Onchain capital markets, May 2026:

$315B in stablecoin supply.

$26B in tokenized RWAs.

$15B in tokenized US Treasuries.

Three years ago, none of this existed at scale.

COIND backs the infrastructure that makes the next $300B possible.

Stablecoins · RWA · Regulated rails

BlackRock filed two SEC applications for tokenized money-market funds on May 8.

One is a digital share class for an existing $6.1B fund. The other is BRSRV — a purpose-built vehicle for stablecoin issuers parking reserves under the GENIUS Act.

The second filing matters more. It's not a digital wrapper around old infrastructure. It's new infrastructure built for stablecoin economics from day one.

When the largest asset manager designs a product specifically for stablecoin reserves, the category has moved past validation.

Senate Banking markup of the CLARITY Act is scheduled for Thursday, May 14.

Polymarket odds of passage in 2026 moved from 46% to 64% the day the yield compromise dropped.

The compromise is structural — and most stablecoin teams haven't internalized what it means yet.

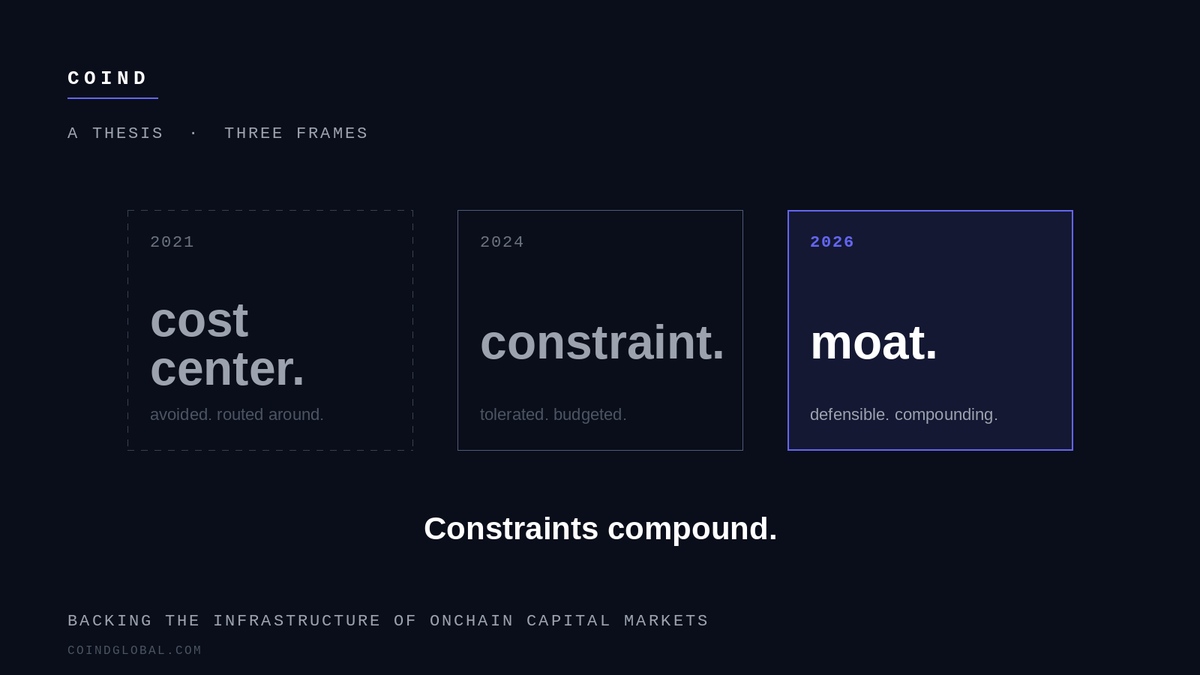

A thesis we keep coming back to: compliance is the moat.

In 2021, compliance was a cost center. Founders avoided it as long as possible. Capital found ways around it.

In 2026, the most defensible companies in crypto are the ones building inside the regulatory frame, not despite it.

Constraints compound.

@compoundfinance is one of the most underappreciated primitives in onchain finance.

While the headlines focus on new launches, Compound has been the rails for $X+ in onchain credit since 2018.

Boring infrastructure beats novel speculation, every cycle.

This week:

— Visa added 5 new networks for stablecoin settlement

— Meta + Stripe launched USDC payouts to creators

— Western Union announced Solana stablecoin USDPT

— State Street unveiled tokenized fund services

Three years ago, none of these companies were "in crypto."

The infrastructure is no longer a side bet for them.

Things we're reading this week:

→ a16z: 9 charts on what stablecoins are becoming

[link]

→ The Defiant: how RWAs became Wall Street's gateway to crypto in 2025

[link]

→ Norton Rose Fulbright: China's 2026 crypto framework and the legal regime for RWA tokenization

[link]

Underrated chart in the a16z stablecoin report:

Stablecoin velocity has roughly doubled since early 2024 — from 2.6× to 6× monthly turnover.

Each dollar of supply is now doing 2.3× the work it did 24 months ago.

Most builders optimize for supply growth. The opportunity is in capturing velocity.

RWA tokenization crossed $30B onchain this week.

Two years ago: $5B. One year ago: $12B. Today: $30B.

The growth isn't from speculation — it's from BlackRock, Franklin Templeton, JPMorgan, State Street, Circle. Every major asset manager is shipping product.

The question is no longer "if". It's "where on the curve are we?"

The CLARITY Act yield compromise is the most important policy development for stablecoin infrastructure this year.

Yield on holding = banned. Yield on activity = allowed.

This isn't a setback. It's a forcing function. The next generation of stablecoin products has to do something — not just sit there.

Buy-and-use, not buy-and-hold.

@delighttoecz wait so when you say "on chain" does that mean the actual art is stored on the blockchain?? 🤔 i thought it was just like a receipt or something!