BREAKING: SK Hynix stock, South Korea’s second most valuable company, officially debuts on the Nasdaq and surges +14% at the open, now worth over $1 trillion.

The company’s ADRs were priced at $149/share, raising $26.5 billion.

A few takeaways from Dylan Patel’s latest podcast:

Anthropic turned free-cash-flow positive in the second quarter of this year and has entered profitability.

Both April and May were profitable and cash-flow positive. At the time of recording, June had not yet been closed, but the trend was continuing in the same direction.

Anthropic’s annualized recurring revenue, or ARR, has now surpassed $50 billion, with gross margins exceeding 70%.

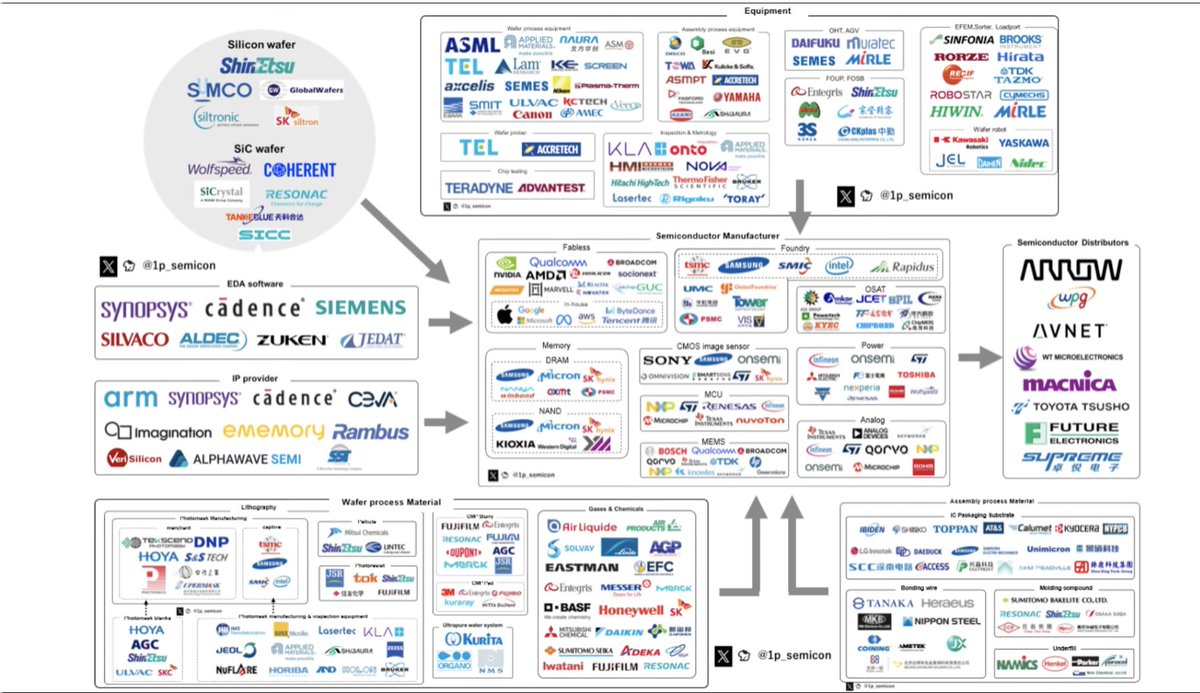

Goldman Sachs had released a supply/demand heatmap and price trends for major sub-segments/products. To provide an overview, here are some key names at each layer:

