Who will be the "Nvidia of Quantum Computing?"

We are currently finalizing our 2026 Quantum Computing Tech Forecast, built on 20+ years of MIT research. Most investments are based on intuition—we’re using patented AI to replace hype with systematic foresight.

Our analysis identifies the winners of the qubit race and the "hidden" supply chain enablers before the market catches up. 📊

Secure your early access to the report:

https://t.co/BVT0Qkoo9P

Technology is leverage and tends to destabilize status quo. Every tool beyond the hands has allowed us to kill at ever-larger scales.

Anxiety is a reasonable reaction and raising the alarm can be quite useful too as it helps us put new safeguards into place.

In general, humanity has shown a remarkable ability to manage and assimilate new innovation. tech anxiety is a vital part of this process. My favorite example is the founding of UL for safety testing at a time when the spread of electricity was literally setting cities on fire.

https://t.co/A5BuV2iLDF

55 years separate NASA's Apollo A7L spacesuit from its Artemis replacement, the Orion Crew Survival System (OCSS). In that time we invented the internet, sequenced the human genome, and put a supercomputer in everyone's pocket. So surely the spacesuit saw some transformative breakthrough?

Not really.

The Apollo missions used one basic suit forced to play two roles. NASA essentially took a moonwalking suit and ripped parts off it until it fit in a pilot's seat.

Artemis doesn't subtract. It separates: OCSS for the spacecraft and AxEMU for spacewalks.

The OCSS is an evolution of the Shuttle-era "pumpkin suit," built for launch, reentry, and catastrophe.

Apollo suit: no independent emergency clock — tethered to the spacecraft's life support.

OCSS: 144 hours of emergency life support on its own.

Why 144 hours? That is the exact time needed for a "free-return" slingshot from the Moon back to Earth.

The Axiom Extravehicular Mobility Unit (AxEMU) is a dedicated suit with bearing joints that actually let a human move.

Apollo suit: 7-hour missions. AxEMU: 8-hour missions + 60 minutes of emergency reserve.

Seven hours was the hard limit for moonwalks in Apollo suits because of CO₂ saturation in the portable backpack. AxEMU managed to remove the CO₂ saturation ceiling by putting a regenerative lung on the back that theoretically allows for indefinite CO₂ removal.

Even after this, there is no significant improvement in spacewalk time due to pure biological limitations such as human fatigue and constraints like battery power and cooling water.

The 55-year gap didn't produce anything magical. It forced one critical design decision: stop making one tool do two jobs.

In 2021, the DOE set a target: $60/kWh battery cells by 2030.

By 2025, average pack prices hit $108/kWh — down 93% from $1,415 in 2008. BEV packs crossed below $100. Chinese LFP cells are already trading at $56/kWh.

So what's blocking the last mile to mass affordability?

The factory floor.

New gigafactories scrap 30-40% of production during ramp-up. In China, that number is under 10%. Each percentage point of scrap costs a factory ~$10M/year. A 30% reject rate at full capacity burns ~$900,000 per day.

Dry electrode processing could cut manufacturing energy use by 46% and costs by 11%. Tesla has produced 100M+ cells with its dry-cathode lines. But scaling the process reliably at speed remains an unsolved problem — LG, Tesla, and AM Batteries are all still iterating.

Then there's silicon. Silicon anodes store 10x more lithium than graphite — but expand 300% when charged. That swelling cracks the cell from the inside out.

The battery cost curve isn't a materials problem anymore. It's a manufacturing precision problem. The chemistry works. The physics works. The engineering at scale doesn't — yet.

In 2015, a survey drone with cm-grade GPS cost $25,000, flew 20 minutes, and had zero AI.

In 2025, a $5,000 drone flies 45 minutes, avoids obstacles omnidirectionally, and can launch, inspect, and land itself in complete darkness.

The decade in numbers:

Precision GPS: $25K → $5K

Onboard AI: 0 → 100 TOPS

Flight time: 23 min → 55 min

Camera sensor: 12MP → 100MP

Aerial survey cost: ~$35/acre → ~$10/acre

One North Sea oil operator saved $4M by swapping rope teams for drones. Power line crews went from 2 miles/day to 20.

The commercial drone market grew from $2B to $30B+ not because of one breakthrough, but because five quiet improvements compounded at the same time.

That's how technology inflection points actually work.

A couple of things worth correcting here. CRISPR wasn't "discovered in 2012." It was first observed in bacteria in 1987. The yogurt bacteria connection was published in 2007. What happened in 2012 was Doudna and Charpentier showing it could be programmed as a gene-editing tool — that's engineering, not discovery. And it was not "filed away as a curiosity." It was immediately recognized as transformative.

