How could you possibly be bearish on compute right now? (Save this).

Every 10 seconds in 2026, the world generates 31.7 billion tokens and by 2030, that number hits 1.27 trillion, every 10 seconds.

That's a 40x increase and that's before the full agent economy comes online.

The Qualcomm CEO said total token demand by 2030 is in the quintillions.

Here's what most people miss because when you use ChatGPT, you generate tokens one conversation at a time but agents don't sleep. ]

They run 24/7, spawning sub-agents, carrying context, updating memory, catching mistakes and every single one of those actions burns tokens.

The shift from human paced to agent paced activity is the single biggest structural change in compute demand we've ever seen.

You don't need a perfect forecast but rather just need to believe agents become persistent and if they do, compute demand goes vertical.

The infrastructure has to be built before the demand fully arrives, which means the window to own the picks and shovels is right now.

That's where neoclouds like Nebius come in.

Nebius isn't trying to be AWS, it is a pure-play AI cloud, GPU clusters, inference infrastructure, and developer tooling built from scratch for AI workloads.

Q1 2026 revenue hit $399M, up 684% year over year and they're guiding for $7–$9 billion annualized run rate by end of 2026.

Analysts are modeling roughly 2,000% total revenue growth from end of 2025 to end of 2027.

They already have contracts with Microsoft and Meta already signed. Capex guidance raised to $20–$25 billion because customer commitments justified it.

They are sold out of capacity because the constraint isn't customers, it's how fast they can build.

Adjusted EBITDA margin on the core AI business hit 45% in Q1 and Jensen Huang called Nebius a close partner at GTC 2026.

And in a world where GPU access is the single biggest competitive moat, that relationship matters more than most people realize.

The bear case on compute requires you to believe the agent economy stalls and that's a very lonely bet to make right now.

Bullish on Nebius and Milk Pro subscribers are already up massively on this trade, come join us using the link below to get our full AI trades and we have a HUGE 33% off right now!

@MelvinInvests Or the moat is non existent and there is no barrier to new entrants and new supply. Compute will become a utility business selling commodity tokens

SEMIANALYSIS: Anthropic To Reach $1B in Operating Profit in Q3

This is extremely bullish for the AI supercycle if true

Would be the first solid confirmation that investing in AI compute can, in fact, be profitable

I published a note today that I've been thinking about for months.. About how the US stock market has arguably become too big and too imp to fail.. It's basically America's retirement fund now and poss even the savior of social security which is expected to run out of money in less than 10yrs

-Curr 55% of ppl own stocks, by far most in world. And w/ Trump Accounts bringing in 28 million add'l americans into stock ownership the vast majority of ppl (incl Top 1% (who own HALF of stock mkt), middle class and lower income) will have financial interest in the health of stock mkt and they're all voters = the political pressure to keep stocks out of a prolonged bear market is going to be very powerful.

-As such I think there's good chance the Fed will buy equity ETFs in the next major downturn to support market and it will be common practice going fwd. China and Japan already do this. They may even target certain sectors or Capex cos with the purchases.

-This is a massive variable that I feel like is a blind spot among the experts out there and why the bears get run over time and time again altho I think investors are onto it as evidenced by the persistent flows into ETFs during pullbacks as well as a survey of 1000 ppl showing 3/4 of them are confident the Fed will bail out markets in next crisis.

-This is just one byproduct of the 'Nothing Stops This Train' monetary supply explosion and debt extravaganza sweeping the world but esp in US which at this point feels irreversable.. Thoughts? lol

Morgan Stanley has warned that AI investors are likely to begin rotating out of semi stocks and into AI hyperscalers.

The firm picked Amazon $AMZN, Microsoft $MSFT, and Meta $META as the most attractive within the current AI ecosystem.

Is the AI infrastructure trade running out of steam?

JPMorgan: Data Center Watch report says not even close.

Worth bookmarking if you're tracking the AI capex debate.

Token usage, GPU leasing rates, and DRAM prices continue to rise. JPM noted in its latest 'Data Center Watch' report that large model usage continues to expand rapidly, token spending has reaccelerated, GPU leasing prices in the non-hyperscale cloud market are still rising, and DRAM spot prices remain strong.

> LLM token : June volume +70% MoM (vs May's 33%, April's 5%). YoY growth hit 20x, above May's 12x and April's 15x. Token spending also rebounded, +70% MoM and 16x YoY, snapping the prior two months' slowdown.

