Starting a challenge portfolio.

Positions just filled.

Half million.

Will screenshot ENTIRE portfolio often, NOT selectively showing positions like every other monkey KOL.

Do not follow. I do not want to be your customer support.

Just showing you it can be done. Be PERSISTENT.

2021 - Stocks top exit ( Publicly 20X )

2022 - Shifted to crypto ( Publicly 7X )

2025 - Crypto top exit

Frankly, I’m not confident. Markets look toppy. But whatever, will manage.

Everything is lining up. 2 big updates on the same day.

Can’t time it, it’ll come. Patience my friends.

2 companies I’ve been talking about

🔸Echostar @EchoStar $echo

🔸UBtech @UBTECHRobotics https://t.co/0mgSsw4mH2

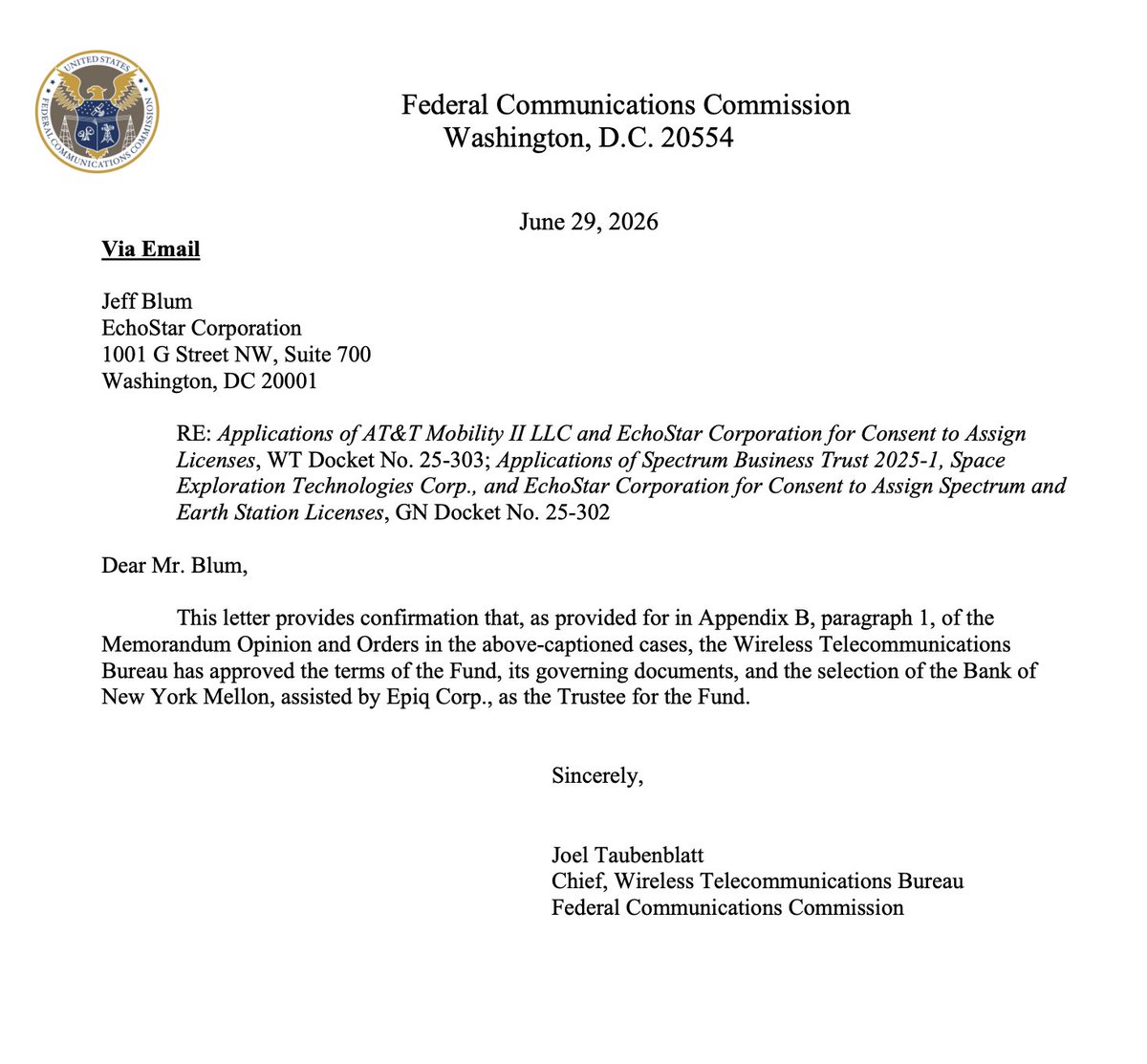

🔸Echostar - FCC approval is in. 29th June. Last step DOJ. Supposed to be close by now. Any day.

$20B+ incoming to clear most debt towards the first profitable quarter + share buybacks ( $2 Billion already approved )

If you are bullish $spcx , study echostar, do the maths.