DRAM

SK Hynix $000660.KS

Micron $MU

CXMT

Nanya Technology $2408.TW

Samsung Electronics $005930.KS

NAND

SK Hynix $000660.KS

Micron $MU

Samsung Electronics $005930.KS

Sandisk $SNDK

Kioxia $285A.T

Western Digital $WDC

YMTC

Nearline HDD

Seagate $STX

Toshiba

Western Digital $WDC

Foundry - TSMC & Local China

SMIC $0981.HK

Hua Hong Grace Semiconductor $1347.HK

Taiwan Semiconductor Manufacturing $TSM

Analog Semis - Global & Local China

Infineon Technologies $IFX.DE

Texas Instruments $TXN

ON Semiconductor $ON

STMicroelectronics $STM

OmniVision Integrated Circuits $603501.SS

StarPower Semiconductor $603290.SS

Nexperia

SPE (Front/Back-End) - Japan & Local China

Tokyo Electron $8035.T

Advantest $6857.T

Lasertec $6920.T

Disco $6146.T

Naura Technology $002371.SZ

Advanced Micro-Fabrication Equipment $688012.SS

Kingsemi $688037.SS

Optics - Cables, Connectors, Devices

Coherent $COHR

Lumentum $LITE

Applied Optoelectronics $AAOI

Fabrinet $FN

Zhongji Innolight $300308.SZ

Eoptolink $300502.SZ

Amphenol $APH

Credo $CRDO

Semtech $SMTC

Macom $MTSI

TE Connectivity $TEL

Corning $GLW

MLCC

Vishay Intertechnology $VSH

Murata Manufacturing $6981.T

Taiyo Yuden $6937.T

TDK $6762.T

Yageo $2327.TW

ABF Substrate

Unimicron $2302.TW

Shinko Electric $6967.T

Ibiden $4062.T

AT&S $ATS.VI

Nan Ya PCB $8046.TW

PCB/CCL

Victory Giant Technology $300476.SZ

Unimicron $2302.TW

Elite Material $2383.TW

WUS Printed Circuit $2368.TW

Furukawa Electric $5801.T

Taiwan Union Technology $6274.TW

Doosan $000150.KS

Shennan Circuits $002916.SZ

T-Glass

Nittobo $6762.T

InP Substrate

AXT Inc $AXTI

Sumitomo Electric $5802.T

Tantalum Powder

Advanced Metallurgical Group $AMG.AS

Silicon Wafers

Shin-Etsu Chemical $4063.T

SUMCO $3436.T

GlobalWafers $6488.TW

Siltronics AG $WAF.DE

Note: Does not cover all possible names. This is a brief overview.