> Unit economics: Token usage and revenue are diverging. Falling model prices haven't dented market revenue - price erosion is slowing while usage growth outruns the cuts. This is the number that decides if AI commercialization actually works.

> Country wars: US models (OpenAI, Anthropic, Google, xAI) fell to 35% of OpenRouter token share, down from 46% in May and 56% in April - even as their volume grew 30% MoM and 8x YoY. Chinese/low-cost models (DeepSeek, MiniMax, MiMo, GLM) are eating share in cost-sensitive use cases: dev workflows, startups, agent coding.

> Rental prices: A100 at $1.63/GPU-hour (+6.3% MoM, 5th straight monthly rise). H100 at $2.72 (+3.7% MoM, 7th straight month up). B200 at $5.33 (+2.7% MoM).

> Memory: AI server DRAM demand is pulling supply from conventional DRAM. Three straight months of modest price declines suggest NAND tightness is easing - but prices are still up 5x+ YoY, so the industry hasn't hit supply abundance yet.

Which number surprises you more: token growth reaccelerating to 20x YoY, or GPU rental rates still climbing after 5-7 straight monthly increases?

Repost this if you're tired of the "AI capex is slowing" take this report has the actual numbers on it.

Here's my full interview with CNBC, covering my bear case against generative AI, OpenAI's questionable finances, AI's lack of ROI, and how all of this is a symptom of the tech industry running out of hypergrowth ideas.

It's great to see the mainstream media discussing this.

This is the kind of insider activity that should get your attention.

A $1.5B telecom company just saw nearly $30M of insider buying in one week...

Liberty Latin America $LILA, a telecom and broadband provider servicing Latin America and the Caribbean, just saw roughly 2% of its ENTIRE market cap eaten up by insiders in the past week.

Meanwhile, price is near all-time lows with a massive multi-year divergence forming.

When insiders put that kind of money to work you have to ask yourself: what do they know that the rest of the market doesn't? $LILA

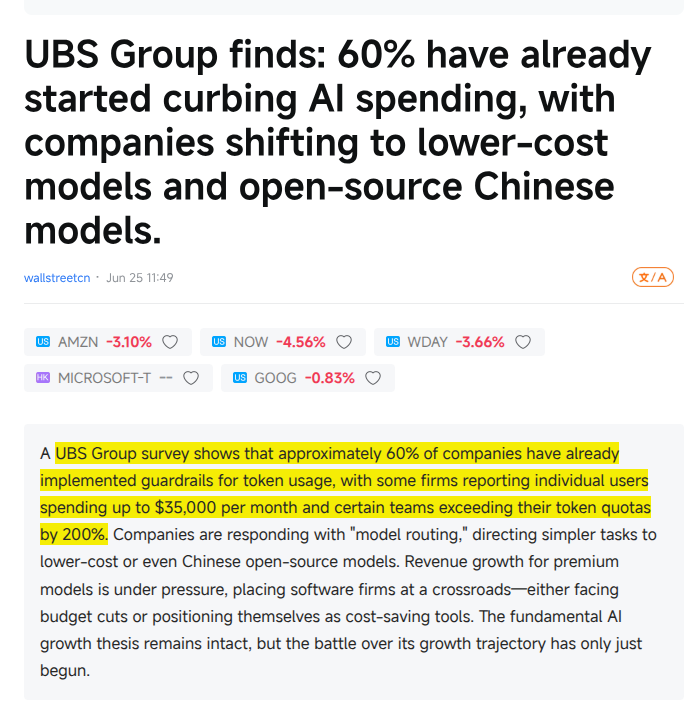

UBS says 60% of companies now watching AI budgets are moving to cheaper models and open-source Chinese models

The pressure is coming from extreme bills, including users spending up to $35K/month, teams exceeding quotas by 200%, and companies cutting internal AI tools from 5 to 2.

Companies are not abandoning AI, they are using model routing, which sends easy tasks to cheaper models and saves premium models for hard reasoning, code, and long-context work.

Chinese open-source models such as Qwen, DeepSeek, MiniMax, GLM, and Kimi now fit the enterprise cost curve because they can be run locally or used through cloud catalogs.