"No cure has ever existed" for sickle cell is also wrong. Bone marrow transplants have been curing it since the 1980s — they're just risky and require a matched donor. And calling it "functionally eliminated" in 2024 is a stretch when Casgevy costs $2.2M per patient and has been administered to very few people.

The broader arc of the post is right — biotech timelines are compressing. But it didn't happen at once. CRISPR, mRNA, peptide chemistry, and gene delivery were all improving at their own steady rates for decades. What changed is they converged — each one unlocking the next. What looks like "20 years of nothing then everything" is usually five or six component technologies quietly compounding until they cross each other's thresholds. The breakthroughs weren't sudden. The visibility was.

AGI still doesn't have an agreed-upon definition. So both of them can be right.

But there's a more interesting question underneath. We keep talking about LLMs as if they're one thing. They're really a bundle of component technologies: transformer architectures, attention mechanisms, tokenization, RLHF, memory systems, inference optimization — each improving at its own rate for its own reasons.

When Hassabis says "one or two breakthroughs are still needed," he's essentially saying some components in the stack are stalling while others keep scaling. LeCun is saying the same thing, just with more pessimism about which ones matter.

So maybe the useful version of this question isn't "are LLMs a dead end" — it's which specific pieces inside the stack are still on steep improvement curves, and which have hit diminishing returns? Because historically, the biggest leaps in technology don't come from scaling one thing harder. They come from a component nobody was watching suddenly getting better.

Maybe not hidden — just not marketed. Intel published its 99.9% gate fidelity in Nature. PsiQuantum's Omega chipset got a Nature paper too. Their fab partners, facility locations, and billion-dollar government deals are all on the record. What they don't disclose is qubit counts and yield. When the only metric nobody shares is the one that actually matters, the race is probably closer than the press releases suggest.

SpaceX uses LiDAR to dock with the ISS. Tesla refuses to put it in cars.

Same company founder. Opposite decisions:

In space: zero interference. Pure geometry. A $250,000 sensor pays for itself when failure means losing a spacecraft.

On Earth: rain, fog, glare, exhaust. LiDAR chokes on exactly the conditions drivers face most. Waymo's original sensor stack cost ~$150,000 per vehicle. A single automotive camera? $15-$30.

Tesla went with 8 cameras at ~$350 total. Waymo went with a full sensor suite at $30,000+. Over 250 billion dollars have been spent industry-wide on autonomous driving R&D — and the cheapest sensor setup is the one scaling fastest.

Perfect sensors win in controlled environments.

Adaptable intelligence wins in the real world.

In 1954, a color TV cost $1,000. A new car cost $2,500. You were paying 40% of the price of a vehicle — for a screen that looked worse than your existing one.

The FCC mandated that color broadcasts work on existing black-and-white sets. So engineers stripped the color data to its bare minimum and hid it in the tiny, unused gaps of the monochrome signal. Millions of B&W viewers never knew it was there.

But even if you bought a color set, the picture was disappointing. Early red phosphors were so weak that engineers had to throttle blue and green just to keep the image from looking radioactive. You paid four times more for a dimmer screen.

The turning point came in the late 1960s — two breakthroughs at once. Rare-earth phosphors like europium finally produced a red bright enough to let all three colors run at full intensity. And solid-state transistors replaced vacuum tubes, making sets cheaper, cooler, and reliable enough to last years without a repair visit.

Color TV eventually won by respecting the installed base, proving that sometimes the most successful technology is the one that learns to coexist with the systems it aims to replace.