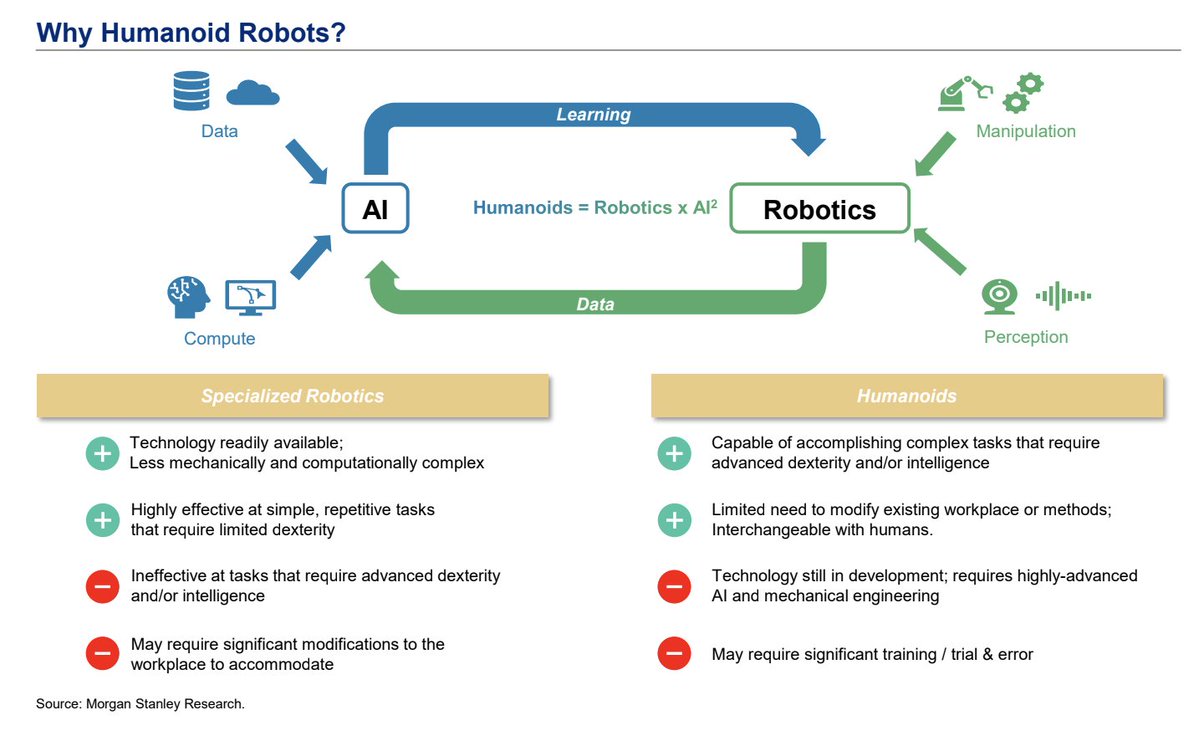

Goldman Sachs: Robotics Call Series

> Aggressive Market Share Target: Schaeffler aims to secure a market share of >10% by 2030 in the rapidly expanding global humanoid robotics sector.

> Explosive Market Growth: Humanoid robot sales volume is projected to multiply by 30x between 2025 and 2030 (reaching 1,000,000 units sold annually). Meanwhile, the bill of material (BOM) cost is expected to decrease by 30% (falling from $50,000 to $33,000).

> Massive Component Capture: Schaeffler's core competency products (such as bearings, encoders, torque sensors, and rotary/linear actuators) already comprise at least 50% of a standard humanoid robot's Bill of Materials (BOM).

Global Ecosystem & Tactical Partnerships

Schaeffler has rapidly embedded itself within the global robotics ecosystem via prominent investments and technology partnerships across major regions:

Americas: Executed a $10 million investment in Agility Robotics (November 2024) and has already deployed three "Digit" robots for material handling and logistics in its US plants.

Europe: Signed a technology partnership and supply agreement in April 2026 with Neura Robotics to supply rotary actuators and integrate Neura humanoids into Schaeffler's production lines.

Asia (China Focus): Signed technology partnerships in early 2026 with prominent regional players including Leju Robot, UBTECH, and Hexagon / Vindynamics.

AI & Software Infrastructure: Formed a partnership with NVIDIA to embed AI capabilities across the Omniverse ecosystem.

Production Footprint: Establishing the Taicang Humanoid Lighthouse Factory in China to serve as a collaborative baseline platform for the Asian humanoid ecosystem.

Commercialization Status

> 2026 as Year One: The company notes that 2026 marks the first true year of humanoid commercialization, driven primarily by service applications (e.g., consultants, education, sales assistants), whereas manufacturing applications will take longer due to strict efficiency benchmarks.

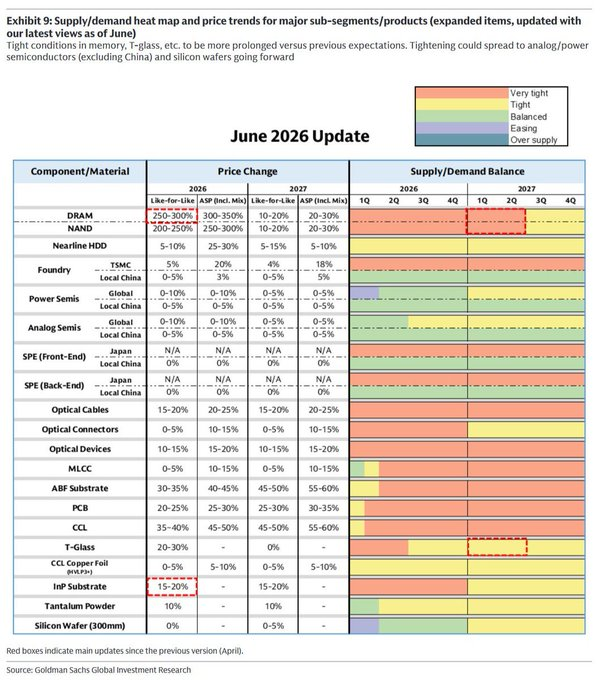

Goldman Sachs: June 2026 Update Supply/Demand

Compared to their May report, they have updated:

