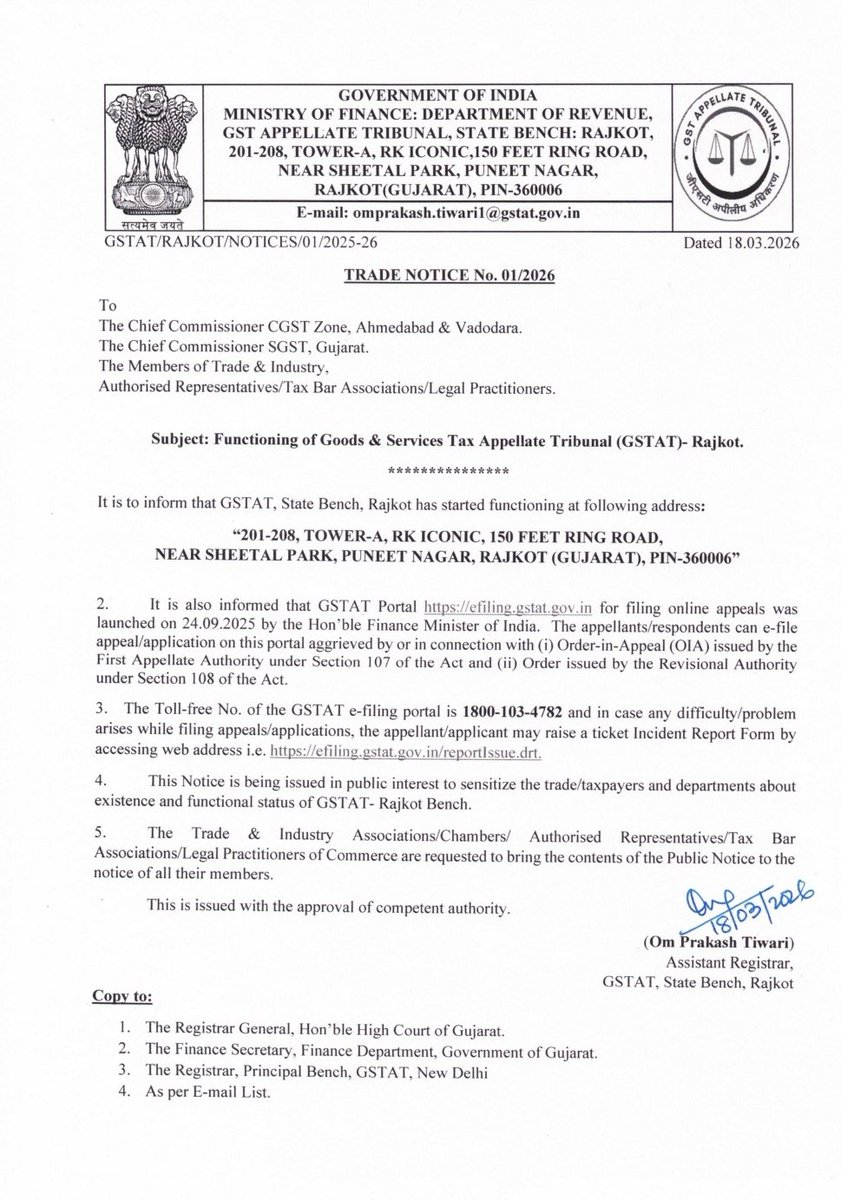

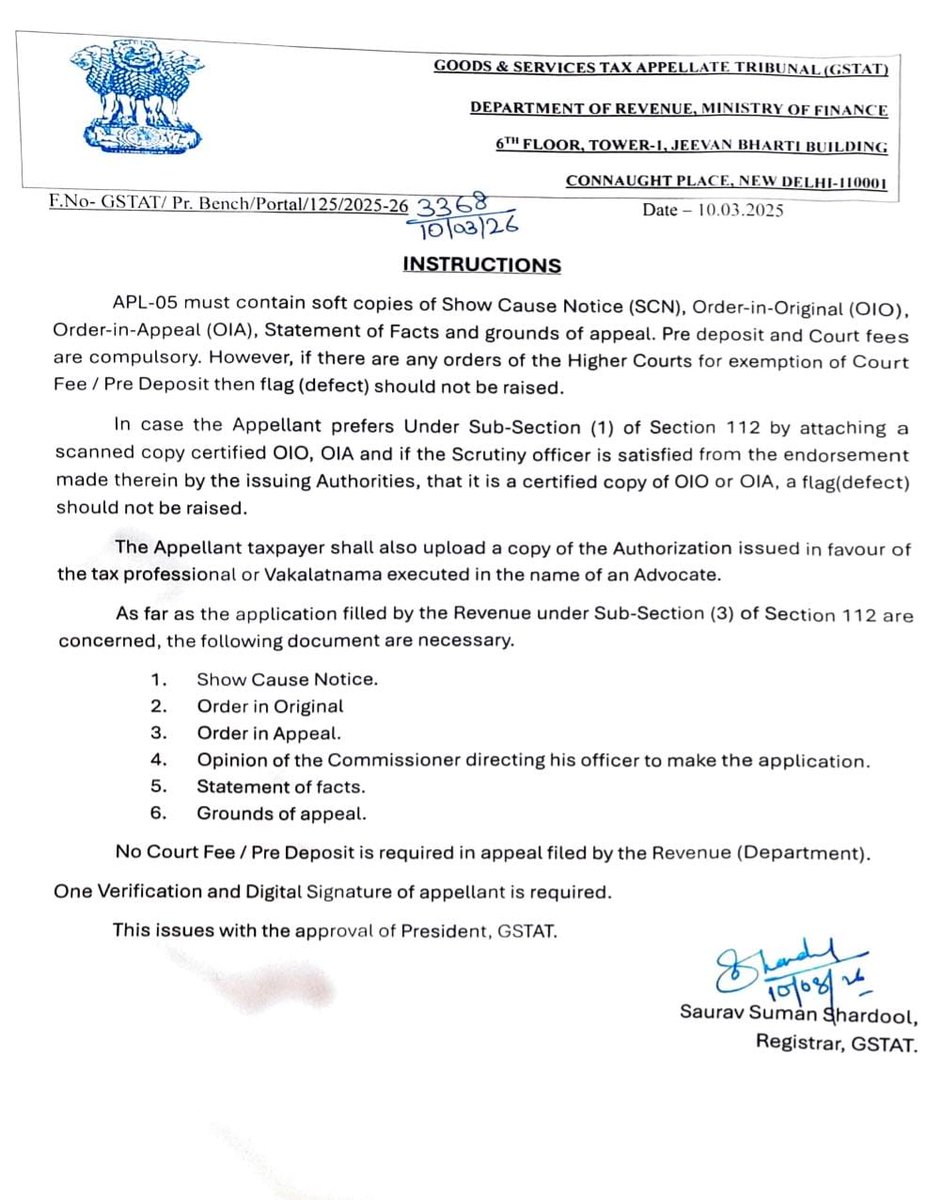

APL-05 filing before GSTAT requires uploading key documents including SCN, OIO, OIA, statement of facts, and grounds of appeal, along with mandatory pre-deposit and court fee (except where exempted by higher courts).

Certified copies of orders and authorization/vakalatnama must also be submitted.

For departmental appeals, no pre-deposit or court fee is required, and the application must include specified documents and a digital verification.

