The robotics build out may become one of the biggest industrial infrastructure expansions of the next decade.

Not just robot OEMs.

The real opportunity may sit inside the enabling technologies powering “physical AI.”

$OUST — Ouster is far more than a traditional LiDAR company. Their digital LiDAR architecture combines high-resolution 3D sensing with rich perception data, allowing robots and autonomous systems to better interpret environments in real time. The company’s software-defined approach improves scalability, reliability and cost structure versus legacy mechanical systems. As robotics evolves from simple automation toward contextual machine perception, Ouster’s stack could become increasingly valuable across industrial automation, warehouses, smart infrastructure, security and autonomous robotics. The bullish thesis isn’t just “robot eyes” — it’s machine perception infrastructure.

$AEVA — Aeva’s technology stack is one of the most technically differentiated in the sector. Unlike conventional time-of-flight LiDAR, Aeva uses FMCW (frequency modulated continuous wave) sensing, allowing simultaneous measurement of depth, velocity and object movement at long range. That capability becomes increasingly important in dynamic real-world environments where robots need to predict motion, track objects and navigate safely around humans. If next-generation robotics requires higher-order spatial awareness and real-time environmental understanding, Aeva could become one of the more advanced perception platforms in physical AI. Higher risk, but potentially massive upside if adoption inflects.

Harmonic Drive Systems (6324.T) — One of the most important humanoid robotics suppliers globally. Precision actuators, reduction gears and motion control systems are critical for humanoid balance, dexterity and efficiency. Many analysts believe actuator systems could represent one of the largest cost layers inside humanoid robots. This is one of the purest “picks and shovels” plays in the robotics ecosystem and a company many retail investors still overlook entirely.

$ATI — ATI produces specialty titanium and advanced alloys used across aerospace, defense and industrial systems. Humanoid robotics introduces a major need for lightweight strength, fatigue resistance and high-performance structural materials. The market still largely views ATI through an aerospace lens, but the company may quietly benefit from the broader robotics and automation build out over time. One of the more underappreciated second-derivative plays in the theme.

$GLW — Corning is quietly positioned across several future infrastructure layers: glass substrates, optical connectivity, advanced materials and photonics. As robotics and edge AI scale, demand for higher bandwidth, lower latency and more advanced semiconductor packaging may rise significantly. Corning’s exposure to next-generation glass technologies and optical systems could make it an overlooked beneficiary of the physical AI cycle.

Machine perception

Precision motion

Advanced materials

Semiconductor packaging

Power and connectivity infrastructure

The supply chain behind physical AI may ultimately become the bigger investment story.

