Tally has introduced a new AI-powered feature called Tally IRA, which lets you upload your purchase invoices (PDFs or images) and automatically generate accounting entries after a simple mapping process.

How to access Tally IRA:

1. Ensure you have an active TSS (Tally Software Services) subscription.

2. Search for "Tally IRA" on Google and open the portal.

3. Log in using your Tally credentials.

4. Once activated, the plugin will automatically appear in Tally. You can verify this by going to Help → Tally Plugins.

5. To import invoices, go to Import → Transactions, upload your invoice (PDF/Image), complete the required field mapping, and Tally IRA will automatically create the accounting entries for you.

That's it, your purchase entries are ready in just a few clicks.

ITC can not be denied, based solely on retrospective cancellation of supplier's GST registration

🎥 Watch Short Video: https://t.co/4uNrJj3MOt

• The Madras High Court held that Input Tax Credit (ITC) cannot be denied solely because the supplier’s GST registration was cancelled retrospectively. Where the supplier was a validly registered taxpayer on the date of the transaction, retrospective cancellation by itself is not sufficient to reject the recipient’s ITC claim.

• The Court observed that the impugned orders primarily relied on the retrospective cancellation of the supplier’s registration, without independently examining whether the underlying supplies were genuine and actually received by the recipient. Such an approach was held to be legally unsustainable.

• Reaffirming its earlier ruling in Engineering Tools Corporation, the Court emphasized that GST authorities must verify the authenticity of transactions by examining supporting evidence such as tax invoices, e-way bills, lorry receipts, transport documents, and other records demonstrating actual movement and receipt of goods.

• While the Revenue argued that certain invoices were issued after the supplier’s cancellation and that adequate proof of receipt of goods had not been furnished, the Court noted that most transactions had occurred before the cancellation order was passed. Therefore, a detailed factual verification of the transactions was necessary before denying ITC.

• Accordingly, the High Court set aside the assessment orders relating to the relevant tax periods and remanded the matters for fresh adjudication. The authorities were directed to reconsider the ITC claims on merits, provide the assessee a reasonable opportunity of hearing, and pass fresh orders in accordance with law within the prescribed timeframe.

Madras HC - Fathima Traders vs Deputy Commercial Tax Officer [WP Nos. 22419, 22420, &22422 OF 2023]

Has the Income-tax Act, 2025 quietly expanded Tax Audit applicability for small businesses? YES!!

Section 58(3) now provides that where an eligible presumptive taxpayer declares profit below 6%/8% and total income exceeds the basic exemption limit, maintenance of books and Tax Audit becomes mandatory.

Under the post-2016 Section 44AD regime, many taxpayers with turnover below ₹1 crore could avoid audit unless the specific 5-year lock-in condition of Section 44AD was triggered.

Take a small shopkeeper with ₹80 lakh turnover and 4% actual profit. Under a literal reading, Tax Audit becomes mandatory despite turnover being below ₹1 crore.

But the bigger impact may be on salaried taxpayers doing F&O trading!

Example:

Salary Income: ₹25 lakh

F&O Turnover: ₹80 lakh

F&O Profit: ₹50,000

Since total income exceeds the basic exemption limit due to salary income and business profit is below presumptive rates, the taxpayer may get pulled into Tax Audit requirements.

Thus, a person earning salary and making a small profit from F&O transactions will now end up facing a Tax Audit merely because of one drafting change in the new law.