> NAND and DRAM from "tight" to "very tight" supply in Q1-Q2 of 2027.

> InP from "very tight" to "tight" in CY27

> T-Glass from "balanced" to "tight" in CY27.

Highlights:

> DRAM Pricing Surge: Like-for-like prices for DRAM are projected to skyrocket by 250–300% in 2026, with Average Selling Price (ASP) including product mix jumping 300–350%.

> Memory & T-Glass Supply Relief Delayed: The supply/demand balance for DRAM/NAND and T-Glass is expected to remain "Very Tight" longer than previously expected, extending all the way through Q2 2027 before potentially easing slightly to "Tight" in Q3 2027.

> InP Substrate: Like-for-like pricing for 2026 has been updated to 15–20%.

> Foundry (TSMC): Stays severely constrained through 2027.

> Advanced Substrates & Materials: ABF Substrate, PCB, and CCL face persistent, severe shortages. This is reflected in heavy price hikes, with CCL and ABF Substrate seeing price increases of 30–50% in 2026 and climbing even higher (45–60%) in 2027.

> Optical Components: Optical Cables and Optical Devices remain severely supply-constrained through the end of 2027, maintaining steady double-digit price increases.

> Global Power & Analog Semis: Shifting from "Balanced" or "Easing" in early 2026 to "Tight"by late 2026/early 2027. Note: Local China supply for these sectors is expected to remain "Balanced".

> Silicon Wafers (300mm): Starting out "Easing" in early 2026, but projected to transition to "Tight" by 2027.

> Local China Foundry & Equipment (SPE): Supply conditions for local Chinese foundries and Semiconductor Manufacturing Equipment (SPE) remain mostly "Balanced" with minimal price fluctuations (0–5%).

> MLCC & Tantalum Powder: Enjoying an "Easing" or "Balanced" state in early 2026 before settling into a stable "Tight" market for the remainder of the forecast period.

These parabolic move unwinds in the semis and in the data center assisters are playing out like all other parabolic moves, vicious , sudden. Now we are in no man's land for many, too later to sell but way too early to buy.

Trump: “You have a couple of guys who went short. Those poor ******* they’re in big trouble.

They’re being wiped out. The short guys.

I never liked short guys because they’re betting against the country”.

Breaking: Leopold Aschenbrenner's next investment just filed for Nasdaq this Friday

SK Hynix $SKHY is raising $28,000,000,000

Situational Awareness indicated interest in up to $7,000,000,000 of shares

Here's what he's buying into:

• 59% of the global HBM market

• 70% of Nvidia's HBM4 chip allocation

• Nvidia alone is 27% of their revenue

• Entire 2026 chip lineup already sold out

SK Hynix chips are inside the vast majority of premium AI data centers

Korean media reported that Kim Yong-kwan, President and Head of Business Strategy at Samsung Electronics’ Device Solutions division, said during a DS division management town hall meeting on July 3 that this year’s operating profit is expected to be in line with market consensus.

Korean brokerages estimate Samsung’s operating profit this year at around KRW 300 trillion, or roughly USD 200 billion.

In particular, Kim reportedly said, “This year’s profit alone will exceed the cumulative profit generated over the 40 years since Samsung entered the semiconductor business.”

According to a new review of the ThinkBook 14 G9 by Notebookcheck, Chinese PC maker Lenovo has, for the first time, begun shipping globally configured laptops equipped with YMTC-made SSDs.

