Susquehanna, 마이크론(Micron, $MU) 목표주가를 600달러에서 1,750달러로 상향

서스퀘하나의 시장 점검 결과, 2분기 D램(DRAM) 평균판매단가(ASP)가 전 분기 대비 50%~60% 상승할 것으로 보이며, 이는 당초 시장 기대치였던 50% 상승을 웃도는 수준이라고 분석했습니다.

또한 낸드(NAND) ASP 역시 전 분기 대비 75%~100% 상승하며 기존 추세를 유지하고 있다고 보고했습니다.

호세이니 애널리스트는 이러한 혼합 평균판매단가(blended ASP)의 지속적인 강세와 마진 구조의 지속 가능성에 대한 확신이 커짐에 따라, 자신이 담당하는 메모리 반도체 제조사들에 대한 실적 전망치를 상향 조정한다고 밝혔습니다.

These 5 stocks should 100%-400% by holding it until 2030-2035:

1. $GOOG — analyst consensus strong buy, avg PT ~$600, with bulls targeting $550. I used $550 as a 2030-horizon bull case.

2. $MU — Deutsche Bank and DA Davidson both have PT of $1,200 with Buy ratings, citing HBM supply locked through 2030+.

3. $NVDA — avg analyst PT ~$280, highest at $380. Used $350 as a strong conviction long-term target.

4. $AMD — BofA recently raised PT to $600, citing AI spending staying strong longer than the market expects through 2030

5. $LITE — Rosenblatt has the street-high PT at $2,000, with JPMorgan at $1,230 and Mizuho at $1,400 after Lumentum's earnings blowout.

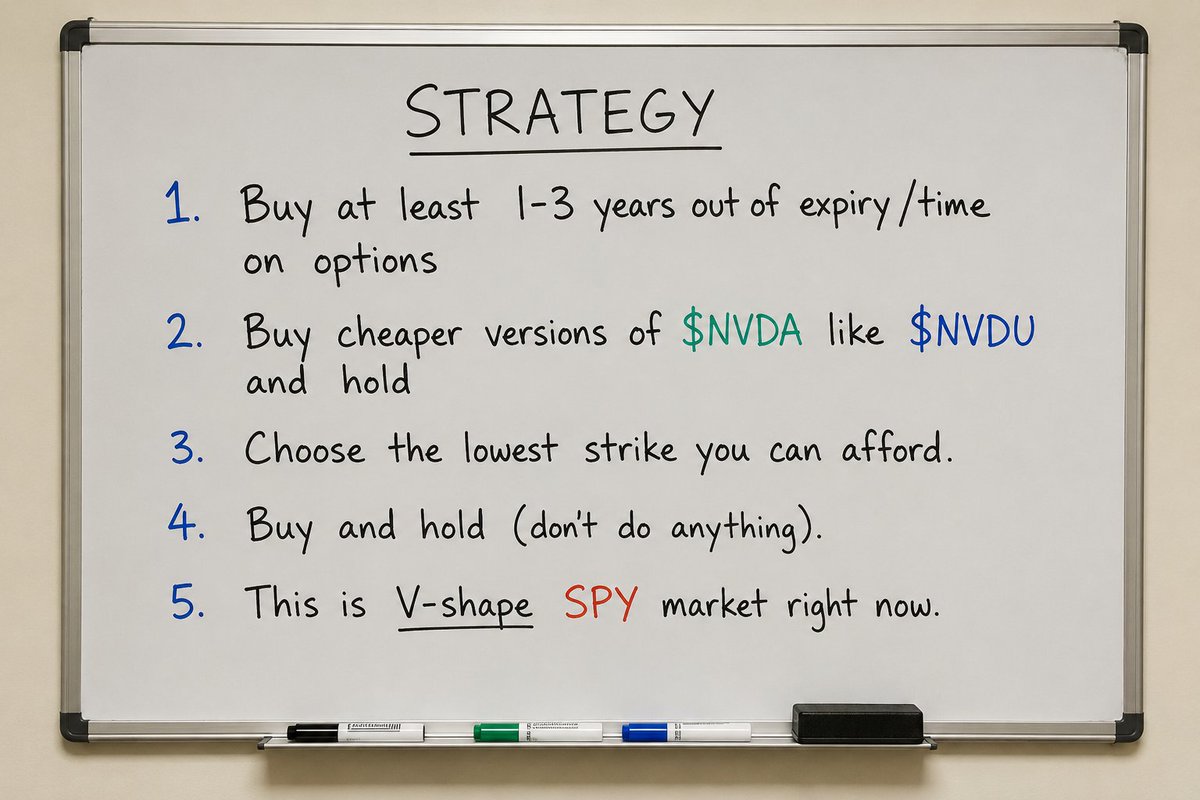

Remember, the strategy is this:

1. Buy at least 1-3 years out of expiry/time on options

2. Buy cheaper versions of $NVDA like $NVDU and hold

3. Choose the lowest strike you can afford.

4. Buy and hold (don't do anything).

5. This is V-shape SPY market right now.

Kioxia with massive earnings beats!

Kioxia is a Japanese NAND producer which shares manufacturing with SanDisk $SNDK.

They reported quarterly earnings this morning and crushed the estimates, especially the guidance:

Q4 FY2026:

Operating income: 596.80bn yen (est. 519.33bn yen)

Net income: 407.73bn yen (est. 358.21bn yen)

Q1 FY2027 guidance:

Operating income: 1.30tn yen (est. 874.09bn yen)

Net income: 869.00bn yen (est. 612.71bn yen)

Further comments worth noting:

- Extremely strong and sustained AI demand in data centers/enterprise SSDs.

- NAND capacity for the year 2026 already sold out, with Kioxia's management expecting demand to continue outstripping supply in 2027.

- Kioxia is preparing for a US ADR listing.

NAND shortages are not ending any time soon, and $SNDK and $MU are poised to profit from it.

$DRAM $EWY $MU $SNDK

Heard Sanjay Mehrotra Micron $MU CEO at TIEcon today. Here’s what matters for investors.

Micron’s market cap was ~$30B when he joined. It’s ~$600B today. That’s not a cycle. That’s a strategy.

Three things that built that 20× run:

1. Manufacturing is the moat.

Foundries can’t give you the cost structure you need to win in memory. Mehrotra learned this at $SNDK SanDisk moved to a Toshiba JV to own the technology at the cost of the technology. At Micron, owned fabs + global operations = the barrier no one can replicate without decades and hundreds of billions.

2. Cadence is the competitive weapon.

Micron has compressed its technology generation cycle to 12 months faster than typical industry pace. Faster node transitions = lower cost per bit, better yields, premium pricing windows, and customers pulled deeper into the ecosystem.

3. AI is early innings and memory is at the heart of ALL of it.

Whether it’s GPUs, CPUs, or custom ASICs nothing runs without DRAM and NAND. The memory market is ~$100B today. Mehrotra sees it hitting $300B+ by 2030, potentially $600B as AI compounding continues. HBM and data center DRAM are the high-profit pools

Micron is deliberately rotating toward.

His line that landed:

“Semiconductors get the first bite before software eats the world.”

AI agents driving business transformation are just starting. This is not a late-cycle bet on memory it’s an early-cycle bet on infrastructure.

$MU is not just a chip company. It’s a foundational layer of the AI buildout.