#IncomeTaxAct2025 #TaxAudit #44AD #CAProfession

🟥 [IMPORTANT] SC dispose of SLP Challenging Constitutional Validity of Section 16(2)(c) of the GST Act

The Hon’ble Supreme Court in M/s Prime Metals v. Central Board of Indirect Taxes and Customs & Ors. [Special Leave Petition (C) No. 18577 of 2026 dated May 29, 2026] on the peculiar facts of the case, declined to interfere with the impugned judgment/order of the Hon’ble Rajasthan High Court relegating the petitioner to the statutory appellate remedy, while leaving open all remedies available to the petitioner to be exercised, and permitted the petitioner to file the appeal with the necessary pre-deposits within a period of eight weeks before the appropriate fora/authority, with the further direction that if the appeal is so filed within the said period, it shall not be dismissed on the ground of limitation. The Hon’ble Apex Court further left open the issues raised in the writ petition relating to the validity of the provisions under Section 16(2) of the Central Goods and Services Tax Act, 2017 (“the CGST Act”), to be agitated before the appropriate fora/authority.

Read Detailed GST Newsletter at: https://t.co/1R1f065XIR

Supreme Court Takes Up Constitutional Validity of Section 16(2)(c) in Bona Fide Recipient ITC Dispute

Read Detailed Newsletter at: https://t.co/1dyXpDh2qg

EWaybill - "Bill to - Ship to" Critical update:

- Now "Ship to GSTIN" is Required in EWB

- MAKE SURE that such address of "SHIP TO" is added as Principal place or Additional place in "SHIP TO" GSTIN REG-01

- Set back for those intermediary who wants to hide the ultimate buyer details (so now main supplier while preparing ewaybill knows exactly to whom the goods is ultimately going)

