@hell0men@_SEAL_Org +1 on the people side. process audits rarely include actor-level threat modelling (devops, oracle ops, gov signers), they usually stop at access-control. LlamaRisk is already moving this way on collateral onboarding, extending to people would be the next step.

@realCoinAPI yeah. logic exploits collapsed because audits + formal proofs caught the obvious math holes. but supply chain (DVN configs, bridge layers, deployer keys, dependency hijacks) is where the value sits now. the surface migrated, not shrunk.

@oSaaT2 right, the soft-liq is the actual primitive that breaks the Aave mental model: borrower stays in the position during the band slide, repays inside the AMM, position auto-unwinds. no forced sale, no liquidator profit extraction.

LlamaLend vs Spark USDS, on-chain right now.

3 whales hold $26M+ in crvUSD debt at 0.4-1.1% APY on LlamaLend. On Spark USDS, the ask for the same dollar is 4.08%.

Even across the two clean borrowers alone, that's $16.6k/mo in savings - 3.6x cheaper on a fair 7-day average.

Addresses and the rate mechanic below.

twocrypto factory got a fresh impl queued via @CurveFinance prop 1408. covers every donation pool, FX + YB alike. headline 'less arb value at rebalances' is the LP-side win: more fee stays in pool, less leaks to MEV every reweighting. https://t.co/fia7ysaIqI

@fraxfinance Tangent pre-deposits open in a week. frxUSD as default stable, sitting on @CurveFinance PegKeeper pools as the cold-start liquidity layer. interesting part: whether frxUSD/USDC float stays 50/50 once tangent vaults size up, or skews toward frxUSD.

Net effect for AAVE holders:

• Gross irreversible cost: 25k ETH (DAO donation)

• Structural liability: up to 30k ETH to Mantle (with repayment)

• Buybacks paused until Mantle clears

• Surplus from extra donations (~24.5k overshoot) → accelerates Mantle close

Sources: Aave governance ARFC + DefiLlama fees + TokenLogic Snapshot

When can AAVE return to buybacks?

TokenLogic's Snapshot proposal pauses AAVE buybacks until Mantle's credit facility is repaid. So the question becomes: how fast can Aave revenue clear that debt?

Bailout structure + repayment math below ↓

Mantle repayment timeline (Aave DAO revenue → Mantle credit):

Last 30d fees: $62.4M (DefiLlama). Annualized ~$760M gross, ~$80M DAO revenue at avg reserve factor.

Mantle facility: 30k ETH ≈ $84M @ ETH $2.8k.

Bear (TVL -40%, low borrow): ~18-24 mo

Base (current rates): ~10-12 mo

Bull (TVL +60%, GHO uptake): ~6-7 mo

ETH price exposure: 30k ETH is principal — ETH 2x → timeline 2x at flat USD revenue.

Clean two-borrower recap:

Combined debt: $6.75M

LlamaLend 7d-TWA cost: $6,368/mo

Spark USDS 4.08% cost: $22,950/mo

Savings: $16,582/mo. 3.6x cheaper even on the fair weekly average.

The spread is in the rate, not the narrative.

Sources: https://t.co/OfX0LZWya2 (7d snapshots), Spark Pool.getReserveData on-chain, controller.user_state.

Why the rate is this low, and why it no longer spikes overnight.

Borrow rate on LlamaLend moves with utilization + PegKeeper monetary policy. Historically the cheap to spike swings were brutal: the WBTC chart shows a peak to ~46% in Feb.

Governance then shipped a sequence of smoothing upgrades: EMA(9d) on the mint rate, TargetFraction retune, rate0 cuts. Result on WBTC: post-EMA the rate collapsed to a flat ~14% band overnight, and subsequent tweaks walked the mean down 14, 11, 7, ~1% today.

The policy is unified by crvUSD peg pressure, so markets track each other (WBTC / wstETH / WETH / tBTC), only per-market utilization bumps them apart.

crvUSD circulating on Ethereum: $234M -> $327M in 14 days. +40%.

Yesterday alone: +$58M.

The headline hides three different stories underneath.