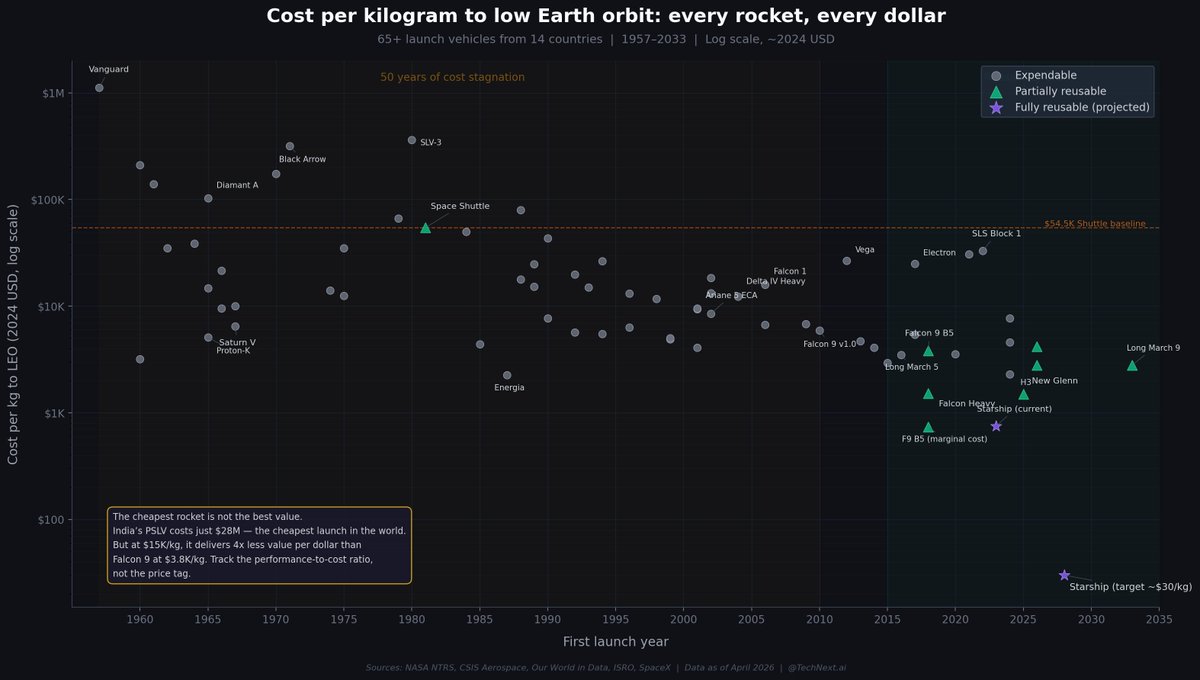

Stop looking at the price tag of a rocket. Start looking at $/kg.

India's PSLV costs ~$28M — cheapest in the world. But at $15K/kg, Falcon 9 at $67M delivers 4x more value per dollar.

Shuttle: $54K/kg

Falcon 9: $3.8K/kg

Starship target: <$100/kg

Track the ratio.

Fascinating by IBM. Using quantum hardware as a scientific instrument to decode the half-Möbius topology is a major milestone. At TechNext, we focus on this shift: where a scientific "spark" becomes a quantifiable and predictable tech domain.

While this molecule is a brilliant discovery, the strategic value lies in how these quantum-centric systems are now aligning with our quantitative growth models. We’ve recently applied our MIT-born methodology to the sector in our new Quantum Report—it’s exciting to see the physical reality catching up to the data.

Path dependence is why industries get stuck. Physics is why they eventually can't stay that way.

Silicon isn't the best semiconductor. GaAs switches faster, GaN handles more heat, and diamond is — in theory — better in nearly every way. Silicon won because its oxide happens to be a perfect insulator — a fortunate accident that seeded a $500 billion supply chain that no one can leave.

But path dependence doesn't last forever.

For decades, copper interconnects were known to be 40% more conductive than aluminum. The industry stayed on aluminum anyway — until shrinking transistors made resistance-capacitance delay the hard bottleneck. Physics forced the switch in 1997. Companies that bet on aluminum late did not recover.

The same pattern is playing out in quantum computing right now. Superconducting qubits lead on qubit count because they borrowed silicon's manufacturing infrastructure. But their coherence ceiling is measurable and close. Trapped-ion systems — currently dwarfed on raw scale — hold coherence times up to two million times longer. Quantinuum's latest results on its 98-qubit Helios processor have collapsed the physical-to-logical qubit ratio to near parity.

The crossover point isn't guaranteed to be soon. But it is no longer theoretical.

This is exactly the kind of inflection that gets missed when investment decisions are driven by what's loudest rather than what's improving fastest. At @TechnextInc, we quantify these improvement rates across thousands of technologies, so organizations can see these shifts before they become obvious.

The aluminum moment always looks obvious in hindsight.

The Great Orbit Gap (2011–2020) ended when SpaceX outpaced institutional inertia. By integrating high-growth tech like 3D-printed superalloys, Friction Stir Welding, and autonomous LIDAR, SpaceX's reusable Crew Dragon disrupted the aging Soyuz's dominance through superior innovation trajectories.

AGI lacks a clear definition despite its massive economic and policy impact. While some define it as surpassing human labor economically, others require total task mastery. This ambiguity, plus the gap between mimicking and understanding, makes timelines highly speculative and prone to hype.

CNTs promised superpowers (stronger than steel, lighter than Al, more conductive than Cu) but spent years stuck between lab promise and real-world adoption. Now they're key battery additives enabling next-gen EV electrodes. Scaled from mg to thousands of tons, CNTs have gone from curiosity to workhorse.