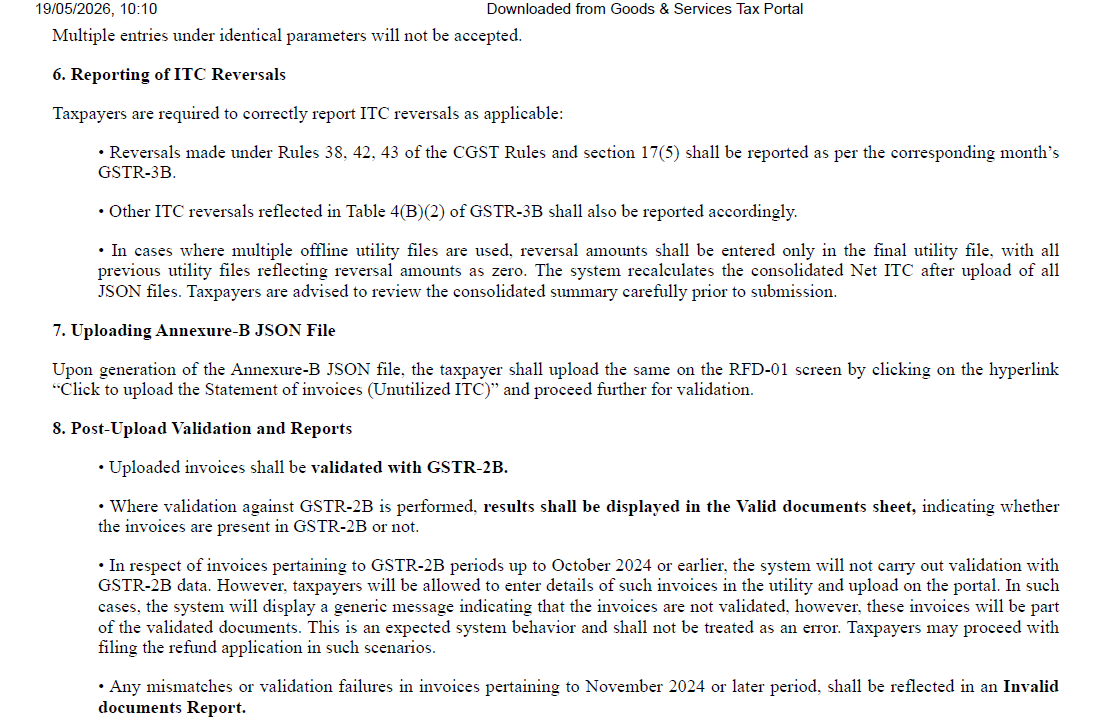

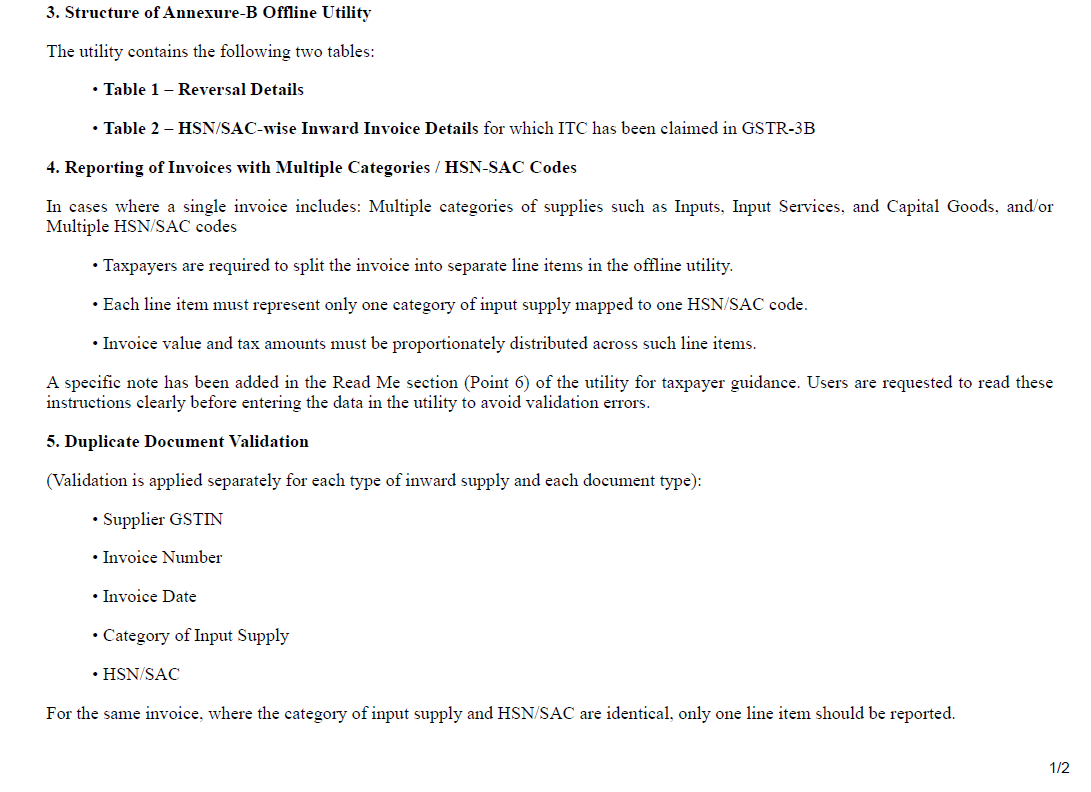

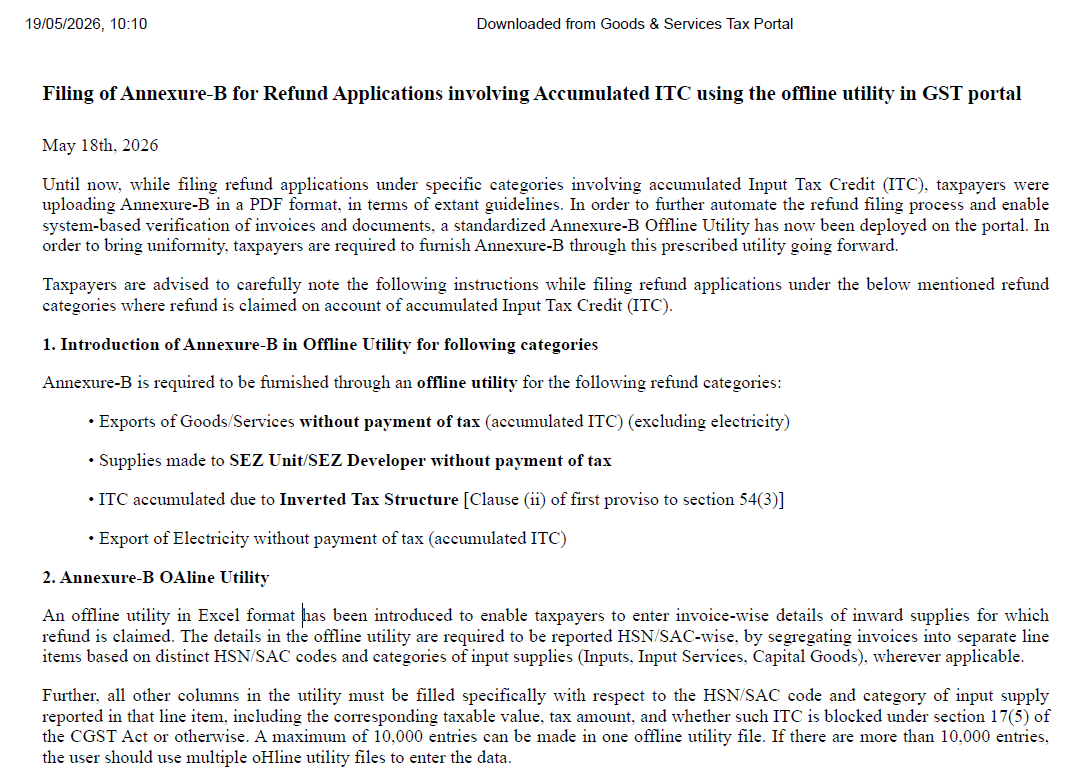

REFUND ANNEXURE B - Tips and Tricks - Part 1

Error: COPY PASTE DISABLED?

Once disabled, Don't use CTRL+C.

• Right click the cells → Copy

• In Annexure B Utility → Paste Special → Values (See clip)

Thank me later 😀

Will post more tricks & tips on @DEEPKORADIA & Wht'App Community (link in bio).