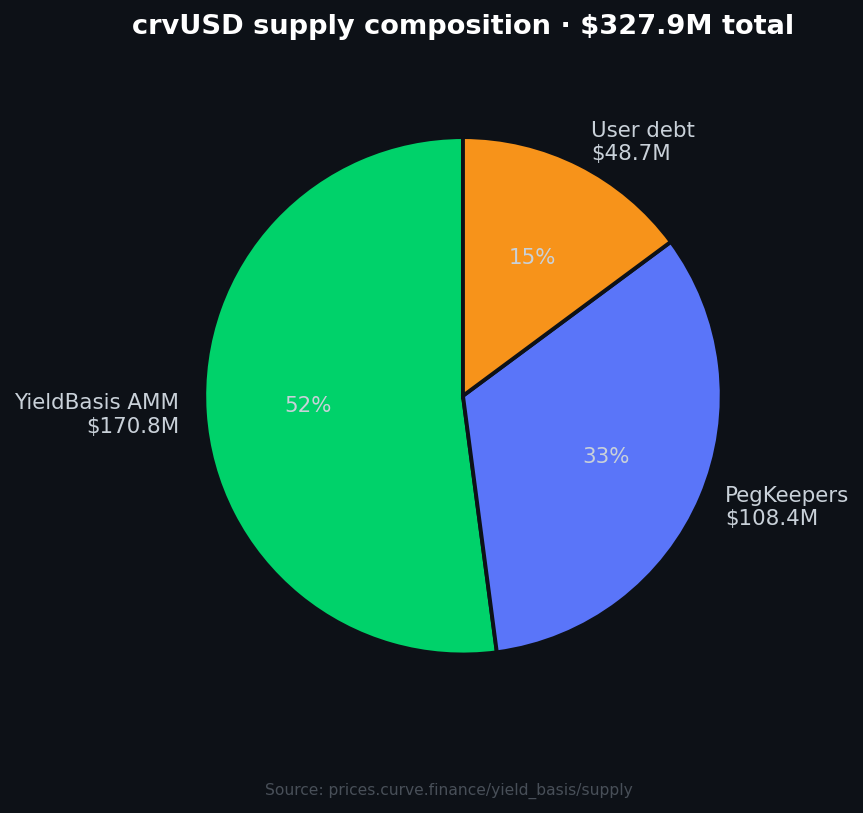

Supply composition ($327.9M total):

• YieldBasis AMM $170.8M 52%

• PegKeepers $108.4M 33%

• User borrowing $48.7M 15%

Most new supply is system mint. Not retail frenzy.

But the user debt bucket tells a different story.

$19.3M -> $48.7M in 14 days. +152%. That IS frenzy.

Where the new debt went:

• wstETH $1.7M -> $17.3M +914%

• weETH $0.14M -> $10.1M +6900%

• tBTC $3.5M -> $4.7M +34%

• WBTC $10.4M -> $12.8M +23%

• sfrxETH $0.83M -> $1.1M +35%

• cbBTC $0.81M -> $1.06M +32%

• WETH $1.8M -> $1.5M -18%

LSTs swallow the flow. Plain ETH shrinks. BTC derivatives quietly compound.

Yesterday's biggest single move:

Address 0xee2..68 deposited 5,315 weETH ($13.5M) and minted $10M crvUSD in one transaction. Health 22.27, ultra-safe LTV.

They immediately swapped $8.3M crvUSD for USDC, pressuring the peg enough that PegKeepers auto-released ~$20M crvUSD over the next 5 minutes to rebalance.

One whale + system response = roughly $30M of yesterday's $58M supply move.

The story isn't "crvUSD pumped."

LST collateral market is maturing. Real leverage gets borrowed against staked ETH. The system absorbs it gracefully, as it was designed to.

#crvUSD #Curve #DeFi #LST #stablecoin

7/ Simplicity is a security property.

Fewer moving parts = smaller attack surface. Curve crvUSD vs restake-over-bridge: the number of trust layers is the risk profile.

Minimal trust set is a design decision, not an optimization. Boring is alpha in 2026.

Invariants, not features.

What breaks repeatedly across DeFi incidents 2022-2026. Not a fix-list, a map of the rakes.

v0.1, 7 tweets. Rough, unfiltered. Push back.

6/ Cross-asset freeze treats the symptom.

Aave froze WETH borrow on Core, Prime, Arbitrum, Base, Mantle, Linea after rsETH broke. Rational damage control. Also proof that risk rating and lending exposure are structurally decoupled.