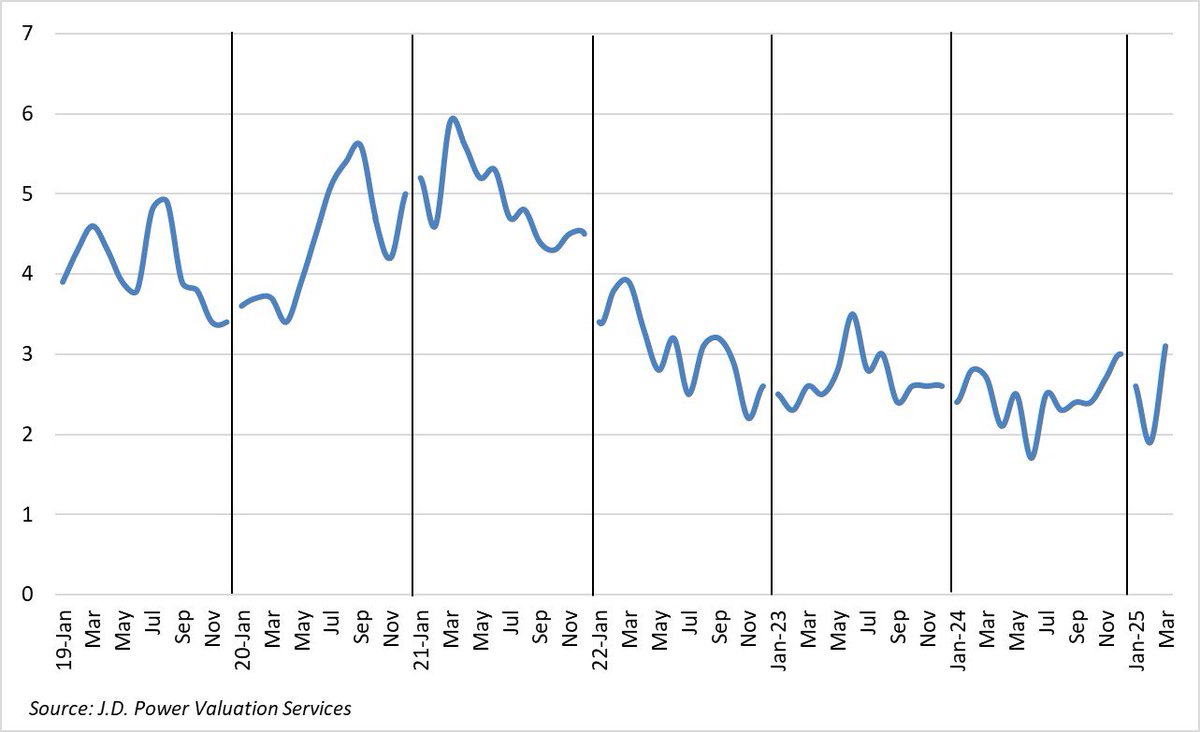

After a strong Q1, the used Class 8 market is on cruise control. The market will continue to strongly favor low-mileage trucks as the supply of higher mileage units increases with pre-buy activity in upcoming months. Read more here:

https://t.co/x8vNS1yC2I

Sustained freight rate improvement, healthy retail sales, and stable pricing collectively signal that the used truck market has cycled back into positive territory. May data here:

#trucking#Assetmanagement#usedtrucks

https://t.co/cPNueb2Gvc

Class 8 retail sales volume roared back in March to the highest level in almost 5 years. Pricing remained stable, suggesting buyers are more confident about their prospects going forward. More data and commentary here:

https://t.co/mIFNfMNHHu

In the March edition of Guidelines, we track lower selling prices in February and provide color behind the movement. Download here:

#trucking#fleets

https://t.co/DoVWuoaIGT

The 2026 used truck market opened up strong in Jan. Auction and retail pricing increased over December, and retail volume was very healthy (by recent standards) for the 2nd month in a row. Click below to download our Feb. Guidelines Market Report:

https://t.co/yXzR2QCFc3

In the January edition of our Guidelines monthly market report, we track auction and retail volume and selling prices over 2025, and provide an outlook for 2026. Click here to download:

#Assetmanagement#fleets#trucking

https://t.co/XuPsE5ZGJJ

As the used Class 8 market enters its seasonal lull, we’re looking towards next year for active truck utilization and capacity to adjust back to where they eventually kick the cycle back into the acquisition phase. Data and commentary here:

#trucking

https://t.co/IpYTWjG4rl

October Class 8 auction pricing was down 6% MoM but up 2% YoY. Pricing is about halfway between 2018 (strong) and 2019 (weak) markets in real numbers. Any recovery will be supply-driven (fleet downsizing), and require the goods economy to hold up.

#FleetManagement#class8

Since July, retail depreciation for sleeper tractors has averaged 2.1%. This is a notable change from stable pricing in 1H. On the bright side, dealers are retailing more trucks than last year. October Guidelines available here:

https://t.co/VVhNwTVSyo

At Class 8 auctions in August, volume ticked up while pricing moved down. 4-6 year-old sleeper tractors averaged 4.6% lower pricing than July, but only 0.4% lower than August 2024. Average monthly depreciation in 2025 is now up to 2.1%. More data and insight next week.

In July, Class 8 sleeper retail selling prices decreased M-o-M for the first time since December 2024. However, dealers sold more trucks than in June. Y-o-Y comparisons remain positive. Click the link below for our full August market update:

https://t.co/BxGCTEIgy2

3-year-old sleepers finally made an appearance at auctions in June. Our July Guidelines provides data on the auction and retail channels, along with commentary. Click here for the download page:

https://t.co/ezoDoTH874

Class 8 sleeper retail pricing increased for the 5th month in a row in May, albeit less than 1%. Retail sales per dealership also ticked up to 3.2 trucks - the best result since June 2023.

More data in the June edition of Guidelines, available here:

https://t.co/CXAco1ItQC

Class 8 auction pricing pulled back in May, with late-model sleepers bringing 3.7% less money MoM. We’re also seeing fewer 3-year-old trucks than we’d typically expect by midyear. Some end users are likely holding off on trading for new.

Supply was tighter and pricing was higher at April Class 8 auctions, as end users traded out of their older trucks to take advantage of what could be the last of pre-tariff, pull-ahead freight activity, plus get ahead of higher pricing. More here:

https://t.co/VsYxPN2ncM

@SegResearch@FreightAlley Why it happened was China’s raw material output grew exponentially from 1995-2018, at a lower price than Canada and Mexico. Why it was *allowed* to happen is we didn’t deem it necessary to substantially limit Chinese imports in that period.

New and used truck markets are diverging. New truck orders/deliveries are weak, while used truck pricing/volume is showing strength. Details and analysis in our April Guidelines, available here:

https://t.co/AB6ZMeHyLk

A bit of good news on a Friday afternoon: Commercial truck retail sales per dealership swung back up into the 3’s in March, averaging 3.1 trucks per rooftop, for the best result since June, 2023. 3.1 is not strong by historical standards, but it outpaces March 2023 and 2024.

Volume and pricing of sleeper tractors both increased at March auctions. 4-6YO trucks averaged 5.6% more than February, and 29.3% more than March 2024. The equipment cycle remains in an extended conservative phase as buyers gauge the impact of unpredictable tariff policy.