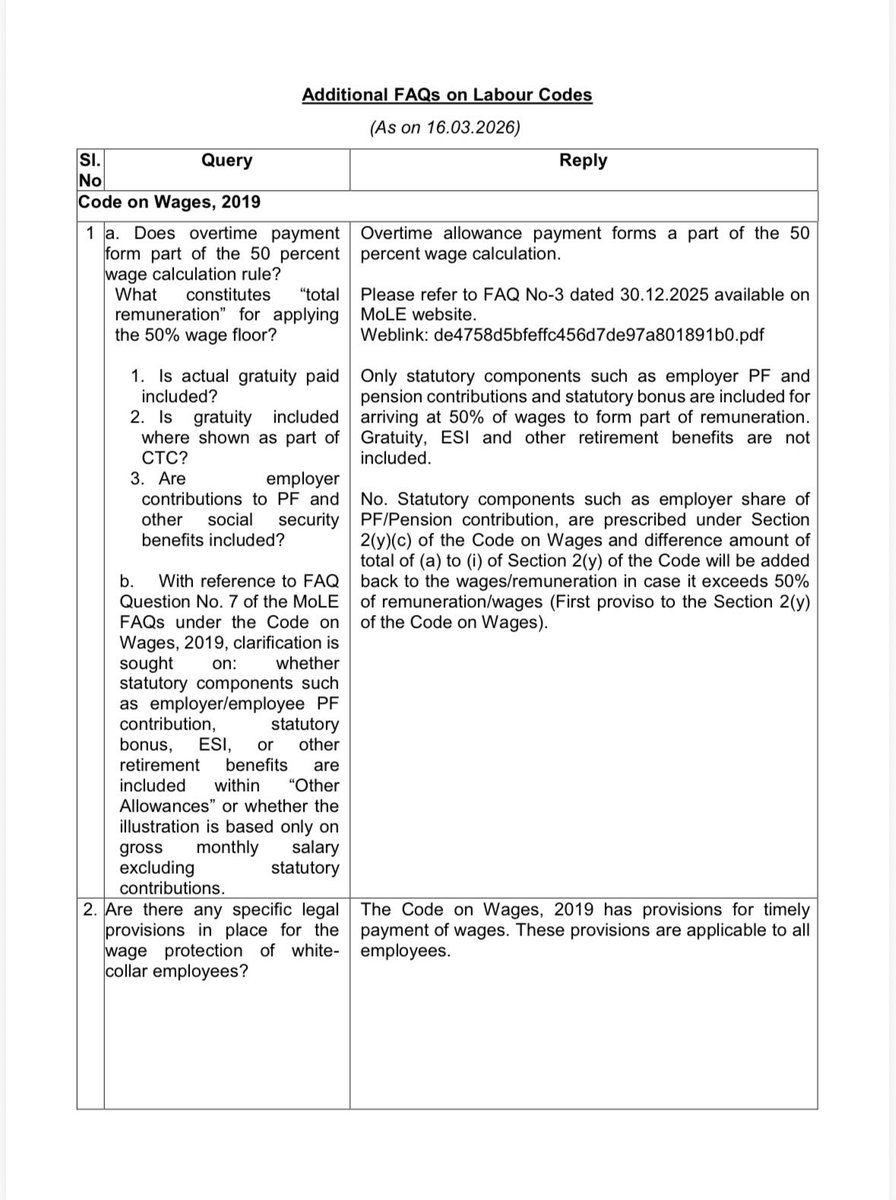

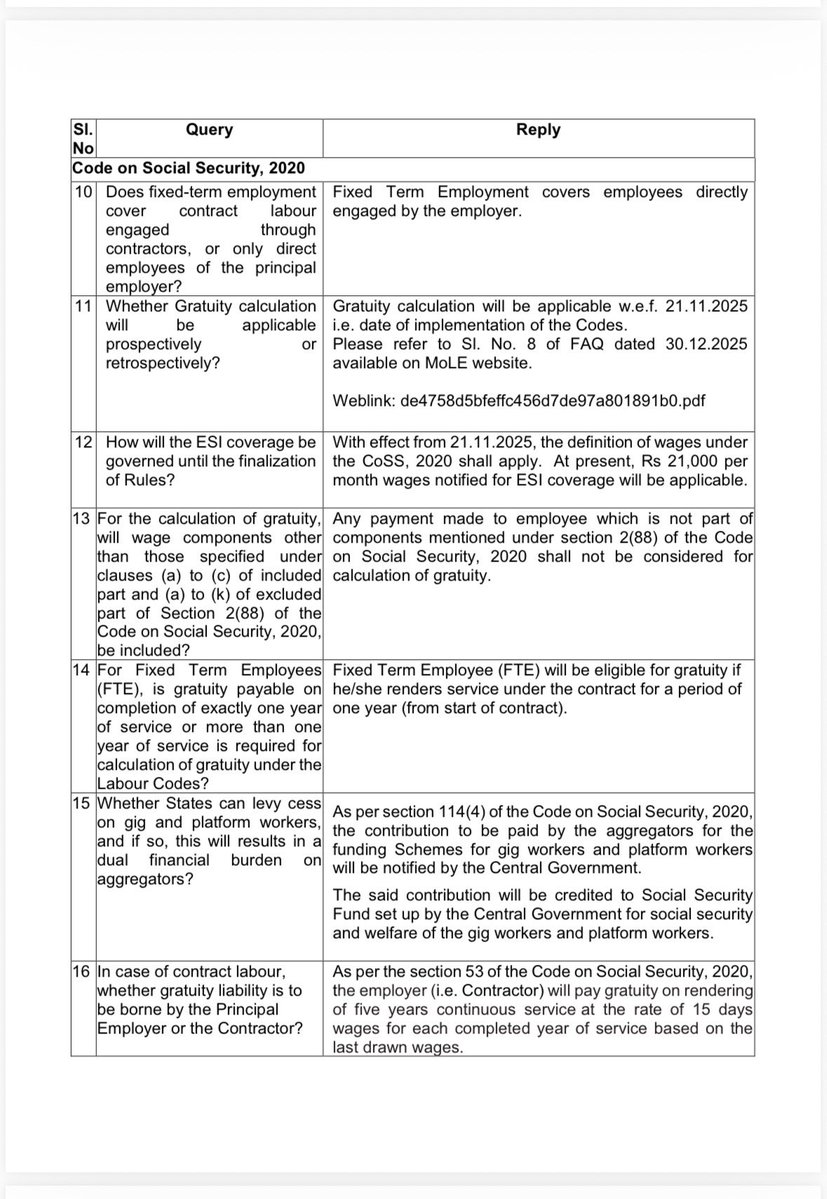

New Clarifications on Labour Codes (As of March 2026)

The Ministry of Labour and Employment (MoLE) has released critical FAQs clarifying how the new Labour Codes, implemented on November 21, 2025, will impact wages, gratuity, and leave policies.

The New Definition of "Wages" & The 50% Rule

One of the most significant changes is the "50% wage floor" rule. To ensure a higher social security base, the law now dictates how "total remuneration" is split:

• Included for the 50% Floor: Only statutory components like Employer PF, pension contributions, and statutory bonuses are included to arrive at the 50% wage threshold.

• Excluded Components: Gratuity, ESI, and other retirement benefits are strictly excluded from this calculation.

• Overtime Impact: Overtime allowance is considered part of the components under Section 2(a) to 2(i). If these allowances exceed 50% of total remuneration, the excess amount must be added back to the "wages" for calculation purposes.

Gratuity: What You Need to Know

The rules for Gratuity have been refined to provide better protection for employees, especially those on fixed contracts:

• Effective Date: The revised gratuity calculations based on the new "wage" definition apply to all service from November 21, 2025 onwards.

• Fixed-Term Employees (FTE): FTEs are now eligible for gratuity if they render just one year of service from the start of their contract.

• Historical Service: For employees retiring or resigning after the enforcement date, gratuity will be calculated based on their last drawn wages as per the new Code's provisions.

🕒 Overtime & Leave Policies