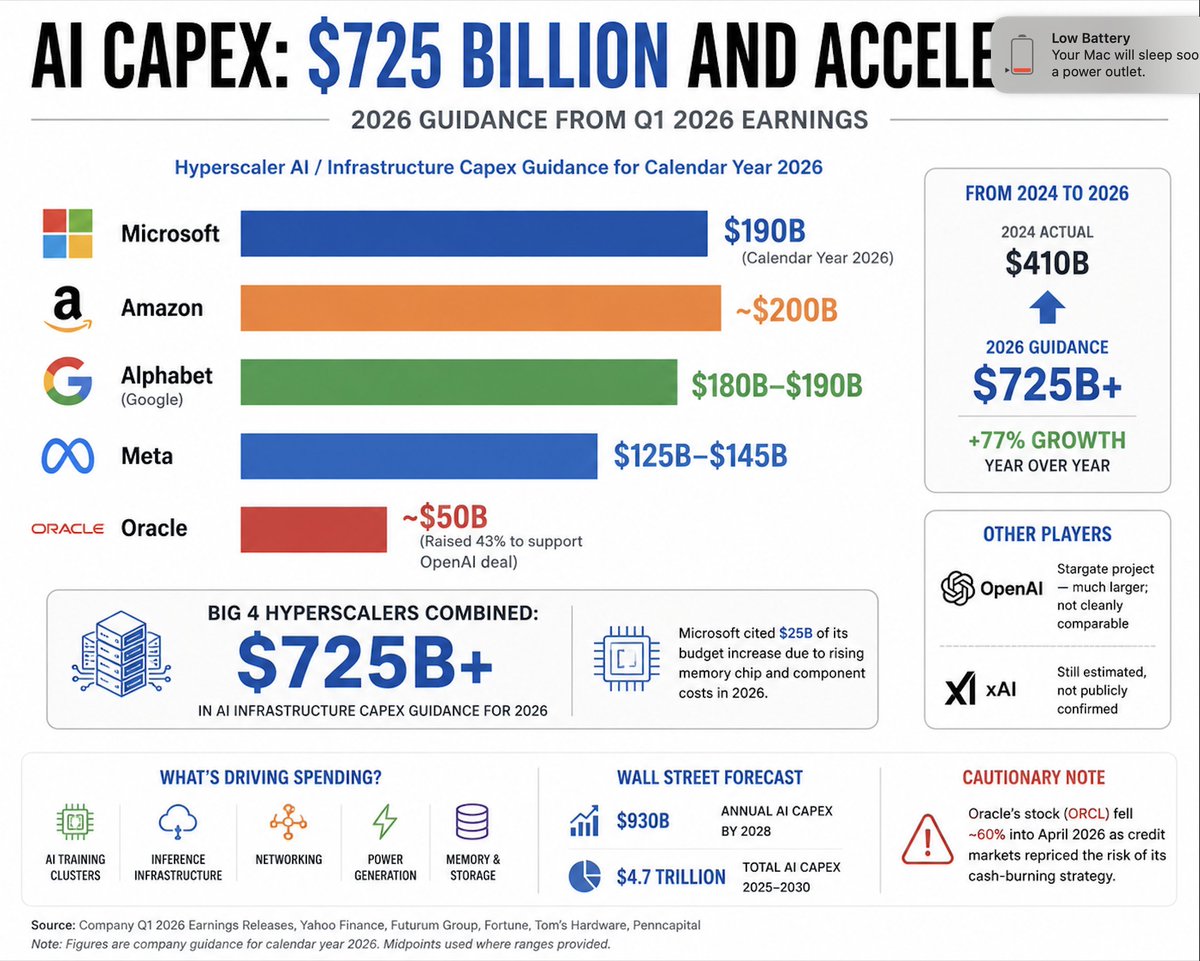

The AI buildout isn't slowing down.

The big hyperscalers are now guiding for roughly $725B+ in AI infrastructure spending in 2026, up from about $410B in 2024.

That's a 77% increase in just two years.

What's interesting is that this isn't based on hype or analyst projections. These figures come from company guidance and Q1 earnings commentary.

$MSFT $AMZN , $GOOGL, and $META continue to increase spending as demand for AI compute, networking, power, storage, and memory keeps growing.

In fact, Microsoft said roughly $25B of its increase is tied to higher memory chip and component costs alone.

The question for investors is where this spending ultimately flows across the supply chain.

Every dollar of AI capex becomes revenue for someone.

Chips.Memory.Networking.Servers.Cooling.Power.

Follow the capex.

I stopped out of a few over extended stocks. That is part of investing.

The late '90s weren't a straight line to the dot-com peak. Between 1997 and 1999, investors endured multiple violent corrections driven by global macro shocks:

📉 October 1997: The Asian Financial Crisis sparks a mini-crash. The Dow falls 7.2% in a single session, triggering trading halts.

📉 August 1998: Russia defaults on its debt. The collapse of Long-Term Capital Management sends shockwaves through markets. The S&P 500 drops 19% while small caps fall more than 25%.

📉 1999: Even during one of the greatest bull markets ever, sharp rotations and pullbacks repeatedly shook investors out of winning positions. Yet despite all of this, the Nasdaq finished 1999 up more than 85%.

The lesson: Legendary bull markets don't eliminate volatility. They often contain some big corrections.

There will be many more opportunities ahead.

CA

If the sector rotation continues, we could see capital flow back into nuclear and power-related names.

$SMR, $LEU, $CCJ, $NEE, and $OKLO have all seen significant pullbacks.

But has the underlying thesis changed?

AI still needs power.

Data centers are still being built.

Grid demand continues to grow.

The stocks corrected.

The narrative didn't.

I went long $OKLO and $SMR.

Both charts are tightening up and could be setting up for a move higher if buyers return to the group.

NFA

$CRDO blowout.

Q4 FY26 — beat & raise across the board.

Revenue: $437M

✅ (+155% YoY)

Adj EPS: $1.16 vs $1.03 est

✅ Adj NI: $226.7M vs $202.7M

✅ Gross Margin: 68.2% — holding the line

Q1 guide: $465-475M (above Street)

AI connectivity is real.

Stock is down -13%

$MU The AI memory trade has been one of the biggest winners of this cycle.

I'm up 115% on $MU since my first buy.

Congrats to the Micron holders what an incredible run.

If the sector rotation continues, we could see capital flow back into nuclear and power-related names.

$SMR, $LEU, $CCJ, $NEE, and $OKLO have all seen significant pullbacks.

But has the underlying thesis changed?

AI still needs power.

Data centers are still being built.

Grid demand continues to grow.

The stocks corrected.

The narrative didn't.

I went long $OKLO and $SMR.

Both charts are tightening up and could be setting up for a move higher if buyers return to the group.

NFA

@SRxTrades Aggressive capital raises and the all stock Omnisys acquisition have kept the share price down. Its looking tight now and ready to go.

Also has a short float of 33%.

$MRVL earnings.

The Numbers: Record Q1 revenue of $2.42B (up 28% YoY) and adj. EPS of $0.80, both topping Wall Street estimates.

The Real Driver: Data center revenue skyrocketed to $1.83B, now accounting for a massive 76% of their total business.

They significantly raised revenue outlooks for both FY2027 and FY2028 based on "exceptional" AI bookings, forecasting 35% YoY growth next quarter ($2.7B midpoint vs. $2.6B consensus).

LONG MRVL.