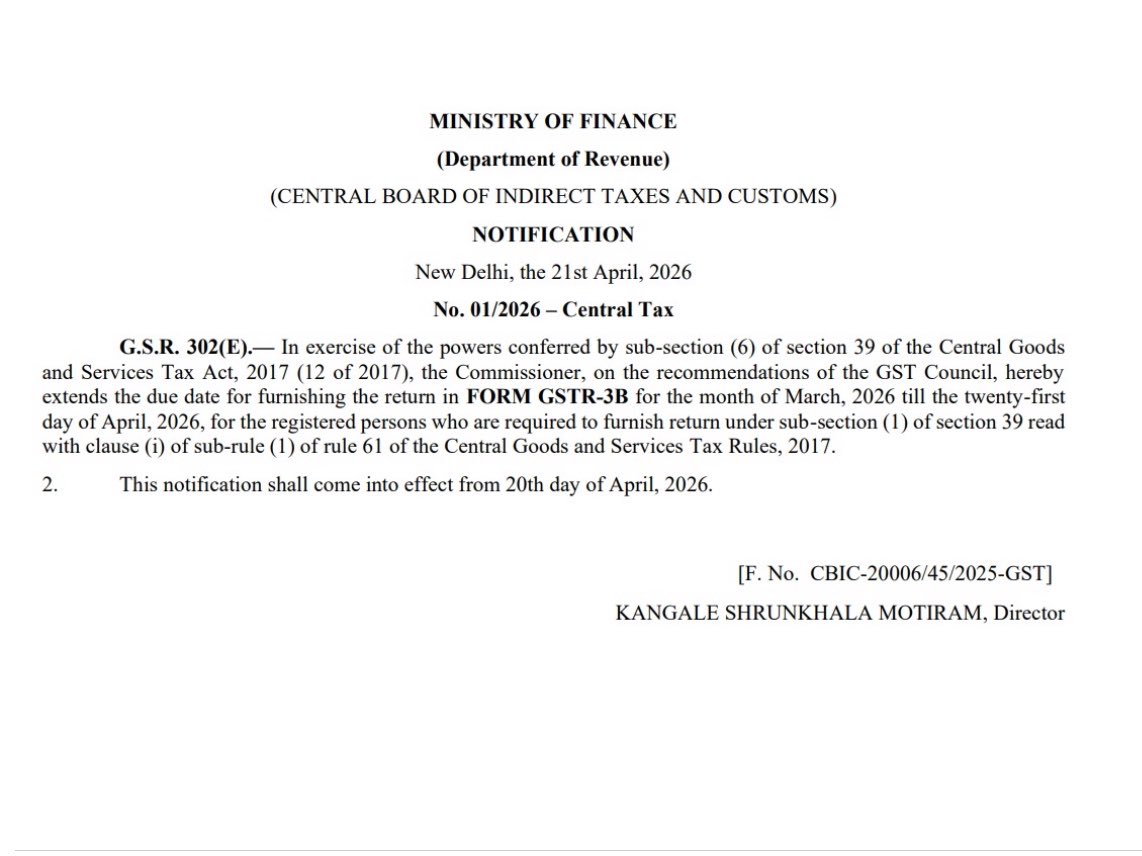

From February 2026 tax period onwards, the GST portal will auto-populate the “Tax Liability Breakup, As Applicable” in GSTR-3B based on document dates reported in GSTR-1/GSTR-1A/IFF.

Taxpayers are required to open the tab on the payment page and confirm the breakup by clicking “SAVE” before filing GSTR-3B through EVC/DSC.

Until the portal issue is resolved, taxpayers must manually open the tab and save the confirmation to complete filing of GSTR-3B.

⚠️ Paid FULL GST demand 'Under Protest', however the portal still asking for 10% pre-deposit while filing the appeal? You don’t need to pay again.

📌 Many taxpayers & professionals miss this small step.

Example 👇

Demand Order: ₹1,00,000

Taxpayer pays ₹1,00,000 under protest (to avoid future interest).

While filing appeal:

Disputed Amount: ₹1,00,000

Pre-deposit (10%): ₹10,000

➡️ Portal asks to pay ₹10,000 again.

But why pay again if ₹1,00,000 is already paid?

❗Reason: Payment through DRC-03 is not linked with the Demand ID (DRC-07) on the GST portal.

💡 Simple Fix:

File DRC-03A and link the earlier DRC-03 payment with the Demand ID.

Once linked:

✔ Portal considers it as amount paid towards admitted + pre-deposit

✔ Balance payable becomes ₹0

✔ Appeal can be filed without paying the amount twice

👉 Can refer the advisory here:

https://t.co/HP6TwpojqH

#GST #GSTAppeal #TaxLitigation #GSTPortal #DRC03

📌 GSTAT Delhi | Sterling & Wilson Pvt. Ltd. vs Commissioner (Odisha GST)

▶️In a landmark development, Principal Bench, GSTAT delivered its first judgment in Second Appeal on 11.02.2026.

▶️The case was heard online in a paperless manner and the judgement is uploaded today i.e. 12.02.2026 on GSTAT portal.

▶️https://t.co/zsrSGVMG6n

🗓 Order dated: 11.02.2026

🔍 Issue:

Demand raised due to mismatch between GSTR-1 vs GSTR-3B for FY 2018–19.

Alleged short payment: ₹27.06 lakh + interest + penalty.

🧾 Taxpayer’s defence:

Mismatch occurred due to:

✔ Credit/debit notes adjustments

✔ Advance tax adjustments of prior periods

✔ Technical/system constraints in early GST regime

✔All transactions were duly recorded in books — no fraud, supression.

✅ Final Outcome:

➡️ Orders under Section 73 (tax/interest/penalty) set aside to that extent.

➡️ Matter remanded back to Proper Officer for fresh adjudication.

➡️ Appellant allowed to file amendment/reconciliation application within 30 days.

➡️ Proper Officer to verify genuineness of credit/debit notes and pass fresh order.