@The_RockTrading $MSFT is a significant holding in my portfolio. Top line is only growing 15% on average. EPS is growing 20-30% which is extraordinary. Revenue by segment is very interesting too. Productivity and business processes segment grows at 30-50% Q/Q beating cloud growth easily.

@qualtrim I love $AVGO as a growth company. I sold it but think it is still cheap. Top line is growing at 20-30%. EPS accelerated to 100-200% growth quarter over quarter from $1.27 to $5.28. In FY 2026 top line grows 65% and EPS grows by 70%. FCF doubles from $25bn to $50bn in FY 2026.

@MrMikeInvesting $NOW is my favorite from the list beside $PLTR. Top line is growing over 20% quarter over quarter. EPS is growing at 20-30%. Balance sheet is strong with $3bn in cash after debt. PEG ratio of 1 is also very attractive fundamentally.

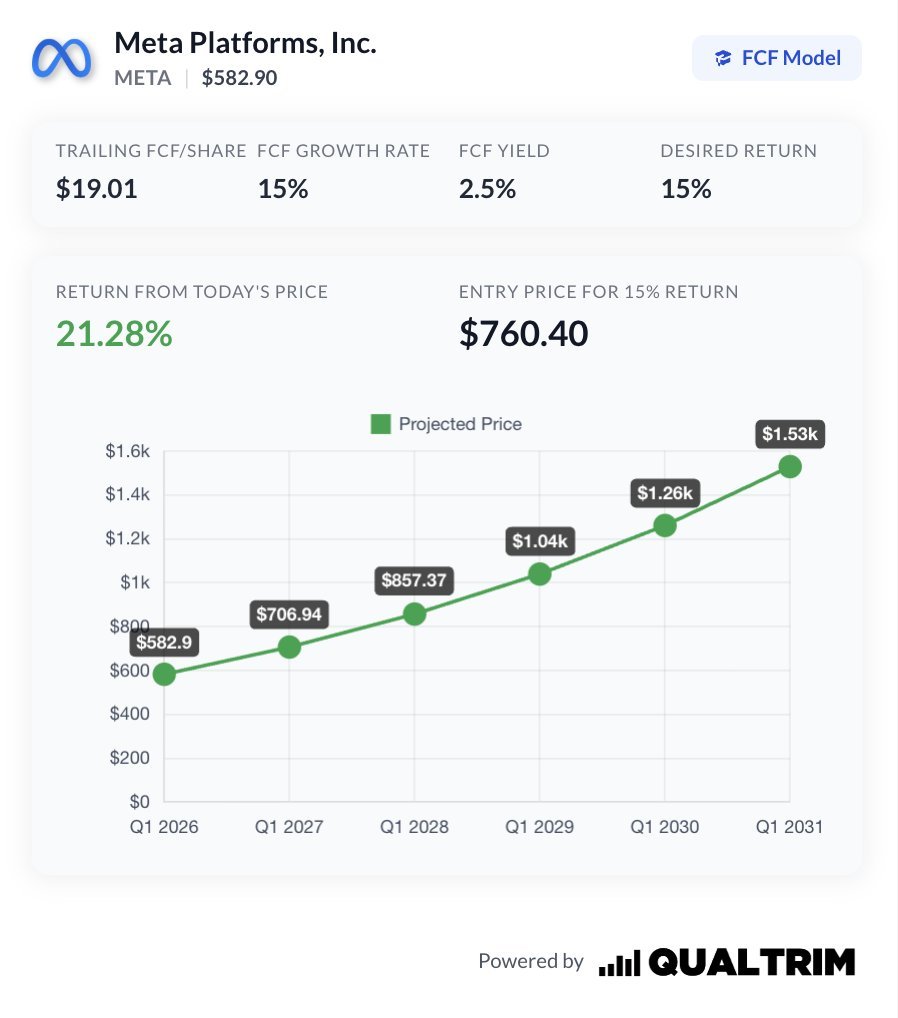

@growthrapidly $PLTR and $META are looking juicy. $PLTR is my top pick as of now. Revenue will eventually grow to over $60bn in the next years. Quick and current ratio sitting at 7x which means they have huge cash reserves and can easily pay short and long term debt.