Echostar owns 2% of spacex

There is a chance SpaceX does a merger with Echostar to take over all spectrums. Personally I hope it doesn’t happen. There’s more upside ( stock price ) as profitability / scaling services with spaceX comes in. I’m willing to hold this. Don’t give a fk until market prices this back to NAV.

🔸UBtech, First to launch humanoid robots looking this hot. Companion humanoid robots are trillions in TAM.

Trending on X

What else you want me to say? I wrote a thesis on this way too early (Highlights 2nd post). Pure humanoid play.

$6 Billion MCAP WTF. Not trading these plays. A day will come where stocks like these will do a semi / memory type of run.

Links post below

Premarket, everything nuking.

Good to know I'm holding below NAV with no leverage.

Time on my side.

Few updates on $SATS

🔸Ticker changing to $echo on 24th.

🔸Feels like rebranding into the first profitable quarter moving forward. Highest expense was debt payment.

🔸Most tax efficient way to deploy incoming profits will be buybacks to NAV.

🔸 I think $20 billion should come in this week.

🔸Lots of inaccurate NAV calculation out-there. All assuming management a monkey and don't know how to be more tax efficient.

🔸 Entire space sector went down, $sats down the least. Good to see that. Recovery will be glorious

🔸Most people forget CEO + Founder owns 50.5% of the stock. Find for me another CEO that have so much skin in the game.

The space narrative will be here to stay. Unlimited TAM. Good example. Project starfall. Demo in 2 days.

If you are uncomfortable, means you are over position sized or your conviction not there.

My theory of $sats price suppression and high short interest + how it will all end.

Convertible arbitrage is probably a major driver of SATS’s elevated short interest

$sats took on a lot of debt. Buyers of the converts sitting on a good 3X, want to lock in gains.

If you loan $sats $1000. You are up 3X. You are now given the option to lock in gains in the latest 10Q

WHAT DO YOU DO?

Short the ownership equal to the value of your own shares to lock in the gains aka convertible arbitrage.

Dateline: June 30

Math Maxing (from latest 10-Q and filings)

🔸Principal amount outstanding: ≈ $1.9426 billion ( Market Value now $6 Billion )

🔸Conversion rate: 29.73507 shares per $1,000 principal

🔸Potential shares if fully converted: ≈ 57.76 million shares

🔸Shares outstanding (as of March 31, 2026): ≈ 289.81 million

🔸Current short interest (as of May 29, 2026): 41.07 million shares

Short % of float: ≈ 30-32%

What does this all mean?

By June 30, Heavy conversion (many arbs convert)

30–50+ million shares bought to cover

Again, this is the kind of DD I’m doing. It makes hodling a hell lot easier.

There will be a time to cut. I’ll know when it comes.

Looking at my timeline. Made the perfect exit at top and perfect entry at bottom to the hour candle.

Was bullish $spcx

Everything was right. But the wrong vehicle again. Reminded me of $sbet

Giving $sats a little more time. If i cut, will let you know. All moves made on challenge port will be shared.

Fundamentally $sats great. Next earnings will be positive due less interest payments which was the problem + partnership with spacex to reduce capex is a great move.

I expect catalyst coming within days. Giving this trade a little more time.

LMAO, $sats liability is GONE. GONE! 😎

Just in 30 mins ago.

TLDR:

🔸$sats owe FCC $2.9 Billion.

🔸If Auction 113 raises ~$2.921 billion or more, EchoStar owes $0

It’s $3.1 Billion now 😎

Project out the rest of the spectrum echostar owns. Markets are pricing in ZERO 😂

Once in a blue moon, market hands you free money.

Do a simple search on $sats and the amount of attention is stock getting is minimal.

This is what you want.

When consensus agrees, you get out.

Last time shorts was this high? $sats did a 3X

$spcx now at $200 = $sats NAV @ $230

Not much shares left to short. Haven't been this excited for a long time 😎

GAMMA SQUEEZE

2 weeks max. $SATS skipped the June 1 interest payment on purpose. They’re confident the AT&T deal closes soon and they’ll easily repay within the 30-day grace period.

FCC approval is already in, assets are in trust, and once that ~$20B+ net cash hits at closing, the balance sheet gets cleaned up fast. Bullish setup.

imagine you own 50% of a publicly listed company.

32% of your float is shorted

When $22B deal is closed, what will you do with the cash?

1. You pay off the debt

2. Remaining cash? The obvious thing to do is do buyback

$SATS at $34 Billion Mcap + Excess cash of $8 Billion after paying down debt.

AHHHHHHHHHH I GONNA CUM

Most detailed, accurate calculation of $SATS i’ve seen.

Includes all concerns of tax, debt after sale and whatever minimal dilution.

This is a short squeeze in the making. I’ll explain the thesis next time.

To everyone questioning SpaceX / $SPCX’s highly successful IPO and its $2.1T market cap, let me share what I believe is the best arbitrage setup.

Do you know $SATS?

$SATS is expected to receive 261.8M shares of $SPCX, worth roughly $42B based on the 6/12 closing price.

Yet SATS’ current market cap is only about $33B.

Short: $SPCX

Long: $SATS

$SATS will effectively own approximately 2% of SpaceX / SPCX.