$SNDK $MU

The AI infrastructure buildout is entering a new phase:

US tech companies are committing to spend a record $850 billion on data center leases over the next several years.

This marks a +$570 billion YoY increase, or +204%, and +$200 billion QoQ increase, or +31%.

Meta, $META, added the most in Q1 2026, committing +$79 billion in new leases, a +76% QoQ increase, bringing its total to ~$183 billion.

At the same time, Microsoft, $MSFT, added +$41 billion, a +26% QoQ increase, bringing its total to ~$197 billion.

Oracle leads with the largest total commitments at ~$250 billion, having already secured many of the key sites needed to fulfill its contract with OpenAI.

Tech companies are doubling down on AI.

What is happening in Hong Kong?

Chinese semiconductor exports to Hong Kong rose to a record $15 billion in May.

This figure has soared over +200% since early 2025.

At the same time, Chinese chip exports to the world surged to a record $35 billion, tripling over the same period.

As a result, Hong Kong accounted for 43% of China’s semiconductor exports in May.

Over the first 5 months of 2026, China exported $239 billion of chips globally, with Hong Kong absorbing over 50% of this total, a record proportion and up from ~33% a decade ago.

Hong Kong has become a dominant logistics hub for China’s chip trade.

Morgan Stanley: Robotics

> Humanoid robots represent the largest embodied AI opportunity, with a projected global total addressable market (TAM) of US$7.5 trillion by 2050, accumulating an estimated global stock of 1 billion robots.

> While the industry is in its infancy, Morgan Stanley forecasts that small-scale commercialization and pilot deployments will begin this year (2026).

> The global humanoid component market is projected to reach a TAM of US$780 billion by 2040. Key hardware components are expected to see massive demand multipliers by 2050 compared to 2025 levels, led by Edge Compute (1,904x), Bearings (370x), Motors (170x), and Reducers (157x).

> Shipment Forecasts: China’s humanoid shipments are expected to grow at an 85% CAGR between 2025 and 2030, rising from 12k units to 262k units.

> Cost Advantage: China possesses a significant Bill of Materials (BoM) cost advantage over non-China supply chains. Survey data reveals that potential adopters view a price range of US$14k–$28k (Rmb100k–199k) per unit as the sweet spot for broad adoption (with products like the Unitree G1 already selling at US$16k).

> Government Support: Government guidance funds for robotics exceed Rmb187 billion (~US$27 billion). Local governments are heavily subsidizing the ecosystem and actively creating early orders via "data collection centers".

> In 2025, China's humanoid shipment mix was heavily dominated by R&D/Education (42%), followed by Data Collection (19%), Interaction (19%), and Entertainment (16%).

10 WAYS TO PLAY ROBOTICS IN 2026

1. $TER tests AI chips & owns the cobots through Universal Robots

2. $NOVT precision photonics & motion inside surgical & industrial robots

3. $OUST eyes & perception for physical AI machines that need to see & map physical world

4. $HIMX provides vision & display chips that help robots process images, depth & sensor inputs at edge

5. $AMBQ low power edge AI layer for robots & devices that need intelligence without burning massive amounts of energy

6. $ON becomes physical AI edge stack after acquiring $SYNA combining power, sensing, connectivity & edge AI for robotics

7. $SYM warehouse automation pure play using robotics & software to redesign how goods move through fulfillment centers

8. $VPG sits in force sensing & precision measurement layer that helps robots understand pressure, weight & real world movement

9. $TSLA humanoid platform bet with Optimus combining custom hardware, AI inference, autonomy software & real world manufacturing scale

10. $CCXI gives public market exposure to Agility Robotics which is one of clearest pure play humanoid robotics companies through its Digit warehouse robot

Be SemiAnalysis:

- Post a scathing piece on CPO delays + optical company valuations, causing a crash.

Which $NVDA, analyst desks, and major optical companies refuted

- Launch an institutional photonics ETF after optical names dropped 40-60%.