---

news .futunn.com/en/post/75068082/ubs-group-finds-60-have-already-started-curbing-ai-spending?level=2&data_ticket=1780870170397383

MICRON SEES AI-DRIVEN MEMORY SHORTAGE EXTENDING BEYOND 2027

• MICRON EXPECTS TIGHT MEMORY MARKET CONDITIONS TO PERSIST BEYOND CALENDAR 2027 DUE TO SURGING AI-DRIVEN DEMAND ACROSS ALL SEGMENTS

• COMPANY SAYS IT CURRENTLY HAS NO CLEAR VISIBILITY ON WHEN MEMORY SUPPLY WILL CATCH UP WITH GROWING DEMAND

• MICRON PROJECTS OPERATING EXPENSES TO INCREASE BY APPROXIMATELY $1 BILLION IN FISCAL 2027

• FISCAL Q4 CAPITAL EXPENDITURE EXPECTED TO REACH AROUND $10 BILLION

• FULL-YEAR FISCAL 2026 CAPITAL SPENDING FORECAST AT APPROXIMATELY $27 BILLION

• QUARTERLY CAPEX IN FISCAL 2027 EXPECTED TO EXCEED FISCAL Q4 2026 LEVELS

• COMPANY CONTINUES TO AGGRESSIVELY INVEST IN CAPACITY TO MEET AI-RELATED MEMORY DEMAND

• MICRON NOTES THAT POTENTIAL IMPACTS FROM TRADE POLICIES OR GEOPOLITICAL DEVELOPMENTS ARE NOT INCLUDED IN ITS GUIDANCE

• UNDER STRATEGIC CUSTOMER AGREEMENTS, MICRON EXPECTS TO RECEIVE APPROXIMATELY $22 BILLION IN CASH DEPOSITS AND RELATED FINANCIAL COMMITMENTS

• COMPANY PLANS TO INCREASE CAPITAL RETURNS TO SHAREHOLDERS

• MICRON STATES IT EXPECTS TO RETURN 100% OF EXCESS CASH TO SHAREHOLDERS OVER TIME

• COMMENTS REINFORCE THE VIEW THAT AI INFRASTRUCTURE DEMAND CONTINUES TO OUTSTRIP MEMORY SUPPLY, SUPPORTING A FAVORABLE PRICING ENVIRONMENT FOR DRAM AND HBM PRODUCERS

The latest BofA survey is essentially a signed death certificate for the semiconductor trade.

80% of global fund managers are now consensus long.

Let that absolute absurdity sink in for a second.

That is the highest crowding metric since the peak of the zero-interest rate tech bubble in October 2020.

The AI reply-guys genuinely believe this is a permanent structural paradigm shift.

In reality, it is nothing but a historic concentration of passive flows waiting for a singular LIQUIDITY shock.

When every single participant is crammed into the exact same side of the boat, there is absolutely zero marginal buying power left.

Primes are already quietly adjusting their margin haircuts on $SMH behind closed doors.

The fact that Mag 7 crowding collapsed to 12% tells you exactly how violently capital has been herded into this one hyper-specific sub-sector.

Institutions are weaponizing your euphoria to systematically distribute their bags at the absolute top of the cycle.

You are not front-running the future of global compute.

You are providing premium exit liquidity for the most obvious cyclical top in a decade.

@oguzerkan Nothing is ever obvious especially when making forecasts. Who knows about your assumption that 8.5% is the correct cap rate and who knows how much the net income figure could erode if Agentic AI cannibalises software apps.

@RazOlsRF Hahahaha quite a stretch to argue that 22 vs 29 is an age advantage for Novak

Novak at 37/38 beating Sincaraz in their early 20's is material.

Making age related excuses for Federer at 29-33 is not!

And the final tell. The money arrived all at once.

Semiconductor ETFs just took in the largest weekly inflow on record. A spike that dwarfs everything in the chart's history, including 2021 and 2022.

This is what tops are made of. Not weakness, euphoria. Record price, record volume, record buying, all in the same week.

O'Neil had a name for it: a climax top. The CAN SLIM playbook teaches that after a long advance, a stock or sector goes near-vertical on its heaviest volume ever, the biggest weekly gains of the entire run. That's not accumulation. That's the last buyer rushing in.

22% of the index. A 5-sigma momentum overshoot. A parabolic third leg. Record inflows.

History doesn't repeat. But it has shown us this exact picture before, and it rarely ends with another leg up.

When everyone is finally certain, there's no one left to buy.

@davidzmorris Yes because Apollo is a chop shop and not a blue chip top tier asset manager with risk committees, investment boards and a sterling reputation!!