@Mr_Derivatives $MSFT trading at a forward 20x earnings is cheap. Top line is growing at 15-18%. EPS grows at 30% in the recent quarters. I also like the operating cash flow which is growing at 20-30%. It is a better indicator than FCF because of huge capex spending.

@BemisLisa83887 For me $META is the best out of the list. Great top line growth of 26% in FY 2026. I also like the payment segment growing at 60% quarter over quarter. Daily active users now at 3.56bn. Only cash burning segment is reality labs but has a potential to bring in high amounts of FCF.

@patrimcriterio I hold $META in my portfolio. The company is growing revenue by over 20% quarter over quarter. Operating cash flow growing at 20-30%. Because capex is sky high I look at operating cash flow because the company can easily cut the capex and produce huge amounts of FCF.

@YodaStockInvest I would buy $PLTR. The stock is valued very fair and fundamentals are very strong. Just look at the balance sheet and revenue growth. I know a forward 80x earnings is not cheap but even Alex Karp is forecasting FCF approximately $15bn in the next 3 years.

@VJNCapital $PLTR is an abnormal beast. Revenue growing at 30-60% every quarter gross margin at 85% and profit margin at 44%. Also they hold $8bn in cash after debt and growing FCF at 80-100%. Next stop this year $200!

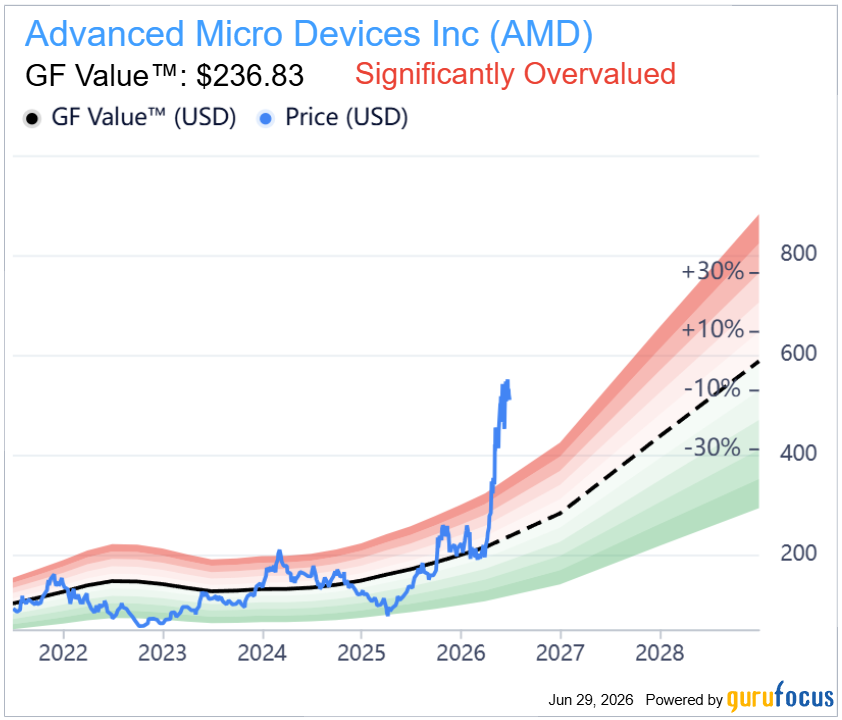

@Speculator_io I like your list very much. As you can see $AMD is wildly overvalued but fundamentally seen (EPS, revenue and FCF) the stock will grow faster than price.

@ModernDayInves At this price level $MSFT is still a buy. I bought 2 weeks ago or so. Revenue is growing double digits and P/S is lagging compared to revenue over time.