According to the SPCX prospectus, in exchange for acquiring spectrum from SATS, SPCX will pay SATS 261.8M shares of SPCX stock, roughly $8.5B in cash, and an additional ~$2.0B in cash to cover interest payments that SATS would otherwise have been responsible for.

In addition, SATS is expected to sell roughly $23B of spectrum to $T.

The transactions with $T and SPCX were approved by the FCC on 5/12. If no petition for reconsideration was filed by 6/11, the approval should likely have become final automatically. As of 6/14, I have not confirmed any petition for reconsideration.

Also, the spectrum transfer structure is SATS → TRUST → SPCX. Since the SATS → TRUST transfer has already been completed, I believe the closing risk is relatively low.

Now let’s calculate $SATS NAV.

My base NAV assumptions:

SPCX ownership: approximately 2%

SATS basic shares outstanding: 298M

Fully diluted shares after convertible bonds: 348M

I use 348M shares in the calculation below.

Cash proceeds from spectrum sales to $T and $SPCX:

From $T: approximately $23B

From $SPCX: approximately $8B in cash

Total: approximately $31B

Assuming the convertible bonds are converted into equity, net cash after debt repayment would be roughly $11B.

Regulatory / escrow / contingent liability haircut: -$2.5B

Net cash after haircut: approximately $8.5B

Remaining operating business value: $10B

Based on roughly $300M of operating income in Q1 2026 × 4 quarters × 8x multiple.

Even after the spectrum sales to $T and $SPCX, SATS will retain remaining spectrum assets. The most notable example is AWS-3 paired spectrum, which SATS previously planned to sell to $VZ for approximately $9.8B.

If we conservatively value the remaining spectrum at $10B, that adds approximately $28.7 per share of NAV based on 348M shares.

Formula:

SATS NAV

= {SPCX market cap × 2% + net cash after haircut + remaining operating business value + remaining spectrum value} / 348M shares

= {SPCX market cap × 2% + $8.5B + $10B + $10B} / 348M shares

SATS NAV by SPCX market cap:

• SPCX $2.0T → SATS approximately $197

• SPCX $2.25T → SATS approximately $211

• SPCX $2.5T → SATS approximately $226

• SPCX $2.75T → SATS approximately $240

• SPCX $3.0T → SATS approximately $254

This is my personal analysis, not financial advice.

So $sats is down a mere $3 from $117 entry and you guys are asking why.

zzzz

The entire space sector just rotated into $spcx. $sats is down the LEAST. Ain't that fking good?

On top of that, MMs needed to cover their ASS. They needed calls to expire worthless.

90% options were calls!

How do we know that?

Short Shares Availability tanked. LOOK AT THE PICTURE. $60+ million was used to pushed price down on a 35 Billion Mcap stock. WTF.

With short interest already 32% on a 50%+ of float thats not available to short?!?!!!! + AT&T deal to be closed in less than a month.

THIS IS A FKING SHORT SQUEEZE IN THE MAKING

Now trading at $90+ value to $170 $spcx per share.

It’s a fking no brainer.

A god candle will come. I live for god candles. It’s the best feeling in the world.

And I’ll be happy riding with you.

@Spawnnnn888 I cant control people’s entry. The best i can do is: The moment my trade goes through, i post 1-3 mins later. Infact my position was down when i shared.

All they needed to do was on notifications

@rioferdy838 arb traders will come in and close the gap. Again, free money. FREE money.

after my ALL in post yesterday, you can see markets beginning to price this accordingly.

Why I went all in $SATS

Here’s the maths:

SpaceX IPO at $135

SpaceX S1 disclosed Echostar owns 261.8 million shares

🔸$135 X 261.8 million shares = $35 Billion

While echostar was worth less than $35 Billion yesterday

Question:

Do you really think that you can put a $135 limit order on ipo day to get the shares?

NO!! Hyperliquid premarket AT $180 already 😂

Your best chance is do a market order buy on $sats before spacex ipo if you are bullish on spaceX

Here is where it gets crazier:

FCC APPROVED deal $22.65 Billion Cash for selling low to mid-band spectrum to AT&T

🔸So that’s worth ZERO? or NOBODY FKING CARED LMAO

My valuation ex- spaceX:

Net cash after debt paydown

$8.5 billion

Remaining unsold spectrum

$10 billion

Core operating business

$10 billion

Total Ex-SpaceX $28.5 billion

🔸Value per share EX- SpaceX ~ $86 ( Conservative )

Now let’s go from crazier to NUTS:

Short interest is 31% !!!! WTF LMAO

But the issue is founder owns 50.5% stake and 86.8% voting rights.

So the short interest on the remaining whatever available float? What’s that? 60++++%???

Seldom market hands you free money. When it does, go all in.

____

P.S. I seldom write long thesis anymore. Why? The hardworking ones will be rewarded with their own DD. You make your own conviction rather than relying on me for customer support.

And what do you want more when I put my own $$ on the line? Who does this transparently? Action speak more than words.

Once in a while, I'll write. But don't count on me mansplaining often. It's better for you to build your own conviction.