• Universal Overtime: Overtime is not just for "workers." Any employee, including supervisory or managerial staff whose minimum wage rate is fixed under the Code, is entitled to overtime pay.

• Rate of Pay: Overtime must be paid at twice the normal rate of wages if work exceeds 8 hours a day or 48 hours a week.

• Leave Encashment: Workers can carry forward up to 30 days of leave. If leave exceeding 30 days is applied for but denied by the employer, it can be encashed at the end of the year.

Welfare & Social Security

• Crèche Facilities: These must now be provided to employees irrespective of gender.

• Gig & Platform Workers: Contributions for social security funds for these workers will be notified by the Central Government, and aggregators will be responsible for these payments.

Disclaimer: These FAQs are for informational purposes. In case of any variance, the official Labour Code documents prevail.

Now you can directly buy organic produce from farmers in Telangana

Govt to launch “TG Organics” app on May 4… direct link between farmers & buyers, crackdown on fake organic products

• Minister Tummala Nageswara Rao to launch in Tandur

• Buyers can connect directly with certified organic farmers

• 500+ farmers, 100+ products already on app

• Location-based search within 50 km radius

• Only govt-certified farmers listed

10,000+ organic farmers, ~50,000 acres under certification in Telangana

Hon. Gujarat High Court upholds constitutional validity of section 16(2)(c) of the GST Act! 🫡

It was argued that placing bona fide purchasers on the same footing as those who have colluded with defaulting suppliers amounts to treating unequals as equals, thereby offending Article 14 of the Constitution, however same has now been upheld as constitutionally valid! 🔥